#SVML Sovereign Metals LTD – Issue of Shares on Conversion of Performance Right

Sovereign Metals Limited (ASX:SVM; AIM:SVML; OTCQX:SVMLF) (Sovereign or the Company) advises that it has issued 9,022,500 fully paid ordinary shares (Shares) upon the conversion of 9,022,500 unlisted performance rights upon satisfaction of the Bankable Definitive Feasibility Study Milestone held by certain directors, employees and consultants of the Company pursuant to its shareholder approved Employee Equity Incentive Plan for nil consideration. Change of Director’s Interest Notices are provided below.

Sovereign Metals Limited (ASX:SVM; AIM:SVML; OTCQX:SVMLF) (Sovereign or the Company) advises that it has issued 9,022,500 fully paid ordinary shares (Shares) upon the conversion of 9,022,500 unlisted performance rights upon satisfaction of the Bankable Definitive Feasibility Study Milestone held by certain directors, employees and consultants of the Company pursuant to its shareholder approved Employee Equity Incentive Plan for nil consideration. Change of Director’s Interest Notices are provided below.

An application will be made for the Shares to be admitted to trading on AIM (Admission) and it is expected that Admission will become effective on or around 22 April 2026.

Total Voting Rights

For the purposes of the Financial Conduct Authority’s Disclosure Guidance and Transparency Rules (DTRs), following Admission of the Shares, Sovereign will have 655,961,203 Ordinary Shares in issue with voting rights attached. The figure of 655,961,203 may be used by shareholders in the Company as the denominator for the calculations by which they will determine if they are required to notify their interest in, or a change to their interest in the Company, under the ASX Listing Rules or the DTRs.

Following the issue of the conversion of unlisted performance rights, the Company has the following securities on issue:

· 655,961,203 fully paid ordinary shares (of no par value);

· 6,190,000 unlisted performance rights subject to the “Final Investment Decision Milestone” expiring on or before 30 June 2026 (expected to lapse unvested); and

· 13,262,500 performance rights subject to the “Construction and Finance Milestone” that have no exercise price and expire 30 June 2028.

Change of Directors’ Interest Notices are provided below.

|

Enquiries |

|

Dylan Browne Company Secretary +61 8 9322 6322 |

|

Nominated Adviser on AIM and Joint Broker |

|

|

SP Angel Corporate Finance LLP |

+44 20 3470 0470 |

|

Ewan Leggat Charlie Bouverat |

|

|

|

|

|

Joint Broker |

|

|

Stifel |

+44 20 7710 7600 |

|

Varun Talwar |

|

|

Ashton Clanfield |

|

Link here to view the full announcement

Mendell Helium #MDH – Proposal to install 1,000 Mcf/day helium production facility at Rost

Mendell Helium is pleased to announce that M3 Helium Corporation (“M3 Helium”) has received a non-binding proposal with a leading helium producer to install equipment to recover and sell helium at its Rost 1-26 well (“Rost”) and the nearby Rost twin well (“Rost Twin”) where drilling has recently finished in the Fort Dodge region of Kansas, USA (the “Facility”).

Mendell Helium is pleased to announce that M3 Helium Corporation (“M3 Helium”) has received a non-binding proposal with a leading helium producer to install equipment to recover and sell helium at its Rost 1-26 well (“Rost”) and the nearby Rost twin well (“Rost Twin”) where drilling has recently finished in the Fort Dodge region of Kansas, USA (the “Facility”).

Highlights

· Proposal to install the Facility to recover and sell helium on the Rost site

· The Facilty would support production from Rost and the Rost Twin

· Phase 1: The Facility is being initially designed at 1,000 Mcf/day of raw gas with 5% helium content which equates to around 50 Mcf/day of helium production based on Rost’s gas composition

· Phase 2: The Facility could be expanded to accommodate future growth from M3 Helium wells in the Fort Dodge region

As announced on 27 June 2024, the Company has an option (the “Option”) to acquire M3 Helium, a producer of helium which is based in Kansas and holds an interest in six producing wells. There is no certainty that the Company’s option to acquire M3 Helium will be exercised, nor that the enlarged group will successfully complete a re-admission. The Company and M3 Helium have agreed to extend the date on which the Option should be exercised to 30 April 2026.

Under the terms of the non-binding proposal, M3 Helium will contract with a leading third party helium processor to facilitate the installation of equipment to recover and sell helium at Rost and the Rost Twin. Phase I of the Facility will be designed to process 1,000 Mcf of raw gas per day. Upon a successful drilling programme by M3 Helium in Fort Dodge. Phase II will incorporate expansion to allow for material incremental throughput from nearby wells and, with that, additional helium production and sales into what has become a constrained helium market.

M3 Helium’s obligations would be to provide a sufficient space on site to accommodate a larger PSA and compression facilities to load tube trailers as well as access to the 3-phase power that is already in place. M3 Helium is also obliged to deliver a gas stream from the wells that is suitable for use in a PSA meaning that some limited pre-treatment may be required.

The proposal includesa fee structure whereby processing fees are expected to be the greater of a fixed monthly amount and a percentage of helium revenues, together with an additional marketing fee. This structure ensures that higher production levels by M3 Helium are expected to have lower incremental costs. The proposal has a four year term and is renewable thereafter.

Subject to execution of definitive agreements, M3 Helium will have several redundant items of equipment at Rost, including its own PSA. These are intended to be redeployed on future wells. Full installation of the new Facility is expected to take around four months subject to availability and lead time for necessary equipment – M3 Helium will continue to operate its own surface purification equipment until that time. Further announcements will be made in due course following the execution of definitive agreements and updates in relation to the development of the proposed Facility.

Nick Tulloch, Chief Executive Officer of Mendell Helium and Chairman of M3 Helium, said: “In another validation of M3 Helium’s operations at Rost and the Rost Twin, this proposed collaboration with a leading helium producer represents a significant expansion of operations. The proposal received from M3 Helium’s partner to size the facilities at 1,000 Mcf/day illustrates its view of the potential of the two Rost wells.

“The conflict in the Middle East has generated some speculation on the direction of helium prices. Whatever the short term benefits may be to helium producers, the long term opportunity centres on the fragility of global helium supplies. Working with an industry partner to produce purified helium at M3 Helium’s well site represents a significant commercial advantage.

“Completion and perforation operations will shortly be underway for the Rost Twin and both Rost wells will be serviced by the facilities already in place at Rost before this proposed redevelopment.”

This announcement contains inside information for the purposes of the UK Market Abuse Regulation and the Directors of the Company are responsible for the release of this announcement.

ENDS

Engage with the Mendell Helium management team directly by asking questions, watching video summaries and seeing what other shareholders have to say. Navigate to our Interactive Investor website here: https://mendellhelium.com/link/PKa6Ve

Enquiries:

|

Investor questions on this announcement We encourage all investors to share questions on this announcement via our investor website

|

|

|

Mendell Helium plc Nick Tulloch, CEO

|

Via our website investors@mendellhelium.com |

|

Cairn Financial Advisers LLP (AQSE Corporate Adviser) Ludovico Lazzaretti / Liam Murray

|

Tel: +44 (0) 20 7213 0880 |

|

SI Capital Limited (Broker) Nick Emerson |

Tel: +44 (0) 1483 413500 |

|

Stanford Capital Partners Ltd (Broker) Patrick Claridge / Bob Pountney

|

Tel: +44 (0) 203 3650 3650/51

|

|

Fortified Securities Guy Wheatley

|

Tel: +44 (0) 203 4117773

|

|

AlbR Capital Limited Gavin Burnell / Colin Rowbury / Jon Belliss

|

Tel: +44 (0) 207 4690930

|

|

Brand Communications (Public & Investor Relations) Alan Green |

Tel: +44 (0) 7976 431608

|

Quantum Helium #QHE – £5 Million Institutional Placing Positions Quantum for Next Phase of Growth

![]() Quantum Helium Limited (AIM: QHE) is pleased to announce it has today raised £5 million (before expenses) by way of a conditional placing of 16,666,666,667 new ordinary shares (the “Placing Shares”) at a price of 0.03 pence per share (the “Placing Price”) (the “Placing”).

Quantum Helium Limited (AIM: QHE) is pleased to announce it has today raised £5 million (before expenses) by way of a conditional placing of 16,666,666,667 new ordinary shares (the “Placing Shares”) at a price of 0.03 pence per share (the “Placing Price”) (the “Placing”).

The Placing was arranged by OAK Securities and was undertaken with a number of institutional investors who approached the Company, reflecting growing interest in Quantum’s asset base and the strategic importance of domestic US helium supply.

Highlights

- £5 million institutional placing

- Cornerstoned by institutional investors following inbound demand

- Validates the strength of Quantum’s helium portfolio and US strategic positioning

- Funding supports the next phase of development at Sagebrush and Coyote Wash

- Multiple near-term catalysts, including results from the Company’s extended production test at Sagebrush

- Strengthened balance sheet and cash resources positions the Company well for next phase of growth

Background to the Placing

The Company has received increasing inbound interest from institutional investors in recent months, driven by the scale and quality of its helium portfolio and the growing strategic importance of helium as a critical commodity.

