Home » Posts tagged 'mining'

Tag Archives: mining

#BRES Blencowe Resources PLC – Beehive Drilling Results

Blencowe Resources Plc (LSE: BRES) is pleased to provide an update on further assay results from shallow drilling at the company’s new Beehive deposit. Both Beehive and Iyan are substantial new exploration finds within the most recent 2025 drill programme and both will contribute significantly to the size and scale of the Orom-Cross graphite project.

Blencowe Resources Plc (LSE: BRES) is pleased to provide an update on further assay results from shallow drilling at the company’s new Beehive deposit. Both Beehive and Iyan are substantial new exploration finds within the most recent 2025 drill programme and both will contribute significantly to the size and scale of the Orom-Cross graphite project.

As part of the Stage 7 drilling programme, the Company completed 110 shallow drill holes at Beehive, designed to test the continuity, thickness and near-surface extent of graphite mineralisation. This announcement reports further assay results from 36 holes (including additional coverage toward the northern extent), following the Company’s previous Beehive assay update.

The shallow programme was designed to define near-surface, bulk mineable graphite mineralisation, with holes drilled to a planned depth of approximately 30 metres. The majority of reported holes intersected graphite mineralisation from near surface to end-of-hole, with many holes ending in mineralisation, highlighting potential for continuation below the current shallow drilling depth. This is consistent with previously reported deeper drilling at Beehive, which demonstrated graphite mineralisation continuing to approximately 100 metres depth.

Whilst the drilling was intended to close out the northern extent of the deposit, results also indicate potential for additional extensions of up to ~400m – particularly toward the northern and western end of the deposit – within the broader target area.

Beehive Drilling Highlights

An additional 36 assay results were received and compiled from the Stage 7 programme:

· Thick near-surface mineralisation: multiple holes deliver ~30-32 meters mineralisation from surface, supporting depth continuity and bulk mining potential.

· Strong bulk grades across the batch: 12 holes average ≥5.0% TGC and 8 holes average ≥6.0% TGC over the drilled intervals highlighting strong in situ grades within Beehive.

· High-grade frequency: all holes are mineralised and grades are consistently higher than overall average grades for other deposits within Orom-Cross.

Selected Beehive Significant Shallow Intercepts Include:

o BHDD-L101: 31.5 meters @ 8.19% TGC from surface

o BHDD-L111: 31.4 meters @ 8.00% TGC from surface

o BHDD-L327: 31.2 meters @ 7.67% TGC from surface

o BHDD-L113: 31.92 meters @ 7.59% TGC from surface, including 9.32m @ 11.14% TGC

o BHDD-L133: 31.4 meters @ 6.83% TGC from surface

o BHDD-L102: 29.61 meters @ 6.11% TGC from surface

o BHDD-L325: 31.3 meters @ 6.21% TGC from surface

Interpretation and Next Steps

These additional shallow results continue to support a thick graphite system at shallow depths, while previously reported deeper drilling has demonstrated mineralisation continuing to approximately 100 metres depth. Together, this work is building the dataset required to define the near-surface component and progress modelling toward a maiden Beehive JORC Mineral Resource scheduled for Q2 2026.

Further Beehive assay batches are being passed directly to the Company’s independent geological consultants, Minrom, for validation and quality assurance. Results will be reported progressively as batches are cleared and, subject to modelling, are intended to support a future Beehive JORC Mineral Resource update and provide further clarity on overall scale and development readiness as Blencowe continues to progress strategic and funding discussions in parallel.

Beehive has been defined over approximately 1,200 metres of strike and 480 metres of width to date, with scope for extensions beyond the current drill lines.

Blencowe Resources Executive Chairman, Cameron Pearce commented:

“We are pleased to report a further batch of Beehive assay results and appreciate shareholders’ patience as results move through laboratory reporting and independent validation. We expect a further set of assay results to become available shortly and will provide updates as batches are cleared.

Beehive continues to build momentum. This further batch reinforces continuity at shallow depths, with multiple plus-30 meter intercepts from surface and standout results including 31.5m @ 8.19% TGC and 31.4m @ 8.00% TGC.

Following the recent maiden Iyan JORC Mineral Resource of 16.9 million tonnes, which increased total Orom-Cross JORC Mineral Resources by 66% to 43.0 million tonnes, Beehive remains the next clear growth lever as we progress toward a maiden Beehive JORC Mineral Resource update this quarter. We would expect the continuity and thickness being demonstrated at Beehive to translate into a material increase in overall tonnage, subject to completion of assay flow, modelling and JORC reporting.

With access to renewable hydroelectric power and an expanding resource base, Orom-Cross continues to be positioned as an integral part of the western markets’ drive for secure, non-China critical mineral supply chains, supporting downstream pathways and longer-term offtake discussions.”

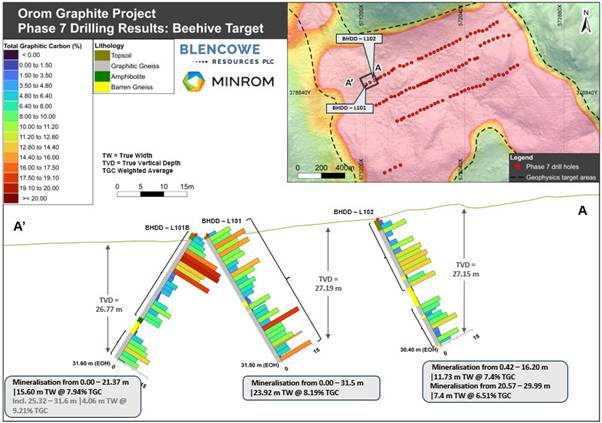

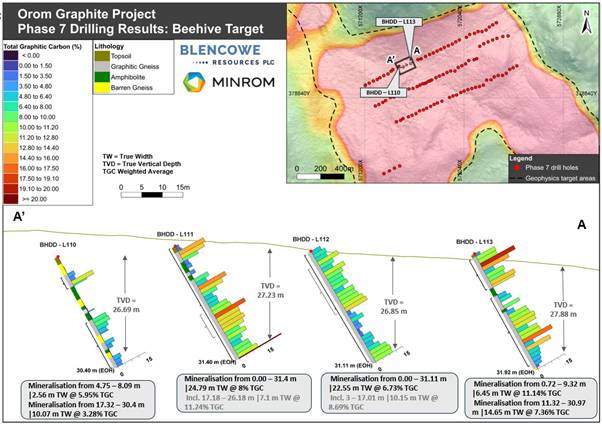

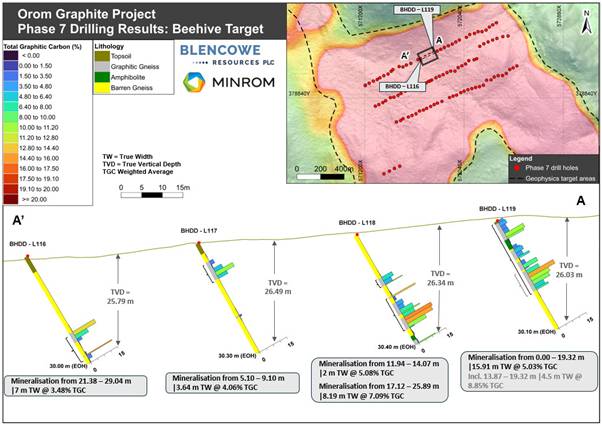

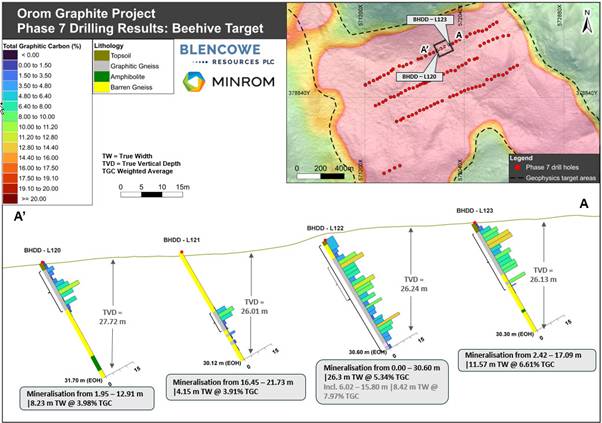

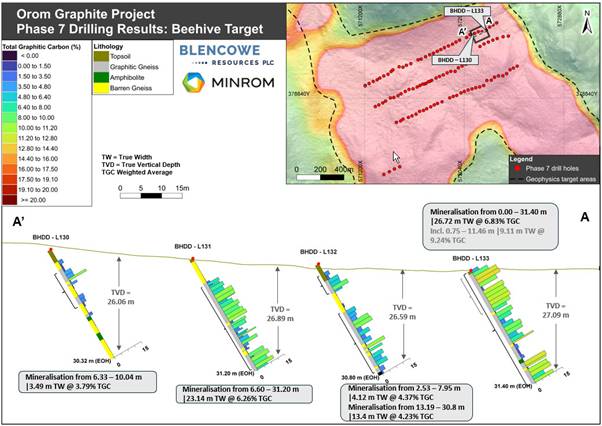

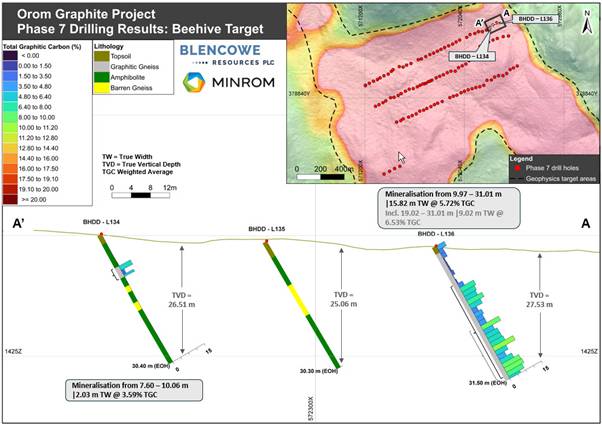

Beehive Deposit – Key Drill Results

Figures 1-2: Beehive Deposit drill sections showing thick, continuous graphite mineralisation remaining open at depth.

|

Blencowe Resources Plc |

|

|

Sam Quinn (Director) |

Tel: +44 (0)1624 681 250

|

|

Sasha Sethi (Investor Relations) |

Tel: +44 (0) 7891 677 441 |

|

Tavira Financial (Joint Broker)

Jonathan Evans |

Tel: +44 (0)20 3192 1733 |

|

Oak Securities (Joint Broker)

Calvin Man /Mungo Sheehan / Jerry Keen |

Tel: +44 (0)20 3973 3678 |

|

|

|

|

|

#SVML Sovereign Metals Limited – Change of Director’s Interest Notice x4

LAPSE OF PERFORMANCE RIGHTS

LAPSE OF PERFORMANCE RIGHTS

Sovereign Metals Limited (ASX:SVM; AIM:SVML; OTCQX:SVMLF) (Sovereign or the Company) advises that 4,992,500 unlisted performance rights that were subject to the “Mining Licence Milestone” lapsed on 31 March 2026 without exercise or conversion.

Following the lapse of these unlisted performance rights, the Company has the following securities on issue:

· 646,938,703 fully paid ordinary shares (of no par value);

· 6,190,000 unlisted performance rights subject to the “Final Investment Decision Milestone” expiring on or before 30 June 2026.

· 9,022,500 unlisted performance rights subject to the “Bankable Definitive Feasibility Study Milestone” expiring on or before 30 June 2026; and

· 13,262,500 performance rights subject to the “Construction and Finance Milestone” that have no exercise price and expire 30 June 2028.

Change of Directors’ Interest Notices in relation to the lapse of unlisted performance rights have been provided below.

|

Enquiries |

|

Dylan Browne Company Secretary +61 8 9322 6322 |

|

Nominated Adviser on AIM and Joint Broker |

|

|

SP Angel Corporate Finance LLP |

+44 20 3470 0470 |

|

Ewan Leggat Charlie Bouverat |

|

|

|

|

|

Joint Broker |

|

|

Stifel |

+44 20 7710 7600 |

|

Varun Talwar |

|

|

Ashton Clanfield |

#SVML Sovereign Metals Limited – Results of Meeting and Issue of Performance Rights

A General Meeting (GM) of Sovereign Metals Limited (Company) (ASX:SVM; AIM:SVML; OTCQX: SVMLF) was held today, 18 February 2026, at 11.00am (AWST).

A General Meeting (GM) of Sovereign Metals Limited (Company) (ASX:SVM; AIM:SVML; OTCQX: SVMLF) was held today, 18 February 2026, at 11.00am (AWST).

The resolutions voted on were in accordance with the Notice of GM previously advised to shareholders. All resolutions were decided on and carried by way of poll.

In accordance with Section 251AA of the Corporations Act 2001 and ASX Listing Rule 3.13.2, the details of the poll and proxies received in respect of each resolution are set out below.

Sovereign Metals Limited (ASX:SVM; AIM:SVML; OTCQX:SVMLF) (Sovereign or the Company) advises that it has today issued 8,650,000 unlisted performance rights to Directors following shareholder approval as follows:

· 3,600,000 unlisted performance rights subject to the “Bankable Definitive Feasibility Study Milestone” expiring on or before 30 June 2026; and

· 5,050,000 performance rights subject to the “Construction and Finance Milestone” that have no exercise price and expire 30 June 2028.

Following the issue of these unlisted performance rights, the Company has the following securities on issue:

· 646,938,703 fully paid ordinary shares (of no par value);

· 4,992,500 unlisted performance rights subject to the “Grant of Mining Licence Milestone” expiring on or before 31 March 2026 (expected to lapse unvested);

· 6,190,000 unlisted performance rights subject to the “Final Investment Decision Milestone” expiring on or before 30 June 2026 (expected to lapse unvested);

· 9,022,500 unlisted performance rights subject to the “Bankable Definitive Feasibility Study Milestone” expiring on or before 30 June 2026; and

· 13,262,500 performance rights subject to the “Construction and Finance Milestone” that have no exercise price and expire 30 June 2028.

|

Enquiries |

|

Dylan Browne Company Secretary +61 8 9322 6322 |

|

Nominated Adviser on AIM and Joint Broker |

|

|

SP Angel Corporate Finance LLP |

+44 20 3470 0470 |

|

Ewan Leggat Charlie Bouverat |

|

|

|

|

|

Joint Broker |

|

|

Stifel |

+44 20 7710 7600 |

|

Varun Talwar |

|

|

Ashton Clanfield |

|

#SVML Sovereign Metals LTD – Issue of Performance Rights

Sovereign Metals Limited advises that 13,635,000 unlisted performance rights have been issued to key staff (non PDMRs) as part of their incentive remuneration as follows:

· 5,422,500 unlisted performance rights subject to the “Bankable Definitive Feasibility Study Milestone” expiring on or before 30 June 2026; and

· 8,212,500 performance rights subject to the “Construction and Finance Milestone” that have no exercise price and expire 30 June 2028.

Following the issue of these unlisted performance rights, the Company has the following securities on issue:

· 646,938,703 fully paid ordinary shares (of no par value);

· 4,992,500 unlisted performance rights subject to the “Grant of Mining Licence Milestone” expiring on or before 31 March 2026 (expected to lapse unvested);

· 6,190,000 unlisted performance rights subject to the “Final Investment Decision Milestone” expiring on or before 30 June 2026 (expected to lapse unvested);

· 5,422,500 unlisted performance rights subject to the “Bankable Definitive Feasibility Study Milestone” expiring on or before 30 June 2026; and

· 8,212,500 performance rights subject to the “Construction and Finance Milestone” that have no exercise price and expire 30 June 2028.

|

Enquiries |

|

Dylan Browne Company Secretary +61 8 9322 6322 |

|

Nominated Adviser on AIM and Joint Broker |

|

|

SP Angel Corporate Finance LLP |

+44 20 3470 0470 |

|

Ewan Leggat Charlie Bouverat |

|

|

|

|

|

Joint Broker |

|

|

Stifel |

+44 20 7710 7600 |

|

Varun Talwar |

|

|

Ashton Clanfield |

|

#BRES Blencowe Resources PLC – Beehive Delivers 2 Standout +90 metre Intercepts

Blencowe Resources Plc (LSE: BRES) is pleased to report the remaining two deep-hole assay results from the newly discovered Beehive deposit, located approximately 3kms from the existing Northern Syncline and Camp Lode deposits at the Orom-Cross graphite project in Uganda.

Blencowe Resources Plc (LSE: BRES) is pleased to report the remaining two deep-hole assay results from the newly discovered Beehive deposit, located approximately 3kms from the existing Northern Syncline and Camp Lode deposits at the Orom-Cross graphite project in Uganda.

Beehive is an extensive new graphite discovery made during the Company’s broader Stage 7 drilling programme in 2025, with exploration there comprising three deep holes to depths below 100 metres to test continuity and 108 shallow holes designed to test graphite mineralisation from surface to 30 metres, which is considered most attractive for low cost-effective mining.

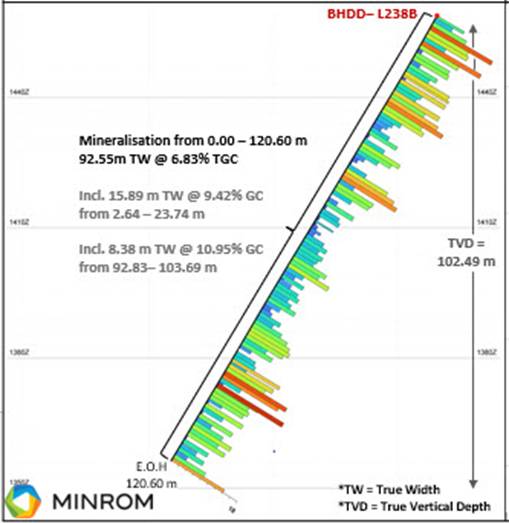

Following the exceptional results previously reported from deep Hole L238B (returning 92.55m @ 6.83% TGC), the Company now reports further excellent drilling results from Beehive deep holes L237B and L239B. These results continue to highlight Beehive as a thick, continuous graphite system and reinforces its potential to deliver meaningful higher-grade early production tonnes within the broader Orom-Cross mining strategy.

Together with recent results from the Iyan Deposit and the existing Northern Syncline and Camp Lode resources, these Beehive results further support Orom-Cross as a graphite system of sufficient scale to underpin long-life and multi-decade production; a key consideration for strategic and institutional funding groups.

In addition to the three Beehive deep holes the programme included 108 shallow holes at Beehive and 72 shallow holes at Iyan. Assay results from these remaining holes are expected near term, providing a clear pipeline of ongoing newsflow as the Company progresses funding discussions in parallel.

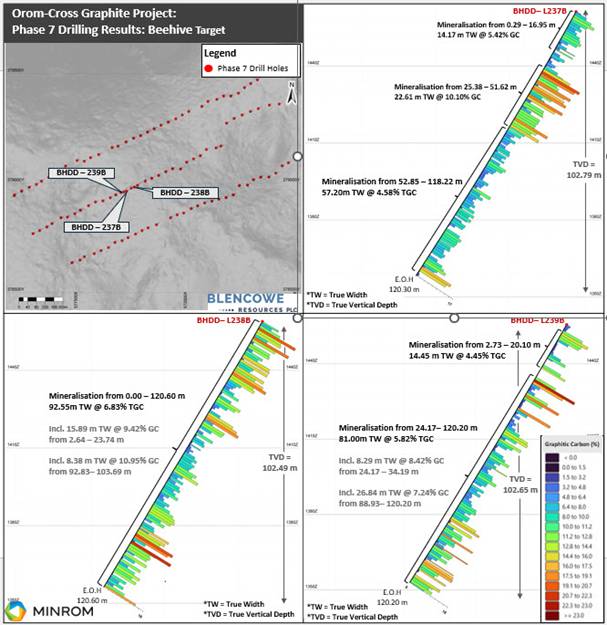

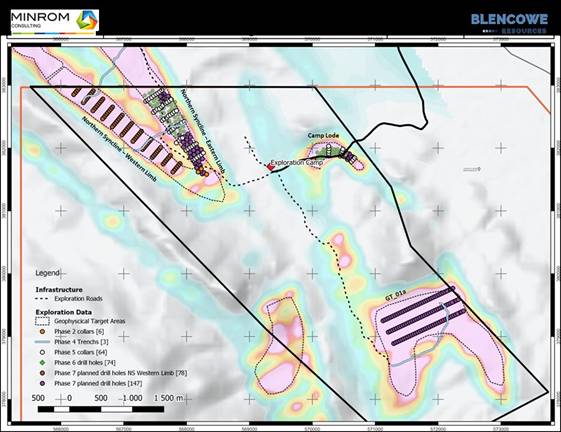

Beehive Deposit – Key Drill Results

Figure 1: Beehive Deposit deep-hole drill sections showing thick, continuous graphite mineralisation remaining open at depth.