Helium plays an essential role in a wide range of high-value industries, including semiconductor manufacturing, AI infrastructure, medical imaging and advanced manufacturing, with demand continuing to increase.

At the same time, global helium supply remains constrained, with recent geopolitical developments, including disruptions in the Middle East, highlighting the importance of secure and domestic supply chains. This backdrop has resulted in increased investor focus on US-based helium development opportunities.

Quantum believes it is well positioned within this environment, with a portfolio of helium assets located in a proven US helium fairway and a clear pathway towards development and production.

Use of Funds

Proceeds from the Placing will be used to:

- Advance development planning and engineering at the Sagebrush Project

- Progress permitting, planning and progressing to drill-ready targets at Coyote Wash (100% owned)

- Fund well planning, long-lead items and infrastructure design at the Company’s Sagebrush and Coyote Wash projects

- Support ongoing technical work, including seismic interpretation and subsurface modelling

- Provide additional working capital and financial flexibility

The Company’s extended production test at the Sagebrush-1 well which remains the key near-term operational milestone is being funded from existing cash resources.

Current Operations

As announced on 16 April 2026, the extended production test at the Sagebrush-1 well is progressing well, with operations advancing in line with expectations.

The next phase of operations will focus on the perforation and testing of the first of two zones in the Leadville Formation. The Lower Leadville will be tested first, followed by a test of the upper Leadville where the DST was previously run. Perforations are scheduled to start this coming week.

The testing programme is designed to evaluate flow characteristics and confirm historical helium concentrations, including the previously reported 2.76% helium, and represents a critical step towards converting resources into reserves and advancing towards commercial development.

The Company expects a number of significant operational updates in the coming weeks as testing progresses through this key phase.

Carl Dumbrell, Chairman of Quantum Helium, said: “This is a very strong outcome for the Company and we are pleased to have secured the support of a number of high-quality institutional investors who recognised the strength of our asset base and the opportunity we are developing.

The Placing reflects increasing awareness of the strategic importance of helium, particularly in the United States, where there is a growing need for secure and domestic supply. Recent global events have further highlighted supply constraints, and we believe Quantum is well positioned to play a role in addressing this.

Importantly, this funding places the Company in the strongest financial position it has ever been in and allows us to accelerate our development plans while maintaining momentum across our operations.

We look forward to delivering on the significant milestones ahead and continuing to build value for shareholders.”

Quantum Chief Executive, Howard McLaughlin, added: “As outlined in our recent operational update, the extended production test program at Sagebrush-1 is progressing well and represents a major step towards unlocking the commercial potential of this project.

We are particularly excited about the upcoming perforation of the Lower Leadville Formation, which is expected to provide critical data on helium concentrations and flow rates. This will build on the historic results and further strengthen our understanding of the reservoir.

With this successful placing, we are now fully funded to execute our broader work programme across both Sagebrush and Coyote Wash. We have a number of important and exciting milestones ahead and remain confident in the outcome of the extended production test.

Our focus is firmly on progressing our projects towards commercialisation and establishing Quantum as a leading helium developer in the United States.

Additional Information

Quantum Helium has appointed OAK Securities (a trading name of Merlin Partners LLP), to act as the Company’s exclusive bookrunner and placement agent in connection with the Placing. Subject to and conditional on Admission, OAK Securities will be paid an annual broker retainer of £50,000 payable in cash, a one-off corporate advisory fee of £15,000 payable in cash, a cash commission in an amount equal to six per cent (6.0%) of the gross proceeds raised pursuant to the Placing. The Company will also issue OAK Securities warrants (the “Broker Warrants“) to subscribe for 6.0% of the number of Placing Shares placed in the Placing, with such Broker Warrants being exercisable at a price per share equal to the Issue Price for 3 years from the date of the closing of the Placing.

The Placing Shares, when issued and fully paid, will rank pari passu in all respects with the existing Common Shares in issue and therefore will rank equally for all dividends or other distributions declared, made or paid after the issue of the new Placing Shares.

Admission to AIM and Total Voting Rights

The Placing is conditional, inter alia, upon the Placing Shares being admitted to trading on AIM. Application has been made to the London Stock Exchange for the Placing Shares, which will rank pari passu with the Company’s existing issued ordinary shares, to be admitted to trading on AIM and dealings are expected to commence at 8:00 a.m. on or around 23 April 2026.

Following the issue of the Placing Shares, the Company’s total voting rights will comprise 49,985,396,722 Ordinary Shares of no par value, and the Company does not hold any shares in treasury. The above figure may therefore be used by shareholders as the denominator for the calculations by which they will determine whether they are required to notify their interest in, or a change to their interest in, the share capital of the Company under the Companies’ Articles.

Market Abuse Regulation (MAR) Disclosure

The information contained within this announcement is deemed by the Company to constitute inside information as stipulated under the Market Abuse Regulations (EU) No. 596/2014 (‘MAR’) which has been incorporated into UK law by the European Union (Withdrawal) Act 2018. Upon publication via Regulatory Information Service (‘RIS’), this information is now in the public domain

Enquiries:

| Quantum Helium Limited

Carl Dumbrell Chairman

|

NOMAD and Joint Broker

SP Angel Corporate Finance LLP Stuart Gledhill / Richard Hail / Adam Cowl +44 (0) 20 3470 0470 |

| Brand Communications

Alan Green Tel: +44 (0) 7976 431608 |

Joint Broker

CMC Markets UK Plc Douglas Crippen +44 (0) 020 3003 8632 Joint Broker OAK Securities Jerry Keen / Robert Bell Tel: +44 (0) 203 973 3678

|

Updates on the Company’s activities are regularly posted on its website: www.quantum-helium.com

Notes to editors

Quantum (AIM: QHE) is a helium and hydrocarbon exploration, development, and production company with projects in the US and Australia. Quantum’s strategic objectives remain consistent: to identify opportunities which will provide operating cash flow and have development upside, in conjunction with progressing exploration. The Company has several projects in the US, in addition to royalty interests in Australia.