Hole L237B:

93.98m (TW) @ 6.03% TGC, comprising three stacked mineralised intervals from near surface to 118.22m, including:

· 22.61m (TW) @ 10.10% TGC,

o including internal high-grade interval of 3.00m @ 14.64% TGC,

o including 1.46m @ 14.3% TGC, and

o including 1.00m @ 12.72% TGC

· 14.17m (TW) @ 5.42% TGC from surface,

o including grades up to ~9.4% TGC

· 57.20m (TW) @ 4.58% TGC,

o including 2.08m @ 12.75% TGC

Hole L239B:

95.45m (TW) @ 5.62% TGC, comprising two stacked mineralised intervals from 2.73m to end of hole at 120.20m, including:

· 81.00m (TW) @ 5.82% TGC,

o including 0.67m @ 18.90% TGC,

o including 1.00m @ 11.98% TGC,

o including 1.00m @ 11.96% TGC, and

o including 4.00m @ 9.95% TGC

· 14.45m (TW) @ 4.49% TGC,

o including 0.69m @ 15.46% TGC

These latest two holes reported are in addition to Hole L238B which was announced in December 2025, with 92.55 metres (TW) @ 6.83% TGC, including 15.89 metres @ 9.42% TGC and 8.38 metres @ 10.95%.

Geological Interpretation

The two newly reported deep holes were drilled to test whether the Beehive graphite system continues beyond the previously reported Hole L238B.

· Hole L237B confirms that thick, high-grade graphite continues along the Beehive structure.

· Hole L239B confirms that graphite continues to depth, with mineralisation still present at the end of the hole.

· All three deep holes intersect graphite from near surface and remain open at depth, which highlights the strength and continuity of the system.

This combination of thickness, continuity and mineralisation remaining open at depth is characteristic of large, long-life graphite systems rather than short-lived or isolated deposits.

Across all three deep holes, Beehive has now delivered consistent mineralised thicknesses of around 90-95 metres, with multiple high-grade zones occurring within each hole. This consistency supports Beehive being interpreted as a large, continuous graphite deposit, rather than isolated high-grade pockets.

Size, scale and continuity are important factors for strategic and institutional funding groups, which typically focus on projects capable of supporting long-life, multi-decade production. Blencowe has existing licenses to explore a mineralised area at Orom-Cross over 20 kilometres in length yet all drilling completed to date sit only within the (ML 1959) Mining License zone which is just a small part of the overall deposit and licensed area.

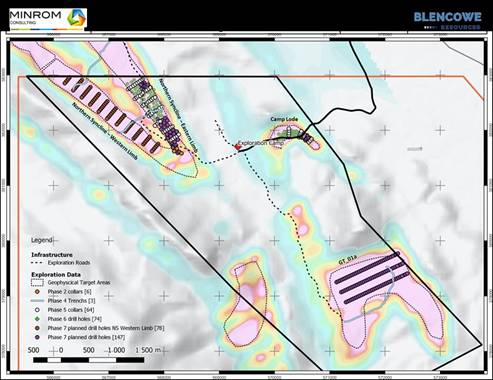

Figure 2: Orom-Cross graphite project showing ML1959 as a part of the overall licensed area.

Blencowe now awaits assay results from the remaining 108 shallow holes drilled at Beehive, which are expected to define significant near-surface tonnage and further demonstrate the overall scale of this new discovery. Beehive sits within the Company’s existing 21-year Mining Licence (ML1959) granted in 2019, adding to its development and permitting strength.

Executive Chairman Cameron Pearce commented: “Beehive continues to deliver standout deep-hole drill results, further demonstrating the scale, continuity and quality of this deposit. The presence of thicker, higher-grade zones reinforces its potential to add meaningful tonnes and support multi-decade production potential, particularly if these results are replicated across the 108 remaining shallow Beehive holes currently being assayed. This is in addition to results expected for another 72 step-out and exploratory holes from Iyan.

Demand for graphite continues to grow, especially for higher quality end-products such as those delivered from Orom-Cross. The Company believes this project has the potential to rank among the larger, lower-cost graphite developments globally, supported by a completed DFS, advanced project readiness, fully completed metallurgical pre-qualification and offtake arrangements in place for all of Phase 1 Production.

With a large volume of drill results still pending from the ongoing programme, we see a clear pathway to continued scale growth and we anticipate a steady flow of further updates as we progress into 2026 while advancing funding discussions in parallel.”

For further information please contact:

|

Blencowe Resources Plc Sam Quinn |

www.blencoweresourcesplc.com Tel: +44 (0)1624 681 250 |

|

Investor Relations Sasha Sethi |

Tel: +44 (0) 7891 677 441 |

|

Tavira Financial Jonathan Evans |

Tel: +44 (0)20 3192 1733 |

Twitter https://twitter.com/BlencoweRes

LinkedIn https://www.linkedin.com/company/72382491/admin/

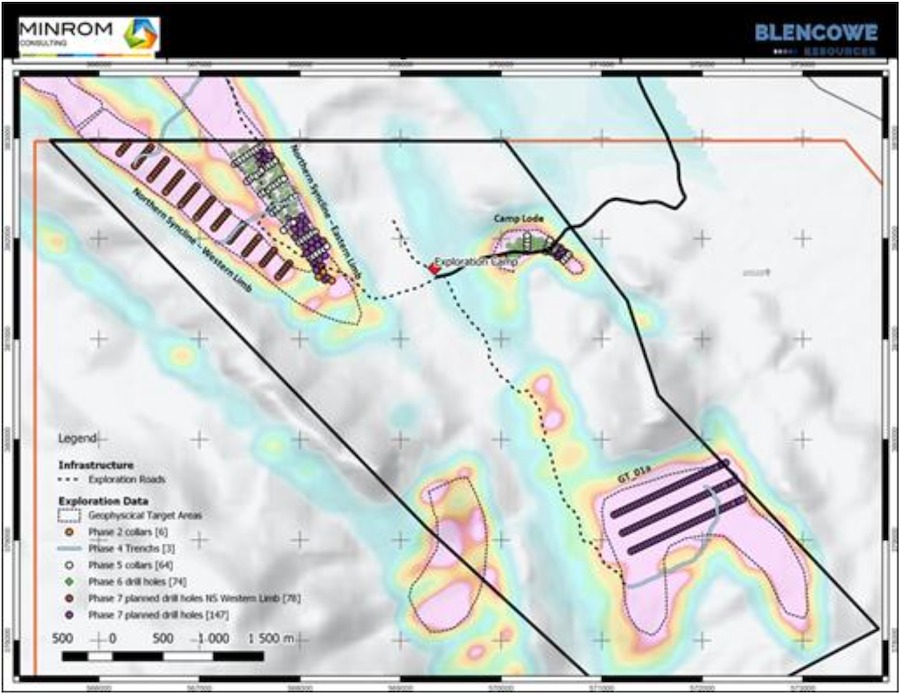

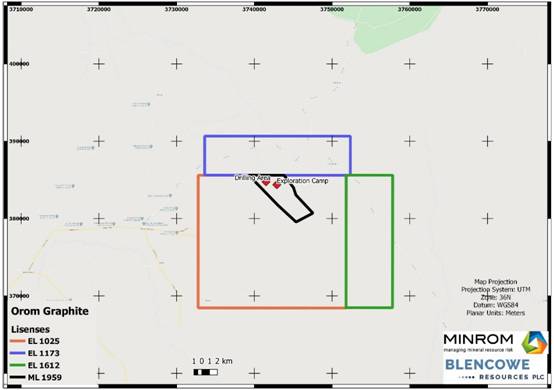

Map 1: Showing the 4x Orom-Cross deposits, including Camp Lode, Northern Syncline, and new Iyan (NS western limb) and Beehive (GT 01a) deposits.

#BRES Blencowe Resources PLC – Beehive Returns 92.55m @ 6.83% TGC from Surface

Blencowe Resources Plc (LSE: BRES) is pleased to report the first deep-hole assay results from the newly identified Beehive Deposit, located approximately 3kms from the existing Northern Syncline and Camp Lode deposits at the Orom-Cross graphite project in Uganda. Along with these other deposits Beehive sits within the existing Mining License (ML1959).

The Company is pleased to announce an exceptional drilling result from Beehive Deposit where early indications of a strong system have now been materially exceeded by the latest assay results from Hole L238B.

Hole L238B returned 92.55m (True Width) @ 6.83% TGC from surface to 120.60m, including multiple high-grade zones. This outstanding intercept confirms Beehive as a thick, continuous, near-surface graphite system and represents one of the most significant results generated at Orom-Cross to date.

This result is the first of over 100 Beehive holes to be reported, with further results to follow.

Beehive Deposit – Key Drill Result

Hole L238B: 92.55m (TW) @ 6.83% TGC [0.00-120.60m]

including:

· 15.89m @ 9.42% TGC

· 8.38m @ 10.95% TGC

Geological Interpretation

The intersection demonstrates continuous graphite mineralisation from surface, extending well beyond the ~30m oxide boundary and confirming strong grade continuity at depth. The thickness and consistency of mineralisation in Hole L238B significantly enhances confidence in the scale and robustness of the Beehive Deposit.

These results support the interpretation of Beehive as a large, laterally extensive system with the potential to materially contribute to future resource growth at Orom-Cross, sitting within the existing Mining License. Beehive is a new discovery with zero previous drilling to date.

Strategic Context

Global demand for secure, high-quality graphite supply continues to accelerate, with increasing focus from Western governments and industrial groups on securing critical mineral assets outside of China.

Recent engagement in the United States by senior management highlighted strong interest in scalable, long-life graphite projects ex-China, capable of supporting growing downstream supply chains. Orom-Cross, and Beehive in particular, displays many of the attributes sought by potential strategic and offtake partners, including scale, grade, near-surface mineralisation and substantial expansion potential.

Executive Chairman Cameron Pearce commented:

“We knew Beehive was shaping up as a promising system, however, the result from Hole L238B has exceeded all expectations. Delivering over 92 metres of continuous graphite mineralisation from surface at a strong average grade is an exceptional outcome and clearly demonstrates the scale potential emerging at Beehive.

This result sits within a substantial drilling programme that has now been completed across Beehive and the nearby Iyan deposit. Approximately 182 step-out and exploration holes have been drilled at both, with a steady flow of assays still pending from the laboratories, alongside the two additional Beehive deep drill holes underway. The results from this programme are expected to materially expand the mineralised footprint and support an updated JORC Mineral Resource Estimate in due course.

Following the Company’s recent £3.0 million fundraise we are well capitalised as we move into 2026, placing us in a strong position to maintain momentum across drilling, resource growth, early project implementation and ongoing strategic engagement following the completion of an outstanding DFS. We continue to see growing interest from potential offtake partners and expect these discussions to progress as the New Year unfolds.

As we approach the end of the year I would also like to thank shareholders, stakeholders and supporters of Blencowe for their continued support, and to wish everyone a happy holiday and festive season.”

For further information please contact:

|

Blencowe Resources Plc Sam Quinn |

www.blencoweresourcesplc.com Tel: +44 (0)1624 681 250 |

|

Investor Relations Sasha Sethi |

Tel: +44 (0) 7891 677 441 |

|

Tavira Financial Jonathan Evans |

Tel: +44 (0)20 3192 1733 |

Twitter https://twitter.com/BlencoweRes

LinkedIn https://www.linkedin.com/company/72382491/admin/

Map 1: Showing the 4x Orom-Cross deposits, including Camp Lode, Northern Syncline, and new Iyan (NS western limb) and Beehive (GT 01a) deposits.

Diagrams 1-3: Beehive Core

#BRES Blencowe Resources PLC – DFS Results Confirms Outstanding Economics

Blencowe Resources Plc (LSE: BRES) is pleased to announce results of the recently completed Definitive Feasibility Study (“DFS”) for its 100%-owned Orom-Cross graphite project in Uganda. The DFS assesses an initial 15 year Life of Mine (“LOM”); with only ~2% of the deposit drilled, the Company expects significant Life of Mine extensions as further drilling converts additional resources to reserves.

Blencowe Resources Plc (LSE: BRES) is pleased to announce results of the recently completed Definitive Feasibility Study (“DFS”) for its 100%-owned Orom-Cross graphite project in Uganda. The DFS assesses an initial 15 year Life of Mine (“LOM”); with only ~2% of the deposit drilled, the Company expects significant Life of Mine extensions as further drilling converts additional resources to reserves.

The DFS has been managed and signed off by Independent consultants, CPC Engineering (“CPC”), one of the world’s leading graphite technical experts responsible for feasibility work on tier-one developments such as ASX listed Syrah Resources’ Balama project and ASX listed Black Rock Mining’s Mahenge project.

The DFS showcases Orom-Cross as a Tier-1 graphite project, delivering strong margins from a low capital base, and incorporating a downstream beneficiation facility to produce uncoated spheronised purified graphite product (“USPG”) in-country.

Completion of this independent DFS marks the single most important technical milestone in the Company’s history and formally transitions Orom-Cross into the financing and development phase.

DFS Highlights:

· Net Present Value (NPV10): US$1.087 Billion

· Internal Rate of Return (IRR10): 96%

· All in Sustaining Costs (AISC): US$485/t over LOM (lowest quartile globally)

· Free Cash Flow: US$2.034 Billion over initial 15 years LOM

· Average Annual EBITDA: US$230 million per annum over LOM

· Phase 1 Production (“P1”): Smaller scale, fast-track operation targeting first production in 1H-2027 (20,000 tpa concentrate with micronised products)

· Downstream Value-Add: In-country beneficiation facility to produce purified graphite.

· Phase 2 Production (“P2”): Expansion to 70,000 tpa concentrate and 20,000 tpa USPG nearby.

· Scalability: Long-term pathway to 175,000 tpa concentrates and 80,000 tpa purified products.

· Offtake: Non-binding offtake agreements already in place for all planned P1 Production.

· Lowest Quartile Total Capital Requirement of US$160 million comprising:

o US$40 million for P1, delivering up to 20,000 tpa concentrate

o US$120 million for P2, lifting up to 70,000 tpa concentrate and up to 20,000 tpa USPG

o Significant contingency included within these capital estimates.

· All further expansions post-P2 to be funded entirely from internal cash flow

Project Strategy

Orom-Cross will commence with P1 Production, a smaller-scale, fast-track development delivering up to 20,000tpa of 96% TGC concentrates by 1H-2027. P1 is designed to be profitable from first production, materially reducing financial risk. Offtake agreements covering all planned P1 volumes are already in place.

With the DFS now complete, the immediate next step is securing the P1 project financing package, which becomes the Company’s primary corporate focus. This funding package will initiate ordering, construction and commissioning. Once P1 production begins and product quality is demonstrated at scale the Company expects additional offtake interest, particularly given the scarcity of new high-quality graphite projects coming online.

Within two years of P1 commissioning, Blencowe intends to implement P2 Production, expanding mine output up to 70,000tpa of concentrate. A downstream beneficiation facility will be built near to Orom-Cross to upgrade small flake concentrate to 99.95% TGC USPG, initially producing up to 20,000tpa. This facility will expand in sync with mine scale-up and will serve as a long-term captive offtaker for Orom-Cross concentrates over life of mine. This will position Orom-Cross among the few commercial-scale producers of 99.95% USPG outside of China, and the first in Africa.

Beyond P2 Production, Orom-Cross is expected to expand in stages toward 175,000tpa concentrate and 80,000tpa USPG, funded entirely by internally generated cash flow and marking a pathway to becoming an industry leading producer of both concentrates and high-value purified graphite, aligning with accelerating global demand for ex-China graphite supply.

Sales and Marketing

· Blencowe continues to use leading global graphite sales and marketing specialists, expanding commercial networks and progressing additional offtake opportunities.

· In 2025, 700 tonnes of Orom-Cross raw material was processed and bulk sample end products were delivered to graphite end users worldwide for extensive test work and evaluation.

· Non-binding offtakes covering all P1 volumes will convert to binding agreements on P1 financing.

· SAFELOOP (EU Gen3 battery initiative) volumes remains outside the DFS as the programme remains under development; however, a substantial additional Tier-1 offtake opportunity will likely emerge from 2028 onwards once SAFELOOP commercialises.

· Continued interest from battery, industrial and specialty-materials sectors reinforces the strategic importance of reliable, high-quality ex-China graphite supply.

Orom-Cross will continue to scale in line with contracted market demand, ensuring disciplined and commercially led expansion. Ongoing engagement with a broad global end-user network remains central to the expansion strategy.

Next Steps: Pathway to P1 Funding and First Production

Completion of the DFS provides Blencowe with a fully defined, independently verified and finance-ready project, marking the transition into the execution phase of development.

Together with its corporate advisor WaterBorne Capital, the Company is advancing a financing solution for P1 Production with active engagement underway with:

· Development finance institutions (DFIs)

· Strategic industry partners

· Institutional investors

· Government and quasi-government funding bodies

Several promising structures are under evaluation. Blencowe’s target is to secure P1 financing by end-1Q 2026, enabling ordering, shipping and construction through 2026, and first production targeted for 1H 2027.

Importantly, the Company expects P1 financing to be primarily funded through non-Blencowe plc equity structures. The combination of strong DFS economics, low capex, secured offtake and integrated downstream value-add support a balanced funding package designed to minimise plc equity dilution.

P2 financing is expected to adopt a more traditional debt-plus-strategic-partner approach. With the DFS complete, formal engagement will now begin with groups that have shown interest, including the US Development Finance Corporation (DFC), the African Finance Corporation (AFC), and other Tier-1 institutions. P2 financing will run in parallel with P1 execution, supporting a rapid scale-up to commercial production.

All expansions beyond P2 are expected to be funded entirely from internally generated cash flow. Blencowe believes that demand for all its products will rise substantially over the next few years, especially once Orom-Cross is in production, and the Company needs to prepare for scaled growth.

SPG Beneficiation Facility

The downstream graphite beneficiation facility will be constructed near Gulu, approximately 150 kms from Orom-Cross and adjacent to existing hydropower infrastructure. The facility will:

· Process Orom-Cross concentrate into battery-ready 99.95% TGC USPG.

· Utilise low-cost, renewable hydroelectricity available through Ugandan national grid.

· Produce both high-value USPG and saleable by-products.

· Expand modularity in line with mine output.

· Function as a long-term captive offtaker for up to 50% of Orom-Cross concentrate (small flake concentrate).

This integrated upstream-downstream model positions Blencowe as one of the very few ex-China suppliers capable of providing high-specification purified graphite to global battery and industrial markets.

Key Performance Indicators

The following represents the KPIs for Orom-Cross initial operations as envisaged within the DFS:

|

KPI |

Value |

Comments |

|

Initial Life of Mine |

15 years |

Further infill drilling will extend this LOM substantially |

|

NPV10 |

US$1.087 Bn |

Compares favourably to PFS (NPV8 US$482M) including a higher discount rate used Incorporates both Orom-Cross and downstream beneficiation facility |

|

IRR10 |

96% |

Strong IRR indicates significant returns on capital |

|

Capital required – P1 Production

Capital required – P2 Production |

US$40M

US$120M |

Initially produce up to 20,000tpa concentrate and micronised products Ramp up to 70,000tpa concentrate and up to 20,000tpa USPG Most key infrastructure already at site |

|

Average Operating cost over LOM (AISC) |

US$485/t |

Lowest quartile costs in graphite market ensures less dependency on graphite prices having to increase for success |

|

Average Selling price over LOM |

US$1,240/t US$2,310/t |

Average for all concentrates sold from Orom-Cross Average for USPG and waste sold from beneficiation facility |

|

Average annual production over LOM |

97,000tpa 56,500tpa |

All concentrates from Orom-Cross Uncoated spheronised purified graphite (USPG) |

|

Average EBITDA over LOM |

US$230M pa |

High profitability once commercial scale is reached |

|

Net Free Cash over LOM |

US$2.034 Bn |

Significant free cash delivered from full project with mine life likely to extend well beyond the initial 15 years |

Capital Comparison (PFS vs DFS)

Whilst the full capital requirement has risen since the PFS (2022) there are several important factors to consider in making comparisons:

· Orom-Cross will have a smaller, lower risk initial phase (P1) production which was not part of the PFS scope.