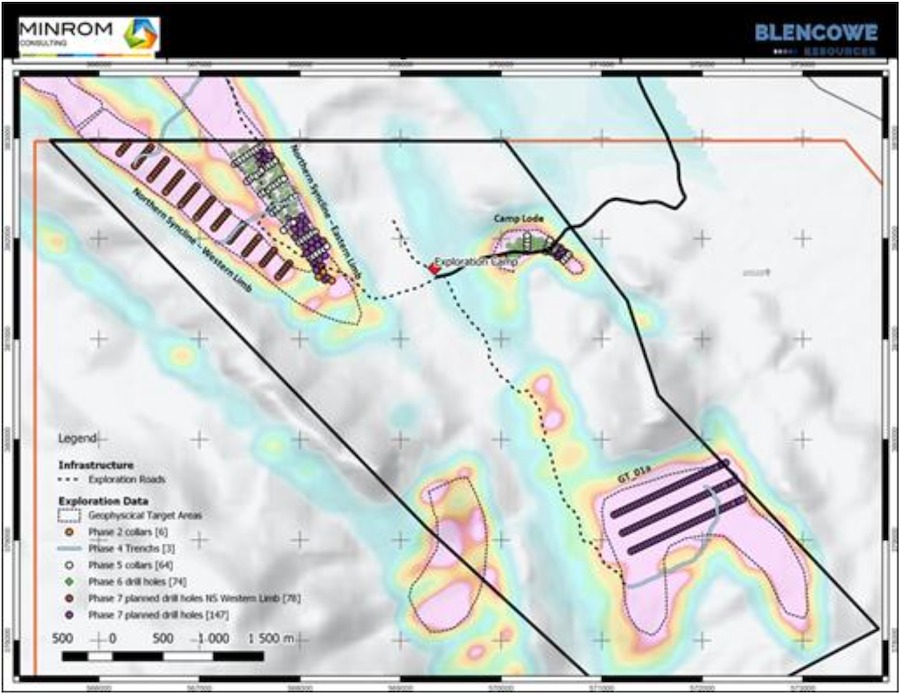

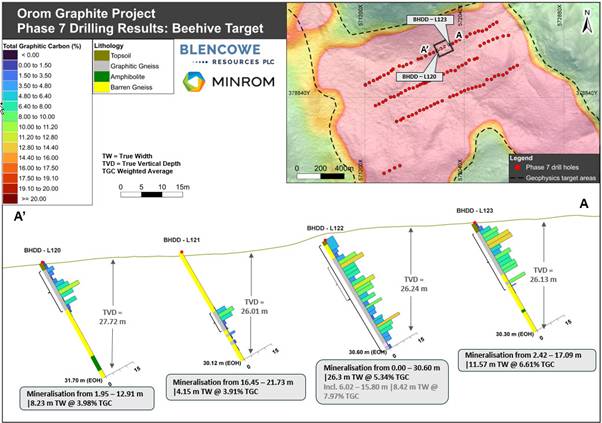

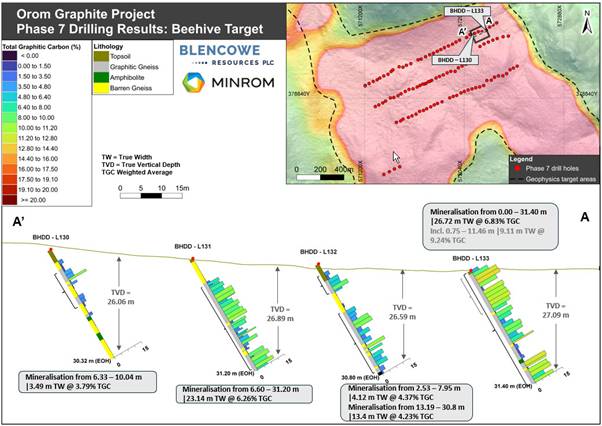

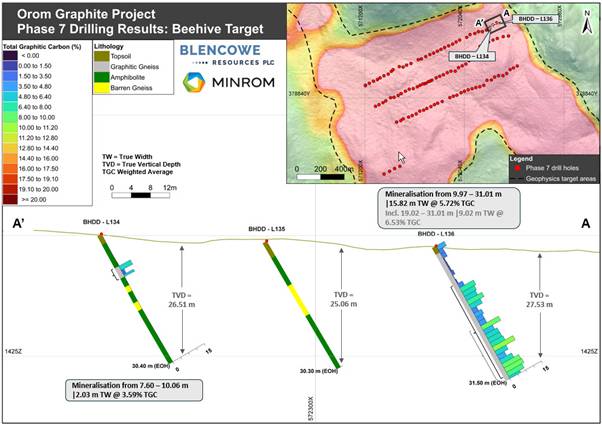

#BRES Blencowe Resources PLC – Beehive Drilling Results

Blencowe Resources Plc (LSE: BRES) is pleased to provide an update on further assay results from shallow drilling at the company’s new Beehive deposit. Both Beehive and Iyan are substantial new exploration finds within the most recent 2025 drill programme and both will contribute significantly to the size and scale of the Orom-Cross graphite project.

Blencowe Resources Plc (LSE: BRES) is pleased to provide an update on further assay results from shallow drilling at the company’s new Beehive deposit. Both Beehive and Iyan are substantial new exploration finds within the most recent 2025 drill programme and both will contribute significantly to the size and scale of the Orom-Cross graphite project.

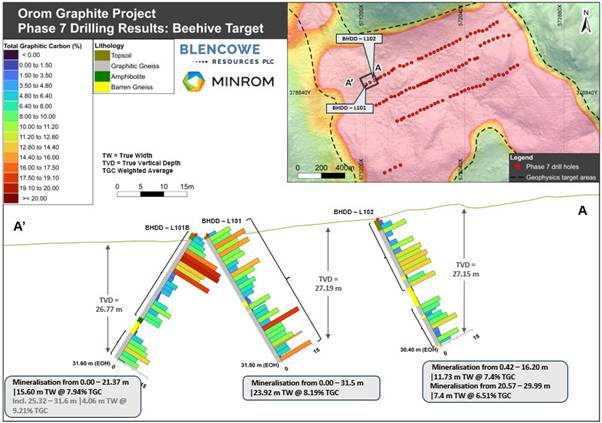

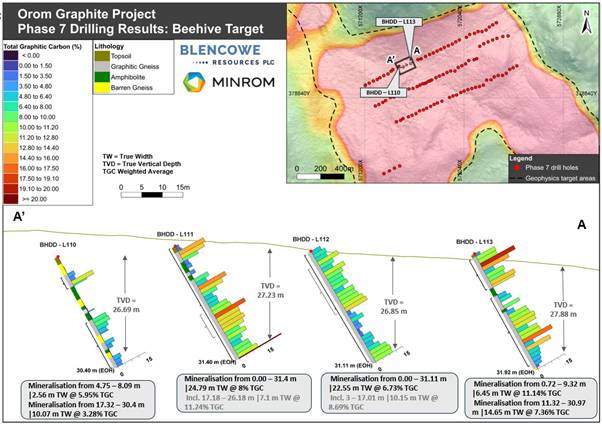

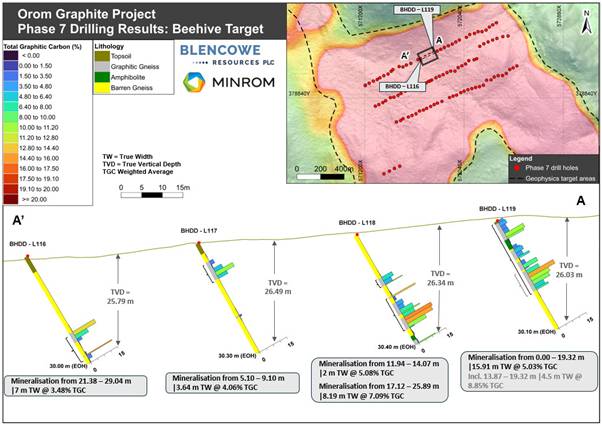

As part of the Stage 7 drilling programme, the Company completed 110 shallow drill holes at Beehive, designed to test the continuity, thickness and near-surface extent of graphite mineralisation. This announcement reports further assay results from 36 holes (including additional coverage toward the northern extent), following the Company’s previous Beehive assay update.

The shallow programme was designed to define near-surface, bulk mineable graphite mineralisation, with holes drilled to a planned depth of approximately 30 metres. The majority of reported holes intersected graphite mineralisation from near surface to end-of-hole, with many holes ending in mineralisation, highlighting potential for continuation below the current shallow drilling depth. This is consistent with previously reported deeper drilling at Beehive, which demonstrated graphite mineralisation continuing to approximately 100 metres depth.

Whilst the drilling was intended to close out the northern extent of the deposit, results also indicate potential for additional extensions of up to ~400m – particularly toward the northern and western end of the deposit – within the broader target area.

Beehive Drilling Highlights

An additional 36 assay results were received and compiled from the Stage 7 programme:

· Thick near-surface mineralisation: multiple holes deliver ~30-32 meters mineralisation from surface, supporting depth continuity and bulk mining potential.

· Strong bulk grades across the batch: 12 holes average ≥5.0% TGC and 8 holes average ≥6.0% TGC over the drilled intervals highlighting strong in situ grades within Beehive.

· High-grade frequency: all holes are mineralised and grades are consistently higher than overall average grades for other deposits within Orom-Cross.

Selected Beehive Significant Shallow Intercepts Include:

o BHDD-L101: 31.5 meters @ 8.19% TGC from surface

o BHDD-L111: 31.4 meters @ 8.00% TGC from surface

o BHDD-L327: 31.2 meters @ 7.67% TGC from surface

o BHDD-L113: 31.92 meters @ 7.59% TGC from surface, including 9.32m @ 11.14% TGC

o BHDD-L133: 31.4 meters @ 6.83% TGC from surface

o BHDD-L102: 29.61 meters @ 6.11% TGC from surface

o BHDD-L325: 31.3 meters @ 6.21% TGC from surface

Interpretation and Next Steps

These additional shallow results continue to support a thick graphite system at shallow depths, while previously reported deeper drilling has demonstrated mineralisation continuing to approximately 100 metres depth. Together, this work is building the dataset required to define the near-surface component and progress modelling toward a maiden Beehive JORC Mineral Resource scheduled for Q2 2026.

Further Beehive assay batches are being passed directly to the Company’s independent geological consultants, Minrom, for validation and quality assurance. Results will be reported progressively as batches are cleared and, subject to modelling, are intended to support a future Beehive JORC Mineral Resource update and provide further clarity on overall scale and development readiness as Blencowe continues to progress strategic and funding discussions in parallel.

Beehive has been defined over approximately 1,200 metres of strike and 480 metres of width to date, with scope for extensions beyond the current drill lines.

Blencowe Resources Executive Chairman, Cameron Pearce commented:

“We are pleased to report a further batch of Beehive assay results and appreciate shareholders’ patience as results move through laboratory reporting and independent validation. We expect a further set of assay results to become available shortly and will provide updates as batches are cleared.

Beehive continues to build momentum. This further batch reinforces continuity at shallow depths, with multiple plus-30 meter intercepts from surface and standout results including 31.5m @ 8.19% TGC and 31.4m @ 8.00% TGC.

Following the recent maiden Iyan JORC Mineral Resource of 16.9 million tonnes, which increased total Orom-Cross JORC Mineral Resources by 66% to 43.0 million tonnes, Beehive remains the next clear growth lever as we progress toward a maiden Beehive JORC Mineral Resource update this quarter. We would expect the continuity and thickness being demonstrated at Beehive to translate into a material increase in overall tonnage, subject to completion of assay flow, modelling and JORC reporting.

With access to renewable hydroelectric power and an expanding resource base, Orom-Cross continues to be positioned as an integral part of the western markets’ drive for secure, non-China critical mineral supply chains, supporting downstream pathways and longer-term offtake discussions.”