· Orom-Cross will deliver 70,000tpa concentrates by P2 in the DFS, versus 50,000tpa at startup within the PFS.

· The DFS includes micronisation plant and equipment which was not part of the PFS scope.

· The DFS also incorporates a 20,000tpa downstream beneficiation facility, compared to zero downstream production in the PFS.

· Inflation since 2022 has increased capital and operating cost inputs across the sector.

Despite these factors, Orom-Cross delivers a significantly more profitable operation for the capital deployed, as demonstrated by the increase in valuation metrics:

· NPV10: US$1.087Bn in DFS vs NPV8: US$482M in PFS

· IRR10 96% in DFs vs 49% in PFS

· Higher discount rate used in (10% DFS versus 8% PFS)

Project Benchmarking

Orom-Cross compares extremely favourably with global graphite peers, demonstrating:

· Lowest-quartile capital and operating costs.

· Robust margins and over US$2 billion in free cash flow over initial 15-year mine life.

· With only ~2% of the licence drilled, substantial additional reserve growth and life of mine extensions is anticipated as new graphite deposits are incorporated.

· Premium product quality supporting strong pricing and long-term demand.

A further updated JORC resource is anticipated in 1Q 2026, incorporating results from an additional 192 step-out holes, including new deposits at Iyan and Beehive.

De-Risking

The DFS together with its world class KPIs, materially de-risks Orom-Cross across technical, financial and commercial dimensions. All capital and operating assumptions have been generated using current input costs validated by technical experts CPC Engineering.

Local infrastructure is largely already in place, and preparatory works can begin immediately following completion of P1 financing.

Non-binding offtake agreements cover all planned P1 Production and these will transition to binding status post-financing. Additional offtake interest is expected post-DFS, particularly given the diverse mix of Western and Asian end-users currently testing Orom-Cross products, including Tier-1 groups such as US DoW, and the EU SAFELOOP initiative.

The Company’s Community Agreement and strong Ugandan Government support provide a stable local operating platform, and key technical relationships (AET, TaiDa Graphite, ADT and others) remain in place, while Orom-Cross’s Minerals Security Partnership accreditation continues to support engagement with strategic funders and offtakers.

As the project advances toward construction, Blencowe will expand its executive and operational teams to support the transition to P1 production.

Market Outlook

Blencowe believes that demand for natural flake graphite, particularly high-purity anode material such as that produced at Orom-Cross and the SPG facility, will grow materially over the medium term. Graphite remains an essential, non-substitutable component of lithium-ion batteries used for energy storage and EVs. Supply is forecast to tighten sharply as global decarbonisation accelerates.

Orom-Cross is exceptionally well positioned as a near-term producer with a defined development pathway. Once in production, the Project will be highly leveraged to rising graphite prices, with its low operating costs ensuring strong margins across a wide range of market conditions. Any future supply deficits or price increases would further amplify the already robust DFS economics.

With a diverse network of relationships across Western and Asian markets, Blencowe intends to prioritise niche and premium applications to maximise returns – a strategy that will strengthen further as purified USPG output commences. The Project also benefits from additional drilled but undeveloped deposits (Beehive and Iyan) that can be rapidly converted to support higher production if required.

Cameron Pearce, Executive Chairman commented:

“I would like the thank the entire Blencowe team and all our associated consultants for their exceptional work over the past two years to deliver this outstanding DFS. Achieving such strong NPV and IRR metrics from a relatively low capital base is a world-class outcome. It is rare to see a project with such consistently strong fundamentals across scale, cost structure, margins and downstream potential.”

“This Study marks a transformational moment for Blencowe clearly demonstrating the scale, quality and longevity of Orom-Cross as we move into the financing and development phase. The DFS confirms Orom-Cross as a Tier-1 graphite project and our focus now turns to the financing process and delivering first production as our next major goals.”

“With the Project now considerably de-risked, graphite markets improving, and a clear pathway to become a major ex-China supplier, we believe Blencowe is exceptionally well positioned for a meaningful re-rating as investors realise the scale of the opportunity ahead.”

For further information please contact:

|

Blencowe Resources Plc Sam Quinn |

www.blencoweresourcesplc.com Tel: +44 (0)1624 681 250

|

|

Investor Relations Sasha Sethi |

Tel: +44 (0) 7891 677 441

|

|

Tavira Financial Jonathan Evans |

Tel: +44 (0)20 3192 1733

|

Twitter https://twitter.com/BlencoweRes

LinkedIn https://www.linkedin.com/company/72382491/admin/

#BRES BLENCOWE RESOURCES – Warrant Exercises Raises Approx £550,000

The Company has received notices to exercise 1,666,666 warrants at an issue price of 4.5p each resulting in the receipt of £75,000. The Company will issue a total of 1,666,666 New Ordinary Shares.

The Company has received notices to exercise 1,666,666 warrants at an issue price of 4.5p each resulting in the receipt of £75,000. The Company will issue a total of 1,666,666 New Ordinary Shares.

The Board welcomes the continued exercise of warrants, which has raised approximately £550,000 since October to date. This additional capital supports ongoing workstreams and enhances our position as we finalise the DFS and advance discussions on project financing.

Admission

The Company will make an application for 1,666,666 New Ordinary Shares to be admitted to trading on the Equity Shares (transition) category of the Official List and the Main Market of the London Stock Exchange at 8.00 a.m. on 19 November 2025.

Total Voting Rights

The Company hereby notifies the market, in accordance with the FCA’s Disclosure Guidance and Transparency Rules, that on Admission, the Company’s enlarged share capital will consist of 392,187,908 Ordinary Shares, each with one vote. The Company does not hold any Ordinary Shares in Treasury. On Admission, the total number of voting rights in the Company is expected to be 392,187,908 and this figure may be used by Shareholders as the denominator for the calculations by which they will determine if they are required to notify their interest in, or a change to their interest in, the Company under the FCA’s Disclosure Guidance and Transparency Rules.

|

Blencowe Resources Plc Sam Quinn |

www.blencoweresourcesplc.com Tel: +44 (0)1624 681 250 |

|

Investor Relations Sasha Sethi |

Tel: +44 (0) 7891 677 441 |

|

Tavira Financial Jonathan Evans |

Tel: +44 (0)20 3192 1733 |

#SVML Sovereign Metals LTD – Lapse of Performance Rights and September 2025 Quarterly Report

LAPSE OF PERFORMANCE RIGHTS

LAPSE OF PERFORMANCE RIGHTS

Sovereign Metals Limited (ASX:SVM; AIM:SVML; OTCQX:SVMLF) (Sovereign or the Company) advises that 10,977,500 unlisted performance rights that were subject to the “Definitive Feasibility Study Milestone” have lapsed today without exercise or conversion.

Following the lapse of these unlisted performance rights, the Company has the following securities on issue:

· 646,938,703 fully paid ordinary shares (of no par value);

· 4,992,500 unlisted performance rights subject to the “Grant of Mining Licence Milestone” expiring on or before 31 March 2026; and

· 6,190,000 unlisted performance rights subject to the “Final Investment Decision Milestone” expiring on or before 30 June 2026.

Change of Directors’ Interest Notices in relation to the lapse of unlisted performance rights have been provided below.

Link here to view the full announcement

Sovereign Metals Limited (ASX:SVM, AIM:SVML, OTCQX:SVMLF) (Sovereign or the Company) is pleased to provide its quarterly report for the period ended 30 September 2025 including advances made at its Kasiya Rutile-Graphite Project (Kasiya or the Project) in Malawi.

HIGHLIGHTS DURING AND SUBSEQUENT TO THE QUARTER

Japanese Government Launches New Nacala Logistics Corridor Development Initiative

· Japan commits US$7 billion in development funding – $5.5 billion through joint program with African Development Bank, plus $1.5 billion in public-private impact investment through Japan’s development agency.

· Initiative focuses on capacity expansion, refurbishment, and resilience upgrades to increase throughput, enhance reliability, and reduce bottlenecks, positioning Kasiya as a key beneficiary of Japan’s mineral security strategy.

· Nacala Corridor is Kasiya’s preferred transport route – providing lowest-cost pathway from Kasiya to international markets via a deep-water port.

Various Critical Components of DFS now complete

· Geotechnical investigations successfully completed across all critical infrastructure locations with oversight from the Sovereign-Rio Tinto Technical Committee confirming favourable subsurface conditions aligned with regional geology

o Over 400 individual tests conducted covering mining infrastructure, tailings storage facility and raw water dam

o Consistent stratigraphy and suitable subsurface conditions to enable more standardised foundation designs and construction approaches across infrastructure areas

· Mining fleet specifically engineered for large-scale dry mining operations following the results of the successful Pilot Mining and Land Rehabilitation (Pilot Phase).

o No drilling, blasting, crushing or milling required at Kasiya resulting in low capital outlays and operating costs.

o Equipment selection and supplier identification completed for all operational requirements across the proposed initial 25-year mine life

· Rehabilitation of land at Pilot Phase test pit site successfully completed during the quarter, further de-risking DFS

o Exceptional first-year results from its rehabilitation trials at the Kasiya, delivering critical data that will inform the progressive rehabilitation strategy for the ongoing definitive feasibility study (DFS).

o Rehabilitation trials achieved 5x crop yield improvement – demonstrating superior post-mining land productivity versus traditional farming.

New Graphite Tariff Environment Underscores Kasiya’s Global Significance

· In July 2025, the U.S. Commerce Department announced 93.5% preliminary anti-dumping duties on Chinese graphite imports, fundamentally altering the economics for battery manufacturers seeking secure, cost-competitive supply chains.

· The new tariff environment highlights Kasiya’s potential as the world’s largest and lowest-cost non-Chinese graphite producer with industry-leading US$241/t incremental cost of production.

Latest Testwork Validates Kasiya Graphite’s World-Class Quality to Anode Manufacturers

· Latest coating optimisation testwork achieved successful coated spherical purified graphite (CSPG) production characteristics with superior performance metrics.

· Samples of Kasiya fine flake graphite concentrate have been distributed to leading natural graphite anode producers and anode project developers to support development of offtake agreements while validating market demand for Kasiya’s high-quality battery-grade graphite

Kasiya Unaffected by Malawi Raw Mineral Export Order

· Subsequent to the quarter, His Excellency President Peter Mutharika, the newly elected President of Malawi, announced an Executive Order regarding the prohibition of the export of raw minerals from the country.

· This prohibition does not apply to the Company or to Kasiya as the ban only relates to minerals that have not been processed, refined, or value-added in Malawi.

o With regards to its future planned Kasiya operations, Sovereign has no plans to export run-of-mine Heavy Mineral Sands as defined in the Executive Order. All future mineralisation will be extracted and beneficiated in country to a final premium quality rutile (+95% TiO2) product. The high-quality Kasiya rutile product is planned to be a direct feedstock for titanium sponge production for high-end titanium metal products, including aerospace and defence applications.

o Similarly, Sovereign intends to process the run-of-mine Graphite as defined in the Executive Order in-country to produce a high-quality graphite product (96% C) suitable for major industry end markets including battery producers and refractory manufacturers.

Next Steps

Over the quarter ending December 2025, Sovereign will:

· continue to advance the Kasiya DFS, for completion in the first quarter of 2026, including finalising mining fleet design, process plant configuration, and mine gate-to-vessel logistics solutions;

· advance rutile and graphite offtake discussions; and

· further the Company’s community and social development programs in Malawi.

|

Enquiries |

|

|

Frank Eagar, Managing Director & CEO South Africa / Malawi +27 21 140 3190 |

|

|

Nominated Adviser on AIM and Joint Broker |

|

|

SP Angel Corporate Finance LLP |

+44 20 3470 0470 |

|

Ewan Leggat Charlie Bouverat |

|

|

|

|

|

Joint Broker |

|

|

Stifel |

+44 20 7710 7600 |

|

Varun Talwar |

|

|

Ashton Clanfield |

#GRX GreenX Metals LTD – GreenX Uncovers Historical Estimate at Tannenberg

HIGHLIGHTS

· 1940 Historical Estimate of Significant Scale: Historical Estimate from 1940 identifies 728,000 tonnes contained copper (1,605 Mlbs) at an average grade of 2.6% copper in part of Tannenberg Project licence area discovered from original project data archives

o Estimate based on a 1935-1938 National Socialist Government drilling campaign across four zones: Ronshausen, Hönebach, Wolfsberg and Schnepfenbusch

o Drilling targeted the thin Kupferschiefer horizon only

o Focused only on copper and did not include by-product metals

· 1984 Historical Estimate provides Validation: Independent company St Joe Exploration GmbH conducted limited drilling between 1980 and 1984, further validating the 1940 historical estimate

o Drilling focused on only 28% of the Ronshausen zone but included by-product silver

o Drilling identified up to 3.45m thick mineralisation straddling the Kupferschiefer and the limestone hanging wall and sandstone footwall above and below the Kupferschiefer

o 1984 historical estimate shows consistent grades of 2.1% copper plus 25 g/t silver with 169,000 tonnes of contained copper and 6.5 million ounces of silver

· Exploration Upside Potential under Modern Interpretation: St Joe Exploration confirmed thicker widths of copper and silver mineralisation at Ronshausen, and more may exist up to 30m above and 60m below the Kupferschiefer in the limestone hanging wall and sandstone footwall

o Hypothesis is consistent with modern understanding of the Kupferschiefer deposit model as demonstrated at KGHM’s Polish mining operations which are also found on the same geological structure as the Tannenberg Project

· Active Exploration Program: GreenX is currently relogging and resampling over 4km of archived core from 47 holes to upgrade historical data to modern standards

o Investigation of German mining archives and the digitisation of original historical data continues

o Planning of future twin drilling campaign to verify the historical estimates, and to establish a mineral resource estimate in accordance with the JORC Code (2012) (JORC Code)

· Cautionary statement: The historical estimates in this announcement are not reported in accordance with the JORC Code. A competent person has not done sufficient work to classify the historical estimate as a mineral resource or ore reserve in accordance with the JORC Code. It is uncertain that following evaluation and/or further exploration work that the historical estimate will be able to be reported as a mineral resource or ore reserve in accordance with the JORC Code.

GreenX Metals Limited (ASX:GRX, LSE:GRX, GPW:GRX, Germany-FSE:A3C9JR) (GreenX or Company) is pleased to announce that through its ongoing search of original archive data, the Company has identified a historical estimate of 728,000 contained tonnes of copper (1,605 Mlbs) at an average grade of 2.6% Cu from the Tannenberg Copper Project (Tannenberg or Project) dating from 1940 (1940 historical estimate). The 1940 historical estimate was produced by the German company Mansfeldsche Kupferschieferbergbau AG (Mansfeld AG) and is based on the 95-drill hole exploration campaign carried out during the late 1930s (refer to announcement dated 11 September 2025).

In addition, a later historical estimate from 1984 was produced by St Joe Exploration GmbH (St Joe), which covers a small part of the same area as the 1940 historical estimate (St Joe’s historical estimate).

The St Joe’s historical estimate is based on limited drilling between 1980 and 1984 (refer to announcements dated 2 August 2024 and 28 April 2025). St Joe’s historical estimate provides further validation for the 1940s historical estimate.

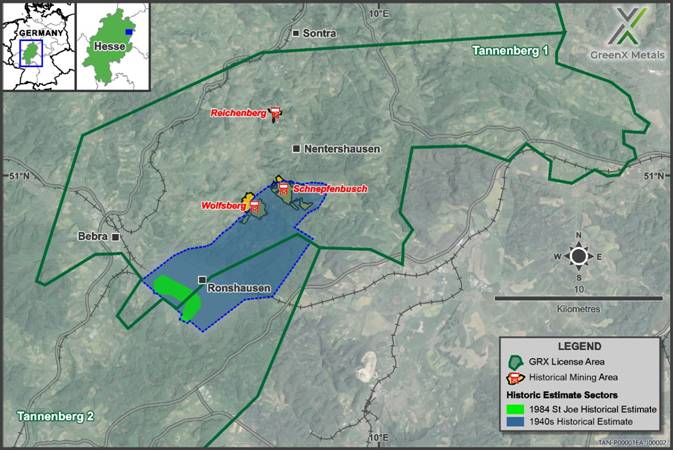

Figure 1: Map showing the location of the zones of the historical estimates and historical mining operations

GreenX’s Chief Executive Officer, Mr Ben Stoikovich, commented: “This represents a significant breakthrough in our archive search and fundamentally supports our exploration hypothesis of the Tannenberg mineral system. It demonstrates that extensive copper mineralisation was identified historically, but exploration at the time was constrained by the prevailing geological model, which focused solely on the thin Kupferschiefer shale and the urgent need to mine given the outbreak of World War II. The 1940 historical estimate, based on a narrow-mineralised interval and excluding by-product silver, was further validated by the 1984 work and modern understanding from Poland’s Kupferschiefer mining operations, together confirming that copper mineralisation extends beyond the Kupferschiefer horizon and providing major proof of concept and clear alignment with GreenX’s geological model. The implications are substantial, reinforcing the potential for a large-scale and high-grade brownfield copper project at Tannenberg, and underscoring the project’s significance as a major European copper opportunity.”

1940 MANSFELD HISTORICAL ESTIMATE

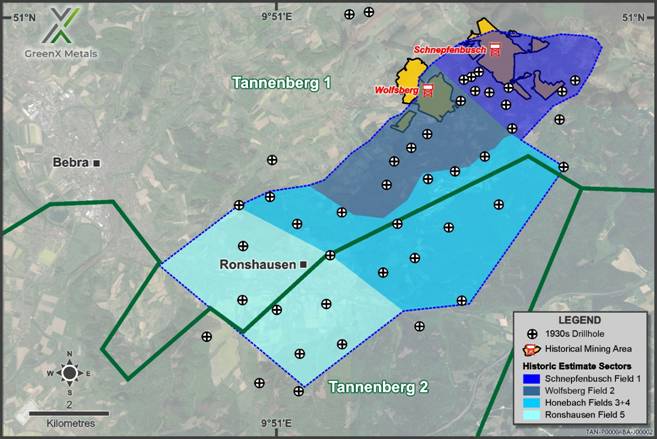

The 1940 historical estimate was calculated by Mansfeld AG according to the relevant German standards applicable during that time. The 1940 historical estimate is based on 18 holes from the 95-hole database generated during the 1935 to 1938 drilling campaign. The original archive document established 728,000 tonnes of contained copper at an average grade of 2.6% copper between the Wolfsberg and Schnepfenbusch mines in the North and the Ronshausen area in the South (Figure 2). The historical estimate covers mineralisation from a depth of 100m in the North to 400m in the Southern end area near Ronshausen.

The 1940 historical estimate covers only the narrow width Kupferschiefer shale mineralisation, which is notable due to the mistaken belief at the time that copper was only present in the distinctive Kupferschiefer shale. Later exploration campaigns have found mineralisation over much wider thicknesses (see 1984 St Joe’s historical estimate section below). This is consistent with GreenX’s exploration hypothesis that historical exploration was mainly based on an outdated deposit model that focused on the 20-60 cm-thick Kupferschiefer shale horizon. The modern understanding of the Kupferschiefer deposit model now shows that up to 95% of mineable copper can be hosted in the footwall sandstone and hanging wall limestone, as evidenced at KGHM Polska Miedź S.A’s Polish mining operations.