Beehive Deposit – Key Drill Results

Figures 1-2: Beehive Deposit drill sections showing thick, continuous graphite mineralisation remaining open at depth.

|

Blencowe Resources Plc |

|

|

Sam Quinn (Director) |

Tel: +44 (0)1624 681 250

|

|

Sasha Sethi (Investor Relations) |

Tel: +44 (0) 7891 677 441 |

|

Tavira Financial (Joint Broker)

Jonathan Evans |

Tel: +44 (0)20 3192 1733 |

|

Oak Securities (Joint Broker)

Calvin Man /Mungo Sheehan / Jerry Keen |

Tel: +44 (0)20 3973 3678 |

|

|

|

|

|

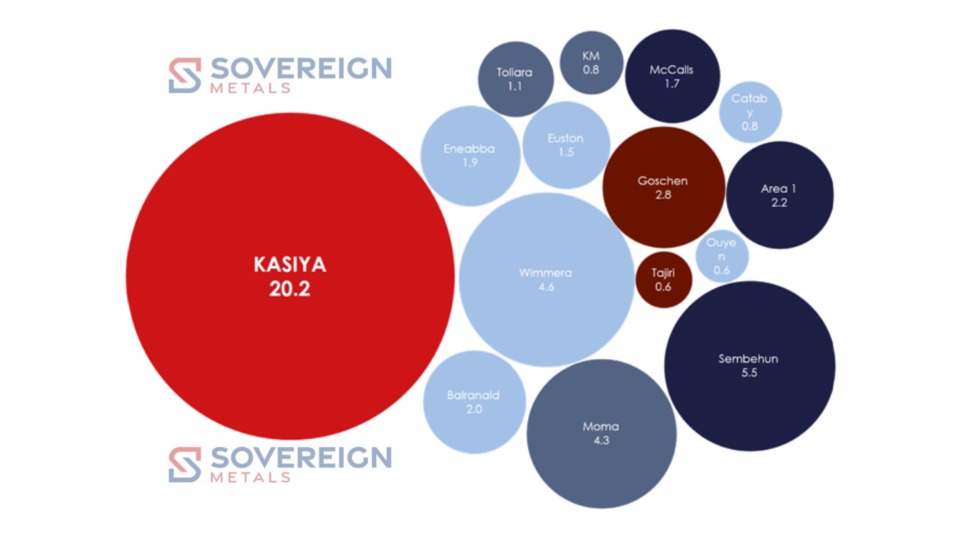

#SVML Sovereign Metals LTD – Kasiya Definitive Feasibility Study Results

OUTSTANDING FINANCIAL RETURNS

Steady State annual EBITDA US$476M and Free Cash Flow (pre-tax, unlevered) US$452M

Total revenue of US$16.2Bn over 25-year initial mine life, with potential for mine life extensions

Pre-tax NPV₈ of US$2.2 billion

NPV/Capex ratio of 3.0x – capital expenditure to first production of US$727 million

Operating cost of just US$450/t product (FOB Nacala) – underpinning strong margin resilience across commodity cycles

GLOBAL LEADER ACROSS TWO CRITICAL MINERALS SUPPLY CHAINS

Positioned to become the world’s largest producer of both natural rutile (222ktpa) and natural flake graphite (275ktpa)

Lowest-cost graphite producer globally at or beyond pre-feasibility stage – including China

Titanium and graphite both designated as Critical Minerals by the United States and the European Union, highlighting their strategic importance to Western supply chains

Free-dig orebody requiring no pre-strip, drilling or blasting with a simple low-energy processing flowsheet

Established export infrastructure: hydropower grid, heavy-haul rail, port at Nacala

BANKABLE DEVELOPMENT PATHWAY

DFS completed under the oversight of the Sovereign-Rio Tinto Technical Committee

Data obtained from Pilot Mining Program, completed with technical input from Rio Tinto, provided real-world inputs across key DFS workstreams

DFS incorporates environmental and social workstreams aligned with IFC performance standards; World Bank/IFC Collaboration Agreement in place as potential co-lead mandated lead arranger for project financing

Non-binding offtake MOUs covering over 50% of Stage 1 rutile production (Mitsui) and over 35% of coarse flake graphite sales (Traxys)

HEAVY RARE EARTH POTENTIAL NOT INCLUDED IN DFS – EVALUATION UNDERWAY

Monazite concentrate recovered from rutile processing circuit with exceptionally elevated levels of heavy rare earths Dysprosium, Terbium and Yttrium

Potential third revenue stream at minimal incremental cost – all three elements subject to Chinese export restrictions

Dedicated monazite evaluation program now underway to assess scale, recovery and economic potential

Sovereign Metals Limited (ASX:SVM; AIM:SVML; OTCQX:SVMLF) (Sovereign or the Company) is delighted to announce the results of the Definitive Feasibility Study (DFS or the Study) for its Kasiya Rutile-Graphite Project (Kasiya or the Project) in Malawi. The DFS builds on the outcomes of the Optimised Pre-feasibility Study (OPFS) and on empirical data from the Pilot Mining and Rehabilitation Program (Pilot Mining). The DFS was undertaken in accordance with a scope of work approved by, and with technical input and oversight from, the Sovereign-Rio Tinto Technical Committee and, where applicable, conforms to the World Bank Group’s International Finance Corporation (IFC) Performance Standards to enhance bankability of the Project.

Managing Director and CEO Frank Eagar commented:

“The completion of this DFS marks a defining milestone for Kasiya and for the global titanium and graphite supply chains. To deliver a DFS of this quality, depth and confidence, rarely achieved by a pre-production company, reflects the calibre of partnerships that Sovereign has assembled around this project: Rio Tinto’s technical expertise, alignment with IFC Performance Standards under our Collaboration Agreement, and offtake interest driven by U.S. and Japanese supply chain security priorities. The successful completion of large-scale field trials, combined with the expertise of our experienced owner’s team and the technical support provided by Rio Tinto, reinforces Kasiya’s potential to be a long-life, low-cost, and reliable source of two critical and globally strategic minerals. Kasiya is not simply a mining project – it is a globally strategic asset.“

TABLE 1: Key DFS Metrics (Steady State)

|

OPERATING METRICS |

Units |

Results |

|

Initial Life of Mine (LOM) |

Yrs |

25 |

|

Total Ore Mined |

Mt |

536 |

|

Phase 1 Plant Throughput (Yrs 1-4) |

Mtpa |

12 |

|

Phase 2 Plant Throughput (Yrs 5-25) |

Mtpa |

24 |

|

Annual Rutile Production (95%+ TiO2) |

ktpa |

222 |

|

Annual Graphite Production (96% TGC) |

ktpa |

275 |

|

FINANCIAL PERFORMANCE |

||

|

Total Revenue |

US$M |

16,210 |

|

Annual Revenue |

US$M |

728 |

|

Annual EBITDA |

US$M |

476 |

|

Annual Free Cash Flow (pre-tax, unlevered) |

US$M |

452 |

|

NPV8 (real, pre-tax) |

US$M |

2,204 |

|

IRR (pre-tax) |

% |

23% |

|

OPERATING AND CAPITAL EXPENDITURE |

||

|

Capex to First Production |

US$M |

727 |

|

Total LOM Development Capex |

US$M |

1,239 |

|

Total LOM Sustaining Capex |

US$M |

431 |

|

Operating Costs (FOB Nacala) |

US$/t product |

450 |

Note: Steady State is defined as years of operation during which total run-of-mine is at full capacity of 24 Mtpa (i.e., years 5 to 23). All results are presented on a 100% project basis.

DFS CONFIRMS SOVEREIGN TO REDEFINE TITANIUM METAL AND GRAPHITE SUPPLY CHAINS

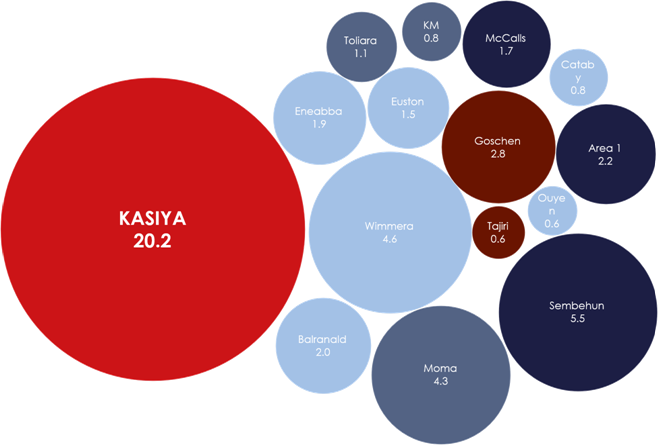

Kasiya, located in central Malawi, hosts the world’s largest natural rutile deposit and the second-largest flake graphite deposit. Both titanium and graphite are officially classified as Critical Minerals by the United States and the European Union. At steady-state, Kasiya is forecast to deliver approximately 222 kt of rutile and 275 kt of graphite annually – positioning Sovereign as potentially the world’s largest producer of both natural rutile and natural flake graphite.

Natural Rutile – Addressing Titanium Supply Chain Vulnerability

Natural rutile is the purest and highest-grade form of naturally occurring titanium feedstock, with titanium dioxide (TiO₂) content typically exceeding 95%. It is the preferred feedstock for titanium sponge production and high-specification titanium alloy applications in aerospace, defence and medical industries.

According to the United States Geological Survey (USGS), the United States currently produces zero titanium sponge domestically and is 100% import-reliant, with record imports of 44,000 tonnes in 2025. Japan supplies over 70% of the US’s titanium sponge imports, and Japanese producers themselves depend on securing reliable natural rutile feedstock. Meanwhile, Western-qualified titanium sponge production has declined 9% to approximately 81,000 tonnes, while China’s share of global sponge production has risen to 70%.

Figure 1: Kasiya contained rutile resource vs. other rutile-bearing titanium deposits (Mt)

(Source: See Appendix 2)

Global primary rutile supply is in structural decline. Rutile reserves at Leonoil Company Limited’s Area 1 Mine are expected to be depleted within the next 2-3 years, and Energy Fuels Inc. has recently ceased operations at its Kwale Mine in Kenya. With no other large-scale primary rutile developments at an advanced stage, Sovereign is positioned to become the only large-scale primary producer of natural rutile globally.

Kasiya’s natural rutile has demonstrated premium chemical characteristics and suitability across all major end-use applications, with high TiO₂ content, low impurity levels, and favourable particle size distribution – positioning it as a preferred high-purity feedstock within a structurally undersupplied market.

Kasiya’s 222ktpa of natural rutile would represent a significant addition to Western-accessible non-pigment rutile supply, directly addressing the structural feedstock deficit facing the US, Japanese and European titanium industries.

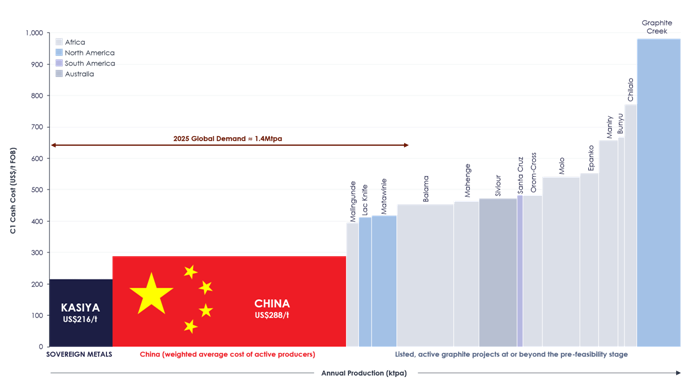

Natural Flake Graphite – Lowest-Cost Producer Outside Chinese Control

Graphite is essential to lithium-ion battery anodes, refractories and a range of advanced industrial applications. China currently dominates global natural graphite production and processing, accounting for approximately 77% of worldwide output and an even larger share of battery-grade anode material³. The US has designated graphite as a critical mineral and is actively seeking to diversify supply away from Chinese-controlled sources, including through the US$12 billion Project Vault strategic reserve initiative.

Kasiya’s incremental cost of graphite production is estimated at US$216/t. Based on public disclosures by listed graphite developers with studies at or beyond the pre-feasibility stage, this positions Sovereign as the lowest-cost graphite producer globally, including China (see Appendix 3).

Compared with single-commodity hard-rock graphite operations, Kasiya benefits from a soft, free-dig orebody and a simple processing flowsheet. The majority of operating costs are allocated to the primary rutile stream, enabling the production of high-purity, coarse-flake graphite at materially lower costs. Independent testing has confirmed that Kasiya graphite performs exceptionally well as an anode material for lithium-ion batteries, while also meeting specifications for traditional industrial markets such as refractories.

Figure 3: Natural flake graphite C1 cash costs. (Source: See Appendix 3. China cost from Benchmark Minerals Intelligence)

Figure 4: Utility-scale battery energy storage system using graphite anodes – California, USA.

SUMMARY OF KEY DFS WORKSTREAMS

Following input from world-class consultancies, Sovereign’s highly experienced owners’ team, and subject matter experts from Rio Tinto, the DFS has reconfirmed that Kasiya will be a leading future supplier to two distinct strategic critical minerals supply chains and outside of Chinese control – natural rutile for the titanium industry and natural flake graphite.

The DFS outlines a large-scale, long-life operation that delivers substantial volumes of premium-quality natural rutile and graphite while generating significant returns across a range of price scenarios.

The DFS for Kasiya has been prepared in accordance with the JORC Code (2012), with an estimated accuracy range of ±15% for Capital Expenditure (Capex) and ±10% for Operating Costs (Opex).

Dry Mining Method Confirmed

Using real-world data collected from the Pilot Mining, the DFS confirms a dry mechanical mining method using draglines and 100t rigid dump trucks. The soft, free-dig saprolite orebody requires no drilling, blasting, crushing or milling. A two-bench approach (5m top cut, up to 15m bottom cut) keeps the draglines above the water table, eliminating the need for production equipment below groundwater level. This represents a significant de-risking step from the hydro-mining method originally considered in the original Pre-feasibility Study (PFS).

No Conventional Tailings Storage Facility

A major advancement in the DFS is the elimination of the conventional Tailings Storage Facility (TSF) leading to a significant reduction in the mining footprint and providing a flexible, lower-risk tailings management solution. All tailings will be stored via hydraulic co-disposal backfilling of mined-out pits, designed in compliance with the Global Industry Standard on Tailings Management (GISTM), aiming for zero harm to people and the environment. The 50:50 fines-to-sand backfill ratio closely matches the existing soil profile, supporting progressive rehabilitation. This has also reduced the raw water dam wall height from 23m to 20.7m and storage capacity from 16.4 to 11Mm³.

Hydropower-Sourced Grid Electricity

The DFS is based on connection to Malawi’s national hydropower grid via a 132kV overhead line to the Nkhoma substation. Electricity Supply Corporation of Malawi Limited (ESCOM) has confirmed significant grid expansion is underway, including a 400kV Mozambique interconnector (2025) and the 375MW IFC/World Bank-funded Mpatamanga hydropower station (2030). Grid connection delivers substantially lower power costs and a favourable emissions profile.

Processing Flowsheet

Ore will be trucked to the processing plant for scrubbing and screening before entering the Wet Concentration Plant (WCP). The WCP employs a low-energy gravity separation process to produce a Heavy Mineral Concentrate (HMC). The HMC is then fed to the Mineral Separation Plant (MSP), where electrostatic and magnetic separation yield premium-quality rutile (+95% TiO₂), suitable as a direct feedstock for titanium sponge production or use in high-end titanium alloy applications, including aerospace and defence. Graphite-rich concentrate recovered from the spirals is processed in a dedicated flotation plant, producing a high-purity, high-crystallinity, coarse-flake graphite product. Independent testing has confirmed that Kasiya graphite performs exceptionally well as an anode material for lithium-ion batteries and meets specifications for traditional industrial markets such as refractories.

Dual Plant Configuration

The DFS confirms a staged development with two 12Mtpa processing plants – South Plant from Year 1 and North Plant from Year 5 – positioned at the respective resource centres of gravity to minimise haulage distances and costs. The configuration provides operational flexibility and a phased capital profile.

Logistics and Export Infrastructure

Kasiya’s products will be railed directly from a purpose-built dry port at the mine site eastward along the Nacala Logistics Corridor to the container terminal at the Port of Nacala on the Indian Ocean. The existing heavy-haul rail line and deep-water port provide a proven, operational export route – a significant infrastructure advantage over comparable undeveloped projects. Product transport cost is estimated at US$117/t product (FOB Nacala).

Rutile and Graphite Pricing

The DFS adopts a life-of-mine weighted-average realised rutile price of US$1,670/t (real, FOB Nacala), based on an independent TZMI market study. Japanese titanium metal producers OSAKA Titanium Technologies Co., Ltd. (Osaka Titanium) and Toho Titanium Co., Ltd. (Toho Titanium) are expected to drive the growth in rutile demand for titanium manufacturing over the next 10 years. Graphite pricing is based on an independent Benchmark Minerals Intelligence (BMI) price forecast, resulting in a life-of-mine average price of approximately US$1,288/t (FOB Nacala) – effectively in line with the OPFS assumption of US$1,290/t. The graphite basket price is derived from FOB China benchmarks, adjusted for an East Africa premium and weighted by Kasiya’s concentrate flake size distribution.

IFC Performance Standards Integrated into Design

The DFS has been prepared in alignment with IFC Performance Standards, with a comprehensive Environmental and Social Impact Assessment (ESIA) nearing completion and the full suite of environmental and social specialist studies completed. Sovereign’s established on-the-ground social team of 22 core staff and 90-member Community Liaison Team represent a level of social preparedness rarely achieved at DFS stage.

Mining and Rehabilitation Trials – Proven in Practice

Large-scale mining and rehabilitation trials were completed during the DFS period, covering excavation, backfilling, soil remediation and crop establishment. During Pilot Mining, the Company successfully completed dry and hydraulic mining trials, excavating a test pit at Kasiya. The test pit covered the planned area of 120 metres by 110 metres and was excavated to a depth of 20 metres through the weathered ore at Kasiya.