Figure 2: Map showing the locations of the zones of the 1940 historical estimate, related drill holes and historical mining operations

It is also noteworthy that the 1940 historical estimate did not include by-product silver mineralisation. The majority of the mineralisation (463,000 tonnes of contained copper) was found to be present in the Ronshausen region, with gradually decreasing amounts to the North, where the historical mining is to be found (See Table 1).

|

Table 1: Summary of Historical Estimate information from the original 1940 Mansfeld report |

||||

|

Zone |

Surface Area |

Thickness (cm) |

Grade Cu |

Contained Copper |

|

Ronshausen |

10,000,000 |

67.4 |

2.85 |

463,000 |

|

Hönebach |

8,088,000 |

34.2 |

1.92 |

130,055 |

|

Wolfsberg |

6,468,000 |

23.5 |

2.35 |

92,945 |

|

Schnepfenbusch |

5,528,000 |

19.3 |

2.38 |

65,673 |

|

SUB-TOTAL |

|

|

2.59 |

751,673 |

|

Less historical production |

(23,793) |

|||

|

TOTAL |

|

|

|

727,880 |

Cautionary statement: The historical estimates in this announcement are not reported in accordance with the JORC Code. A competent person has not done sufficient work to classify the historical estimate as a mineral resource ore reserve in accordance with the JORC Code. It is uncertain that following evaluation and/or further exploration work that the historical estimate will be able to be reported as a mineral resource ore reserve in accordance with the JORC Code.

The 1940 historical estimate data provides a good level of transparency with regard to the input data and the calculation methods used. The estimation resulting from the drill hole data was cross-checked by Mansfeld AG against the production grades at the Wolfsberg and Schnepfenbusch mines, which were operating in the area at the time of 1940 historical estimate. The comparison was favourable, and hence the assays from the exploration holes were used. GreenX has reviewed original records covering 17 of the 18 holes (~95%) used for the historical estimation and found no discrepancies.

Mansfeld AG made specific adjustments as part of the 1940 historical estimate to account for sterilisation. A total of 250,000 tonnes of contained copper was omitted to account for areas where surface features might prevent mining. Mansfeld AG also estimated that a further 23,793 tonnes of contained copper had already been extracted by mining at Wolfsberg and Schnepfenbusch (at a production grade of 2.2% Copper). This amount was then subtracted from the historical estimate, as presented in the original source document (refer Table 1 above).

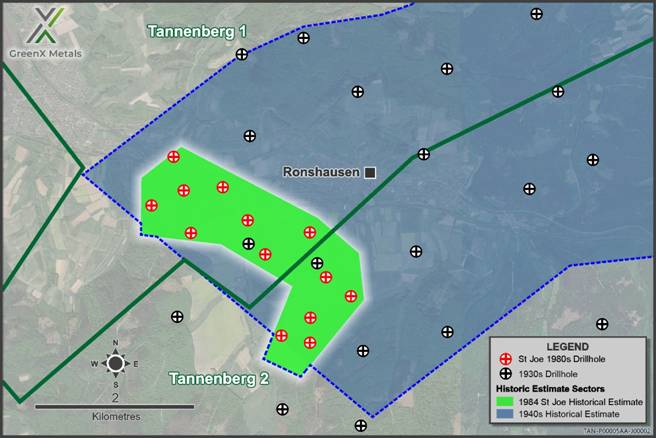

1984 ST JOE’S HISTORICAL ESTIMATE

Part of the Ronshausen zone of the 1940 historical estimate was drilled by St Joe Exploration during the 1980’s, resulting in recognition of the St Joe’s historical estimate more than 40 years later. Of the many holes drilled by St Joe, a total of 14 holes were used in the estimate of 169,000 of contained copper and 6.5 million ounces of contained silver. The St Joe’s work estimated grades of 2.1 % copper and 25 g/t silver at typical depths between 290 and 370m (Figure 3).

St Joe benefited from both technological advancements and enhanced geological understanding in the 40 years following the work by Mansfeld AG. Consequently, St Joe assayed wider intersections and found that the mineralisation was up to 3.45m width. The historical estimate was calculated using thicknesses of between 1.5 to 2m, considerably thicker than the narrow Kupferschiefer assayed and estimated by Mansfeld AG in 1940.

Figure 3: Map showing the drill holes and locations of the Ronshausen zone of the 1940 historical estimate and the relative location of the 1984 St Joe’s historical estimate

Given the increased mineralisation thickness covered by St Joe and the fact that the drilling covered only 28% of the Ronshausen zone, the St Joe’s historical estimate further validates the 1940 historical estimate. The identification of much thicker mineralisation and contained silver also points to considerable exploration upside over all five mineralisation zones covered by the 1940 historical estimate.

Cautionary statement: The historical estimates in this announcement are not reported in accordance with the JORC Code. A competent person has not done sufficient work to classify the historical estimate as a mineral resource or ore reserve in accordance with the JORC Code. It is uncertain that following evaluation and/or further exploration work that the historical estimate will be able to be reported as a mineral resource or ore reserve in accordance with the JORC Code.

1930s DRILLING CAMPAIGN

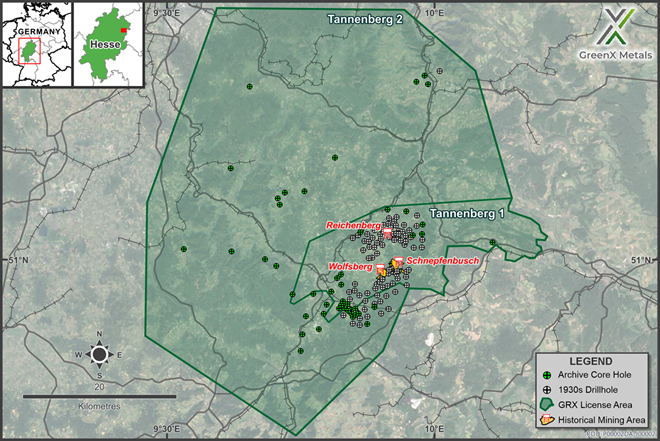

The 18 holes used in the 1940 historical estimate were drilled between 1935 and 1938 (Figure 4). The southern holes tested the downdip continuation of known Kupferschiefer mining sites from the mid-1800s and led to the opening of the Wolfsberg and Schnepfenbusch mines. In the northern area, the drilling discovered previously unknown down-faulted Kupferschiefer that does not outcrop and had not been previously exploited. This discovery led to the opening of the Reichenberg mine.

GreenX recently found the majority of the relevant original records of these drill holes in a regional archive. To date, of the 95 holes indicated to exist in the 1930s database, the Company has found logs for 43 holes, and of those, original historical assay results have been found for 35 holes. GreenX is continuing the archive search whilst digitising the records to add to the geological database for the Project.

Drilling up to 95 holes today is estimated to cost over €25 million and take several years, given modern permitting requirements. The discovery of the original historical drill database and 1940 historical estimate not only represents a significant saving in both time and money for GreenX, but it also provides valuable data points for its current exploration work program, including exploration targeting and 3D modelling. Combined with the 47 drill cores GreenX is currently re-logging and sampling (Figure 4), the quantity of previous exploration data available at Tannenberg is quickly growing, and underscores Tannenberg as a significant brownfield exploration opportunity.

Figure 4: Location Map of GreenX’s Tannenberg project area showing the newly discovered 95 x 1930s drillholes, the location of the three underground copper/ silver mines opened during the late 1930s, and the location of the modern era 47 archive core holes that GreenX now has access to for re-logging and sampling

Upcoming Work Programs

The discovery of this historical estimate and the National Socialist era drill database is part of the Company’s continued search for original historical mining and production data in German archives, which are part of a broader exploration program at Tannenberg, which includes:

· Logging, assaying, and hyperspectral scanning of historical core (ongoing);

· Reprocessing and analysis of historical geophysical data (ongoing);

· Collation of historical geological, mine development, and production data (ongoing); and

· Airborne magnetic and radiometric survey (results released in September 2025)

In light of the discovery of this significant upgrade in the understanding of the Tannenberg mineralisation, GreenX is planning a future twin drilling campaign to verify the historical estimates, in order to establish a mineral resource estimate in accordance with the JORC Code.

ENQUIRIES

|

+44 207 478 3900 ir@greenxmetals.com |

Sapan Ghai Chief Commercial Officer – UK

|

|

Kim Eckhof Investor Relations – UK / Germany

|

Kazimierz Chojna Investor Relations – Poland

|

Competent Person Statement – HISTORICAL Estimate

The information in this announcement that relates to historical estimates is based on information reviewed and compiled by Dr Matt Jackson, a Competent Person who is a member of the Australian Institute of Mining and Metallurgy. Dr Jackson is a Technical Consultant for GreenX and is a holder of unlisted options in the Company. Dr Jackson has sufficient experience that is relevant to the style of mineralisation and type of deposit under consideration and to the activity being undertaken, to qualify as a Competent Person as defined in the 2012 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Dr Jackson consents to the inclusion in this announcement of the matters based on his information in the form and context in which it appears. Dr Jackson confirms that the information provided under ASX Listing Rules 5.12.2 to 5.12.7 is an accurate representation of the available data and studies relating to the Tannenberg Copper Project.

Forward Looking Statements

This release may include forward-looking statements, which may be identified by words such as “expects”, “anticipates”, “believes”, “projects”, “plans”, and similar expressions. These forward-looking statements are based on GreenX’s expectations and beliefs concerning future events. Forward looking statements are necessarily subject to risks, uncertainties and other factors, many of which are outside the control of GreenX, which could cause actual results to differ materially from such statements. There can be no assurance that forward-looking statements will prove to be correct. GreenX makes no undertaking to subsequently update or revise the forward-looking statements made in this release, to reflect the circumstances or events after the date of that release.

The information contained within this announcement is deemed to constitute inside information as stipulated under the Regulation 2014/596/EU which is part of domestic law pursuant to the Market Abuse (Amendment) (EU Exit) Regulations (SI 2019/310) (“UK MAR”). By the publication of this announcement via a Regulatory Information Service, this inside information (as defined in UK MAR) is now considered to be in the public domain.