Post mining, the rehabilitated pit has achieved maize yields of 5.2 tonnes per hectare within six months of backfilling – over five times the local community average of approximately 1 tonne per hectare. The Pilot Mining validated the progressive rehabilitation approach and confirmed that mined land can be returned to productive agricultural use within one to two years.

|

Enquiries |

|

|

Frank Eagar, Managing Director & CEO South Africa / Malawi +27 21 140 3190

|

Sapan Ghai, CCO London +44 207 478 3900 |

|

Nominated Adviser on AIM and Joint Broker |

|

|

SP Angel Corporate Finance LLP |

+44 20 3470 0470 |

|

Ewan Leggat Charlie Bouverat |

|

|

|

|

|

Joint Broker |

|

|

Stifel |

+44 20 7710 7600 |

|

Varun Talwar |

|

|

Ashton Clanfield |

|

To view this announcement in full, including the Summary Section of the DFS and all images and figures, please refer to: https://api.investi.com.au/api/announcements/svm/b6f76c34-dfa.pdf.

Quantum Helium #QHE – Sagebrush-1 Testing Progresses; Key Leadville Perforation Next Week

Quantum Helium Limited (“Quantum” or the “Company”) is pleased to provide an operational update on the extended production test at the Sagebrush-1 well, Colorado.

Quantum Helium Limited (“Quantum” or the “Company”) is pleased to provide an operational update on the extended production test at the Sagebrush-1 well, Colorado.

Highlights

- Extended production test program progressing well, with operations advancing in line with plan

- Lower Leadville perforation scheduled for next week, targeting the primary helium-bearing interval

- Key well preparation milestones are progressing, including cementing, casing integrity testing and drill-out operations

- Testing programme designed to test flow rates and confirm historical helium concentrations of 2.76%

- Critical step towards converting prospective helium resources into reserves and commercial development

Operational Update

Operations at Sagebrush-1 continue to progress well, with the extended production test now actively underway.

Over the past week, the Company has successfully completed key preparatory and completion activities, currently completing cementing operations across the currently producing Ismay zone, pressure testing of casing, and drill-out of cement and bridge plug. These works are essential to ensure well integrity and optimise conditions ahead of flowing the primary target interval.

The next phase of operations will focus on the perforation and testing of the Lower Leadville Formation, the principal helium-bearing reservoir at Sagebrush, with perforation operations scheduled to start over the coming week as the programme moves into its key testing phase.

The Leadville test is designed to evaluate flow characteristics and confirm helium concentrations, building on historic testing at the Sagebrush-1 well, which recorded helium concentrations of 2.76%.

The Company will continue to provide updates as operations progress through this critical phase of testing.

Project Progress to Date

Quantum has delivered a series of significant milestones to reach this stage of operations, including:

- Acquisition and consolidation of the Sagebrush Project

- Approval of key agreements with the Ute Mountain Ute Tribe

- Securing and funding of the Irrevocable Letter of Credit for bonding purposes

- Approval of lease assignments and operatorship by the BIA and relevant regulators

- Completion of 3D seismic across the project area, identifying a large, well-defined structure

- Final regulatory approvals enabling commencement of field operations

These achievements position the Company strongly as it moves into the most critical stage of the extended production test.

Strategic Context

The extended production test at Sagebrush-1 represents a key step in Quantum’s strategy to unlock the value of its helium portfolio.

The Company holds over 1 Bcf of 2U prospective recoverable helium resources across Sagebrush and Coyote Wash, representing one of the largest independently assessed helium portfolios among London-listed companies.

The current testing programme is focused on advancing Sagebrush from a resource-stage asset towards reserves, development and ultimately commercial production, while further growth potential exists across multiple drill-ready prospects at Coyote Wash.

This strategy is supported, in part, by Quantum’s existing oil production at Sagebrush, which has continued to generate revenue and contribute towards funding helium-focused operations.

Quantum Chief Executive, Howard McLaughlin, commented: “We are very pleased with the progress being made at Sagebrush-1, with operations advancing smoothly through the initial phases of the extended production test program.

What sets Quantum apart from many of our peers is that we are not searching for helium – we already have a significant, independently assessed helium resource base. Our focus now is on confirming the historical helium concentration of 2.76% recorded at Sagebrush-1, and moving the resource into reserves, through appraisal and ultimately commercial development.

The upcoming perforation of the Lower Leadville Formation is a major milestone for the Company and marks the transition into the key testing phase. This is the interval we believe holds the greatest potential, and we are excited to now be entering this stage of operations.

Importantly, Sagebrush is just one part of a much larger growth story. With a substantial prospective helium resource base and multiple drill-ready targets at Coyote Wash, we believe Quantum is uniquely positioned in the London market as we move into the next stage of value creation.

We look forward to keeping shareholders updated as the flow testing program and results become available in due course.”

Enquiries:

| Quantum Helium Limited

Carl Dumbrell Chairman

|

NOMAD and Joint Broker

SP Angel Corporate Finance LLP Stuart Gledhill / Richard Hail / Adam Cowl +44 (0) 20 3470 0470 |

| Brand Communications

Alan Green Tel: +44 (0) 7976 431608 |

Joint Broker

CMC Markets UK Plc Douglas Crippen +44 (0) 020 3003 8632 |

Updates on the Company’s activities are regularly posted on its website: www.quantum-helium.com

Notes to editors

Quantum (AIM: QHE) is a helium, hydrogen and hydrocarbon exploration, development, and production company with projects in the US and Australia. Quantum’s strategic objectives remain consistent: to identify opportunities which will provide operating cash flow and have development upside, in conjunction with progressing exploration. The Company has several projects in the US, in addition to royalty interests in Australia.

Mendell Helium #MDH – Update on drilling the Rost twin well

Mendell Helium is pleased to announce the successful conclusion of drilling operations at M3 Helium Corporation’s (“M3 Helium”) new twin well to the existing Rost 1-26 well (“Rost”) in Fort Dodge, Kansas.

Mendell Helium is pleased to announce the successful conclusion of drilling operations at M3 Helium Corporation’s (“M3 Helium”) new twin well to the existing Rost 1-26 well (“Rost”) in Fort Dodge, Kansas.

Highlights

- Rost 2-26 well (“Rost Twin”) reached total depth of 5,571 feet

- Mass spectrometer evidences helium with low hydrocarbon signatures in several zones

- Completion process, including perforating the well, will begin in the next 10 days

- Second jumbo tube trailer identified for lease to support expected increase in production

- Commitments received from US investors to fund 35% of the Rost Twin

As announced on 27 June 2024, the Company has an option (the “Option”) to acquire M3 Helium, a producer of helium which is based in Kansas and holds an interest in six producing wells. There is no certainty that the Company’s option to acquire M3 Helium will be exercised, nor that the enlarged group will successfully complete a re-admission. The Company and M3 Helium have agreed to extend the date on which the Option should be exercised to 30 April 2026.

Rost Twin

Drilling operations at the Rost Twin have concluded at total depth of 5,571 feet. Completion with larger 7 inch casing has been successful with this part of the project being both on budget and on time.

M3 Helium employed a mass spectrometer, coupled with gas detection equipment, to assess the prospective hydrocarbon gases, hydrogen and helium in the Rost Twin. Very encouragingly, the mass spectrometer recorded several shows of helium in different potential production zones within the well. The helium was detected with low hydrocarbon signatures supporting M3 Helium’s theory that the helium-rich sands from which Rost produces extend to the Rost Twin.

Preparations are now underway for completion and perforation of the Rost Twin, with work expected to commence in the next 10 days. Although Rost produces only from the Morrow sands, for the Rost Twin, M3 Helium will examine perforating other potential production zones based on results from the mass spectrometer and gas analyses to be performed during completion. The Rost Twin was drilled with larger casing to support enhanced production and M3 Helium will use that flexibility in determining the extent of perforations. Certain of the zones where helium has been detected may require stimulation, most likely with an acid frack, and this will also be established in the completion process.

Following completion, the electric submersible pump that was previously used to de-water Rost, will be installed in the Rost Twin.

In preparation for increased production from the Rost wells, M3 Helium has also identified an additional jumbo tube trailer for lease. This would take its fleet to two trailers, each with a capacity of 160 Mcf, and therefore would ensure no interruption to production in between deliveries.

As previously announced, M3 Helium received interest from high net worth US investors to co-fund the Rost Twin and M3 Helium has now entered into a series of binding agreements with Rixford Resources LLC (“Rixford”), representing the investors, in relation to the development of the Rost Twin well (the “Rost Agreements”). The Company closed applications prior to the results of the mass spectrometer being known at which time Rixford confirmed that it had received commitments for 35% of the expected costs for the Rost Twin and the upgrade of the Brobee salt water disposal well, being US$372,000 in aggregate. These commitments will now be validated and payments will be remitted to M3 Helium in line with the work programme. Pursuant to the Rost Agreements, Rixford will acquire a 35% working interest in the Rost Twin well.

The funding is for the wells only and not for the surface helium purification facility installed at Rost. M3 Helium will charge Rixford a processing fee equal to 20% of their share of the helium produced from the Rost Twin. Rixford has an option to acquire a 50% interest in the PSA at development cost and, if it elects to do so the processing fee would cease.

Under the Rost Agreements, Rixford has been granted a right of first refusal to participate in up to five future wells drilled by M3 Helium or its affiliates in Kansas on substantially the same terms as the Rost Agreements.

Nick Tulloch, Chief Executive Officer of Mendell Helium and Chairman of M3 Helium, said: “The decision to drill the Rost Twin has been thoroughly vindicated by positive helium detection in several zones. As M3 Helium now moves towards completing and perforating the well, these early signs are that the Rost Twin has indications of being a successful production well. With the 7 inch casing supporting greater production levels than have been achieved at Rost, this is a significant opportunity for M3 Helium and paves the way for the ongoing development of the Fort Dodge region.

“The next project will be the recompletion of the Schneweis Ventures 13A well with Ritchie Exploration, Inc. and thereafter the development of the Bleumer and Enlow leases, with a production permit already secured for the first well on Enlow.

“We are also pleased to welcome Rixford as investors in M3 Helium’s projects. This first successful conclusion of funding new wells at the project level paves the way for a faster roll out of operations through an innovative non-dilutive funding mechanism.”

This announcement contains inside information for the purposes of the UK Market Abuse Regulation and the Directors of the Company are responsible for the release of this announcement.

ENDS

Engage with the Mendell Helium management team directly by asking questions, watching video summaries and seeing what other shareholders have to say. Navigate to our Interactive Investor website here: https://mendellhelium.com/link/PKa6Ve

Enquiries:

| Investor questions on this announcement

We encourage all investors to share questions on this announcement via our investor website

|

https://mendellhelium.com/s/a6a55a |

| Mendell Helium plc

Nick Tulloch, CEO

|

Via our website

investors@mendellhelium.com |

| Cairn Financial Advisers LLP (AQSE Corporate Adviser)

Ludovico Lazzaretti / Liam Murray

|

Tel: +44 (0) 20 7213 0880 |

| SI Capital Limited (Broker)

Nick Emerson |

Tel: +44 (0) 1483 413500 |

|

Stanford Capital Partners Ltd (Broker) Patrick Claridge / Bob Pountney

|

Tel: +44 (0) 203 3650 3650/51

|

| Fortified Securities

Guy Wheatley

|

Tel: +44 (0) 203 4117773

|

| AlbR Capital Limited

Gavin Burnell / Colin Rowbury / Jon Belliss

|

Tel: +44 (0) 207 4690930

|

| Brand Communications (Public & Investor Relations)

Alan Green |

Tel: +44 (0) 7976 431608

|

URU Metals #URU – Ground-Based Geophysical Survey to Start Following Completion of Line Preparation

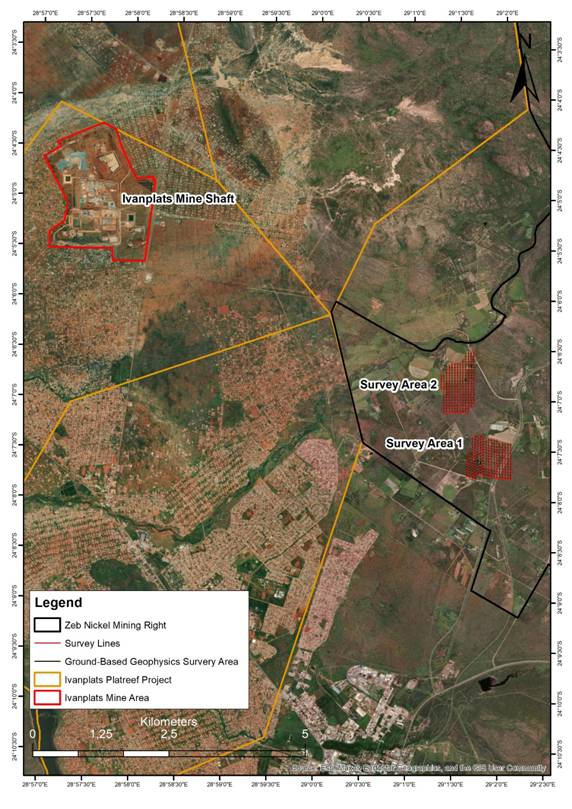

URU Metals Limited (“URU” or the “Company”) is pleased to announce that line preparation has been completed across both priority survey areas for the planned ground-based geophysical programme at the Zeb Nickel Project.

URU Metals Limited (“URU” or the “Company”) is pleased to announce that line preparation has been completed across both priority survey areas for the planned ground-based geophysical programme at the Zeb Nickel Project.

The ground-based gravity survey is scheduled to commence today, 15 April 2026, with the frequency-domain electromagnetic (“FDEM”) survey expected to commence shortly thereafter. The programme forms part of the next phase of exploration aimed at enhancing the resolution of the previously completed airborne geophysical surveys.

The airborne programme successfully identified several compelling coincident gravity-magnetic-electromagnetic anomalies interpreted to be associated with a magmatic conduit system linking the Uitloop ultramafic bodies. The higher-resolution ground-based surveys are expected to refine these anomalies, improve target definition, and better constrain the geometry of conductive bodies potentially associated with semi-massive nickel sulphide mineralisation.

The results of the gravity and FDEM surveys will support prioritisation of drill targets and maximise the effectiveness of the Company’s upcoming drilling campaign.

Figure 1: Map showing the ground-based geophysical survey areas, including the adjacent Ivanplats Mining Right and mine shaft. The gravity survey along the planned lines commenced on 15 April 2026.

CEO John Zorbas commented: “We are very pleased to have completed line preparation across both survey areas and to now be commencing the ground-based geophysical programme. While the airborne programme successfully identified several compelling targets, the higher-resolution ground surveys will allow us to sharpen our focus on the most prospective semi-massive nickel sulphide targets. This work is designed to maximise the effectiveness of our upcoming drilling campaign. We are very excited about the progress being made and look forward to the coming weeks and months as the surveys advance. We will continue to provide shareholders with regular updates as results become available.”

About the Company

URU Metals is a mineral exploration and development company focused on advancing high-potential critical metals projects in South Africa. The Company is committed to creating sustainable value through responsible mining practices, regulatory compliance, and active stakeholder engagement. For more information, visit www.urumetals.com

For further information, please contact:

URU Metals Limited

John Zorbas

(Chief Executive Officer)

+1 416 504 3978

SP Angel Corporate Finance LLP

(Nominated Adviser and Broker)

Ewan Leggat / Caroline Rowe / Devik Mehta

+ 44 (0) 203 470 0470

#FDR First Development Resources PLC – Selta Project – GAIP survey update

![]() First Development Resources plc (AIM: FDR), the UK-based, Australia-focused exploration company with mineral interests in the Northern Territory and Western Australia, is pleased to provide an update on the Gradient Array Induced Polarisation (“GAIP”) geophysical survey at its Lander West gold target, part of the Company’s 100%-owned Selta Project in Australia’s Northern Territory.

First Development Resources plc (AIM: FDR), the UK-based, Australia-focused exploration company with mineral interests in the Northern Territory and Western Australia, is pleased to provide an update on the Gradient Array Induced Polarisation (“GAIP”) geophysical survey at its Lander West gold target, part of the Company’s 100%-owned Selta Project in Australia’s Northern Territory.

HIGHLIGHTS

· GAIP survey has recommenced following temporary suspension, as improved weather conditions allow for safe access and mobilisation back to site.

· Programme refined to prioritise key prospective areas, following weather-related delays, with the aim of maintaining technical objectives while improving efficiency.

· One-third of the survey remains outstanding, with completion anticipated within approximately 2 weeks and results intended to inform the next phase of exploration.

Tristan Pottas, Chief Executive Officer of FDR, commented:

“After an unusually heavy rainy season we are pleased to see improving conditions at Selta, allowing our team to safely return to site and resume the GAIP survey at Lander West. While the weather-related delays were unavoidable, they have provided an opportunity to refine the survey scope and focus on the most prospective zones within the target area.

This approach is expected to deliver high-quality geophysical data in a shorter timeframe, supporting our objective of defining robust drill targets. We look forward to completing the programme over the coming weeks and progressing Lander West to the next stage of exploration.”

OPERATIONAL UPDATE

The GAIP geophysical survey at the Lander West gold target commenced in early January 2026 and is designed to complement previously completed high-resolution aeromagnetic and radiometric geophysical surveys. The programme aims to enhance the Company’s understanding of subsurface geology and structural architecture across the target area, supporting the refinement of potential drill targets.

Unusually heavy seasonal rains resulted in adverse weather conditions across large parts of Central Australia and caused a temporary suspension of the GAIP survey. As a safety precaution in early February, the Company paused field operations and demobilised the survey team, with flooding rendering access tracks impassable, particularly at creek crossings.

The geophysical team has remobilised and the survey has recommenced with a refined scope to focus on the most prospective areas within the Lander West gold target. Approximately 33% of the refined survey area remains to be completed and is anticipated to take around two weeks. The Company expects the refined dataset to provide sufficient geophysical coverage to advance the Lander West gold target to the next phase of exploration.