REFERENCES

Mansfeldsche Kupferschieferbergbau AG. (1940). On the development of the Richelsdorf area. In German. State archive of Saxony Anhalt Region (Merseburg)*

St Joe Exploration GMBH. (1984) A Final report on the activities of St Joe Explorations GMBH in the Kupferschiefer project, Richelsdorf 1984. Archive No 17. PO BOX, 5780, 3000 Hannover 1.*

*English translation of the original source document

SCHEDULE 1 – HISTORICAL ESTIMATE

Details of Non-JORC Historical Estimates in relation to ASX Listing Rule Chapter 5

Listing Rules 5.10 to 5.12: Requirements applicable to reports of historical estimates of mineralisation for material mining projects:

|

5.10 – An entity reporting historical estimates or foreign estimates of mineralisation in relation to a material mining project to the public is not required to comply with rule 5.6 of the JORC Code) provided the entity complies with rules 5.12, 5.13 and 5.14 |

For the Non-JORC historical estimate included in this market release, GreenX is not required to comply with Listing Rule 5.6 of the JORC Code as all relevant and requested disclosures are stated in this announcement and tabulated below. The Company complies with Listing Rule 5.12 requirements for the statement of Non-JORC historical estimates, as discussed below. |

|

5.11- An entity must not include historical estimates or foreign estimates (other than qualifying historic estimates) of mineralisation in an economic analysis (including a scoping study, preliminary feasibility study, or a feasibility study) of the entity’s mineral resources and ore reserves holdings. |

GreenX is not applying any economic analysis or commentary to the historical estimates in this Announcement. The historical estimates should not be relied upon for any economic evaluation. |

|

5.12 – Subject to rule 5.13, an entity reporting historical estimates or foreign estimates of mineralisation in relation to a material mining project must include all of the following information in a market announcement and give it to ASX for release to the market: |

|

|

5.12.1 – The source and date of the historical estimates or foreign estimates. |

On the 2 January 1940 a historical estimate was estimated by Mansfeldsche Kupferschieferbergbau AG (Mansfeld AG). The original source document was discovered by GreenX in the archive of the Saxony Anhalt Region of Germany located in Merseburg. In 1984, a historical estimate was created by St Joe Explorations GMBH. The original source document was found in archives of the Hessian Agency for Nature Conservation, Environment and Geology. The original data (drillhole logs and assays) for the historic estimates were found across various mining archives in Germany. |

|

5.12.2 – Whether the historical estimates or foreign estimates use categories of mineralisation other than those defined in Appendix 5A (JORC Code) and if so, an explanation of the differences. |

No resource category or reporting code was quoted as the practice of the reporting codes was only introduced in Germany in the 1990’s and common practice from the 2000’s onwards.. The 1984 St Joe’s historical estimate uses categories which were not used in this announcement to avoid inadvertent comparison with similar terms used in the JORC Code. The historical estimate figures used in this announcement are referred to by St Joe as “geological reserve” whereas in accordance with the JORC Code, the term “reserve” could only be used after quantitative assessment of modifying factors. The historical estimates were made prior to the JORC Code reporting guidelines being formulated and do not conform to the requirements in the JORC Code. |

|

5.12.3 – The relevance and materiality of the historical estimates or foreign estimates to the entity. |

The historical estimates are both material and relevant to the Tannenberg Project and Company, as they indicate the project’s scale while supporting the view that further exploration is warranted to evaluate the mineralisation in accordance with the JORC Code. Further, the historical estimate for the Tannenberg Project lie within the Tannenberg 1 and Tannenberg 2 exploration licences and are relevant to understanding the extent of mineralisation and copper grades present at the project. The original historical estimate documents also detail the results of an exploration program and historical estimates that were used to justify the establishment of mining operations in the 1940s. The information is material due to GreenX’s statutory obligation to release information that affects the understanding and prospectivity of the Tannenberg Project and any potential unmined mineralisation present. The information gained will be central to guiding future mineral exploration to develop the project. |

|

5.12.4 – The reliability of the historical estimates or foreign estimates, including by reference to any of the criteria in Table 1 of Appendix 5A (JORC Code) which are relevant to understanding the reliability of the historical estimates or foreign estimates. |

The historical estimates are not reported in accordance with the JORC Code. A competent person has not completed sufficient work to classify the historical estimates as a Mineral Resource Estimate in accordance with JORC Code 2012. The Estimates were made prior to the JORC Code 2012 reporting guidelines being formulated and do not conform to the requirements in the JORC Code 2012. Of the 18 holes used for the 1940 historical estimate, GreenX has found details of 17 holes and assays in various archives across Germany. These independently identified records confirm the grades and locations used in the estimate. The 1940 historical estimate validated the drill hole grades used in the estimate by comparing them with production grades from the Schnepfenbusch and Wolfsberg mining operations. The comparisons were favourable and confirmed the grades used in the historical estimate. A map of the 1940 historical estimate zones was reportedly attached to the original document, this has not been found by GreenX. GreenX has independently calculated the surface area of each of the estimate zones based on drill hole locations and the text description and the results match the estimation work performed in 1940. The German language 1940 estimate was translated by an online translation tool and was separately read and summarised by a specialist native German speaker. The human German speaker was not aware of the online translation. Both summaries were independent of each other and all key facts matched. The Company has completed a Table 1 of Appendix 5A (JORC Code) which are relevant to understanding the reliability of the historical estimates. Please refer below. GreenX is not treating the historical estimates as a Mineral Resource Estimate or Ore Reserve and considers the historical estimates to represent an exploration project that requires verification. However, nothing has come to the attention of the Company or the Competent Person that causes it to question the accuracy or reliability of the historical estimate and it is on this basis that the Company and Competent Person consider the historical estimates to be reliable. However, the Company and Competent Person has not independently validated the historical estimates and therefore is not to be regarded as reporting, adopting or endorsing the historical estimate. It is possible that following evaluation and/or further exploration work the currently reported historical estimates may materially change and at this point the Company will need to be update the reporting in accordance with the JORC Code (or it may never become reportable at all in accordance with the JORC Code). |

|

5.12.5 – To the extent known, a summary of the work programs on which the historical estimates or foreign estimates are based and a summary of the key assumptions, mining and processing parameters and methods used to prepare the historical estimates or foreign estimates. |

Refer to the “1930’s drilling campaign” and 1984 St Joe’s historical estimate sections of this announcement. The 1940 historical estimate were based on 18 drill-holes completed in the late 1930’s. The 1984 St Joe’s historical estimate was based on 16 drill-holes in the early 1980’s. The collar locations are indicated on the map in the main body of the announcement. No cut-off grade was used and this was believed to be appropriate because as the estimate covers only a very narrow portion of the known mineralisation with sharp grade boundaries. Additionally, the drill holes were only sampled in the very narrow portion of the copper mineralised Kupferschifer shale.

|

|

5.12.6 – Any more recent estimates or data relevant to the reported mineralisation available to the entity. |

Some additional holes were drilled by Mansfeld AG which were not used in the 1940 historical estimate because they were drilled after the publication of the estimate. GreenX has access to only part of the information for these holes and they are all believed to have results that confirm the estimate. The 1940 historical estimate was validated within the Ronshausen (Field 5) area by the later 1984 St Joe historical estimate. There are sufficient similarities between both the grade and tonnage of each of the estimates to justify confidence in the 1940 Mansfeld AS historical estimate. |

|

5.12.7 – The evaluation and/or exploration work that needs to be completed to verify the historical estimates or foreign estimates as mineral resources or ore reserves in accordance with Appendix 5A (JORC Code) |

The Company plans to take the following next steps to further seek to verify the historical estimates identified at Tannenberg: · Relogging and sampling of archived drill core (underway at the time of writing) · Further review and validation of historical data. · Twinning (repeat drilling) of certain holes. · Mineral Resource Estimation and reporting according to best practice and the JORC Code. There is no certainty that further exploration work will result in the historical estimate being reported in accordance with the JORC Code. |

|

5.12.8 – The proposed timing of any evaluation and/or exploration work that the entity intends to undertake and a comment on how the entity intends to fund that work. |

The Company expects to complete the next steps identified above in the following 12 months. GreenX currently has cash reserves of approximately $3.7 million (30 September 2025 – unaudited). |

|

5.12.9 – A cautionary statement proximate to, and with equal prominence as, the reported historical estimates or foreign estimates stating that: the estimates are historical estimates or foreign estimates and are not reported in accordance with the JORC Code; a competent person has not done sufficient work to classify the historical estimates or foreign estimates as mineral resources or ore reserves in accordance with the JORC Code; and it is uncertain that following evaluation and/or further exploration work that the historical estimates or foreign estimates will be able to be reported as mineral resources or ore reserves in accordance with the JORC Code |

A cautionary statement, proximate to, and with equal prominence as, the reported historical estimates has been stated on pages 1, 4 and 5 of this announcement. |

|

5.12.10 – A statement by a named competent person or persons that the information in the market announcement provided under rules 5.12.2 to 5.12.7 is an accurate representation of the available data and studies for the material mining project. The statement must include the information referred to in rule 5.22(b) and (c). |

A statement by a named competent person is included on page 7 of this announcement. |

JORC Code, 2012 Edition – Table 1 Report

Section 1 Sampling Techniques and Data

(Criteria in this section apply to all succeeding sections.)

|

Criteria |

JORC Code explanation |

Commentary |

|

Sampling techniques |

Nature and quality of sampling (eg cut channels, random chips, or specific specialised industry standard measurement tools appropriate to the minerals under investigation, such as down hole gamma sondes, or handheld XRF instruments, etc). These examples should not be taken as limiting the broad meaning of sampling. |

Due to the historic nature of the drilling results reported herein, it is not possible to comment on the quality of the sampling used to produce the results described. It is known from historic reports that the drill core was sawn. Sampling of ¼ core was conducted during multiple exploration phases between 1980 and 1987 within the licence area by St Joe. The information shown here was collated from original hard copy reports from that era and a State Survey Database. Assays, geological logging and gamma ray logs were conducted by St Joes Exploration and Mansfeld AG. No other information is available for the exploration drilling. |

|

|

Include reference to measures taken to ensure sample representivity and the appropriate calibration of any measurement tools or systems used. |

No details covering the representivity of the samples for the 1940 or 1984 estimate were included. Verification of the exploration assays was carried out by Masfeld AG against production grades from Wolfsberg and Schnepfenbusch production grades

|

|

|

Aspects of the determination of mineralisation that are Material to the Public Report. In cases where ‘industry standard’ work has been done this would be relatively simple (eg ‘reverse circulation drilling was used to obtain 1 m samples from which 3 kg was pulverised to produce a 30 g charge for fire assay’). In other cases more explanation may be required, such as where there is coarse gold that has inherent sampling problems. Unusual commodities or mineralisation types (eg submarine nodules) may warrant disclosure of detailed information. |

Work was not conducted to modern industry standards. |

|

Drilling techniques |