For further information visit www.firstdevelopmentresources.com or contact the following:

|

First Development Resources plc Tristan Pottas (CEO) |

Tel: +44 (0) 20 3778 1397 |

ABOUT REACH ANNOUNCEMENTS

This is a Reach announcement. Reach is an investor communication service aimed at assisting listed and unlisted (including AIM quoted) companies to distribute media only / non-regulatory news releases into the public domain. Information required to be notified under the AIM Rules for Companies, Market Abuse Regulation or other regulation would be disseminated as an RNS regulatory announcement and not on Reach.

ABOUT FIRST DEVELOPMENT RESOURCES

First Development Resources’ assets comprise eight granted tenements covering a total area of 2,314.4km2. Five of the tenements, comprising three prospective copper-gold projects, are located in Western Australia (WA) while the remaining three tenements, comprising a rare-earth element (REE), uranium, lithium and gold project, are located in the Australia’s Northern Territory. All tenements are wholly owned by FDR. The assets are a mixture of drill ready and earlier stage exploration.

The WA Projects include the Company’s Wallal Project as well as Ripon Hills and Braeside West Projects situated in the Paterson Province, which is widely regarded as one of the most productive regions in Australia for the discovery of world-class gold-copper deposits, and which is home to several world-class mines and more recent discoveries.

The Selta Project in the Northern Territory is located in an area considered highly prospective for uranium and rare-earth element mineralisation along with base and precious metal mineralisation. Numerous companies are actively exploring within the region.

Beyond the existing portfolio, FDR is actively looking to expand its portfolio through the acquisition of early-stage exploration projects in Australia.

Quoted Micro 13 April 2026

AQUIS STOCK EXCHANGE

AQUIS STOCK EXCHANGE

Oscillate (SRVL), which is changing its name to Serval Resources, raised £34,000 in its retail offer at 22.5p/share, which is below the maximum level of £300,000. It is acquiring Kalahari Copper and moving to AIM on 27 April.

Digital assets investor Valereum (VLRM) has received confirmation that the $300,000 cash element of the coupon is being paid in instalments over four days. Further amounts due from strategic partner Quorum Global Photonics (QGP), which is a 49.7% shareholder, are expected to be paid under the $200m royalty and streaming financing agreement. Pieter Scholtz and Gerhard Kotzee are directors of both companies.

Wishbone Gold (WSBN) plans to acquire the Silver Lake project in Western Australia. Before that happens, historic data will be further analysed. If it goes ahead 3.57 million shares will be issued for the acquisition.

Hot Rocks Investments (HRIP) has made new investments in Central Gold, Futuro Resources and Cobra Resources (COBR). Investee company Mendell Helium (MDH) is moving from Aquis to AIM, and 49%-owned Sunshine Gold Capital has been granted a third tenement as part of the Dexter gold project, which is near to two existing gold mines in Western Australia.

Stack BTC (STAK) made a loss of £110,000 in the six months to January 2026. There was cash of £51,000 at the end of January 2026 and since then £4.28m has been raised. There have been 31 Bitcoin acquired. The focus is finding a business to acquire.

Ethtry (ETHY) has spent £100,000 to buy 66.6737 Ethereum. It owns 816.6737 Ethereum.

Cooks Coffee Company (COOK) was franchisor of the year (expanding food and non-food) in the 2026 Irish Franchise Association Awards, and a franchisee was named franchisee of the year.

Shepherd Neame (SHEP) non-exec director George Barnes bought 2,173 shares at 458p each. Falconedge (EDGE) chief executive Roy Kashi and family have bought 2.9 million shares for an average of just over 1p each. The total holding has risen to 6.45%. EPE Special Opportunities (LON: EO.P) directors Clive Spears and David Pirouet each bought 5,968 shares at 176p and 168p respectively.

TechFinancials has changed its name to Ubuntu Mining and Metals Inc (UNTU).

ASSET MATCH

Brewer Wadworth and Company (WAD) says 2025 accounts should be published later in April. Strong Christmas trading meant like-for-like sales were 7% ahead. Beer volumes were 16% higher in the first two months of the year as the company sold more of its beer via its own pubs. Like-for-like sales of the group are 4% higher, but margins are under pressure even though gas and electricity costs are set until 2029. One pub was sold in January.

AIM

RentGuarantor (RGG) growth is accelerating with first quarter revenues more than doubling to £880,000 and this has sparked an upgrade. New partners have been brought onboard. It is also offering a new product with mydeposits that combines insuring rent deposits with the rent guarantee service. Allenby has increased its 2026 pre-tax profit forecast by 26% to £300,000. This would be a maiden profit.

Van Elle (VANL) is recommending a 52.3p/share cash bid from STRABAG UK, which values the ground engineering company at £58.8m. The share price has not been that high for more than three years. The directors had talks with other suitors before receiving this bid approach. Vienna-based STRABAG provides construction services, and it was seeking to expand in the UK.

Alien Metals (UFO) says joint venture partner GreenTech Minerals has identified material upside potential for the Munni Munni Platinum-Palladium-Copper-Nickel project in Western Australia not included in the current mineral resource estimate of 24Mt @ 2.9 g/t PGE₄ for 2.2Moz. Alien Metals has a 30% interest and a free carry until completion of a bankable feasibility study. High grade zones have been identified and there is potential for open pit mining. The results of the maiden drilling programme should be announced later this month. Joint venture partner West Coast Silver has announced a 1,500 metre drilling programme for the Elizabeth Hill silver project in Western Australia.

Data analysis software and services provider Celebrus Technologies (CLBS) says full year revenues are broadly in line with expectations at $23.3m, down from $38.7m because of a change in business model, and the loss will be around $200,000. Annualised recurring revenues grew from $13.6m to $15m. Two bank customers sold off parts of their businesses, so their payments were reduced. Some expected deals at contracted stage were lost or delayed and Celebrus Technologies is improving its skills in winning new clients. Cash was $32m at the end of March 2026. Another loss is anticipated for 2026-27.

Mercantile Ports and Logistics (MPL) is pursuing legal remedies to regain control of port operating subsidiary, Karanja Terminal & Logistics. One bank did not sanction an agreement for a one-time settlement of company debt with the consortium of banks. The court has told the Committee of Creditors holding the company debt to consider an offer to redeem 100% of outstanding debt. There has been no progress and there are potential buyers interested in the assets. An international oil and gas company is a potential provider of funds to help redeem the debt. A meeting was held to consider Mercantile’s proposal on Friday 10 April.

The shares of Secure Property Development and Investment (SPDI) returned from suspension. The property company amended heads of agreement with energy storage technology developer Adven, which it is proposed will acquired SPDI, so it is not a reverse takeover anymore. Instead, Adven intends to join AIM and launch a share exchange for SPDI. Adven can then raise money via EIS.

Steppe Cement (STCM) has increased cement sales in Kazakhstan in the first quarter of 2026 to 344,058 tonnes, from 276,217 tonnes in the same period last year. The average price was one-fifth higher at around $57/tonne. Market share increased to 16%. Capacity is being increased and the final estimated cost is $35m.

Atome (ATOM) is in the final stages of negotiations for the funding of the Villeta fertiliser project in Paraguay. Definitive documentation with the equity consortium is expected by 17 April. The potential funders are likely to be at the IMF and World Bank spring meetings at that time.

Physiomics (PYC) has accepted a general meeting request from Michael Whitlow, who owns 13.7%, and the meeting is on29 April. Michael Whitlow wanted to appoint Nicholas Tulloch, Ian Bagnall, Martin Gouldstone (later removed) and himself as directors and remove Dr Jim Millen, Shalabh Kumar, Dr Tim Corn, and Dr Peter Sargent, as long as least two of the new directors are appointed. The board did offer to appoint two non-execs to replace two existing ones, but it felt that the remuneration requested was too high. The board believes that the disruption could hamper the ability to commercialise its IP. They are asking shareholders to vote against the resolutions.

Quantum Blockchain Technologies (QBT) says a court has stopped enforcement of a €6m plus damages award against Sipiem relating to the Mediapolis business. The company has not been able to enforce the seizing of property of a former Sipiem director because he has declared bankruptcy. The liquidation of Mediapolis is being completed and a further distribution of €132,000 is expected to be received by the end of June.

MAIN MARKET

Financial management software developer Aptitude Software (LSE: APTD) has decided to seek a potential purchaser as well as considering other options for the business. It is possible that other businesses would be sold to concentrate on Fynapse. The refocus on that product led to a 1% dip to £49.8m even though Fynapse sales were higher. Recurring revenues were £54.4m and operating profit was flat at £10m. Net cash is £21.2m. The dividend is 5.4p/share.

Solvonis Therapeutics (SVNS) has been granted a US patent for its PTSD programme. The patent covers a chemically distinct monoamine modulator series designed to modulate serotonin, dopamine and noradrenaline transporter systems (SERT, DAT and NET) and lasts February 2043.

Andrew Hore