Introduction from new Anglesey Mining #AYM CEO Rob Marsden

An introduction from new Anglesey Mining #AYM CEO Rob Marsden from Parys Mountain

- Rob provides an overview of his CV, along with a brief overview of Parys Mountain mine and the surrounding area

- A brief overview of today’s assay results that “demonstrate good continuity, supporting the integrity of the geological model”

- Litho geochemical results from all three holes due in the coming weeks

- Targeting a resource update on the Northern Copper Zone

Anglesey Mining #AYM – Further drilling results confirm scale of Northern Copper Zone at Parys Mountain

![]() Anglesey Mining plc (AIM:AYM), is pleased to announce that assay results have been received for the recently completed drill hole NCZ003. Drill hole NCZ003 was the third hole to be completed from the infill drilling program of the Northern Copper Zone (NCZ) and Garth Daniel Zone (GDZ) at the Company’s Parys Mountain Cu-Zn-Pb-Ag-Au VMS project on the Isle of Anglesey in North West Wales.

Anglesey Mining plc (AIM:AYM), is pleased to announce that assay results have been received for the recently completed drill hole NCZ003. Drill hole NCZ003 was the third hole to be completed from the infill drilling program of the Northern Copper Zone (NCZ) and Garth Daniel Zone (GDZ) at the Company’s Parys Mountain Cu-Zn-Pb-Ag-Au VMS project on the Isle of Anglesey in North West Wales.

Consistent both with historical drilling and the recently completed NCZ001 and NCZ002 holes, the assays confirm NCZ003 intersected a significant zone of mineralisation across the NCZ with 90m @ 0.57% CuEq (including internal dilution). Drill hole NCZ003 was terminated prematurely at a depth of 535m due to a large, potentially fault-related void. The last 6 metres of core prior to the 4m void assayed 1.16% CuEq and coincides with previous high-grade assays from historic drilling.

As with the previous two holes in the program, NCZ003 intersected both broad zones of mineralisation and multiple higher-grade zones. Importantly, the drilling is demonstrating good continuity and further supports the integrity of the geological model and drill targeting, with indications of greater mineralised volumes overall.

Key intersections within the broad zone of mineralisation are detailed below:

Northern Copper Zone – Hole NCZ003

- 0m @ 0.51% Cu, 0.06% Zn, 0.03% Pb, 2.16g/t Ag and 0.14g/t Au (0.57% CuEq) from a depth of 389m, including:

- 0m @ 0.80% Cu, 2.19g/t Ag and 0.16g/t Au (0.82% CuEq) from 427.0m

- 0m @ 0.99% Cu, 4.33g/t Ag and 0.15g/t Au (1.08% CuEq) from 449.0m

- 0m @ 0.47% Cu, 1.53g/t Ag and 0.07g/t Au (0.49% CuEq) from 490.0m, including 4.0m @ 0.48% Cu, 2.48g/t Ag and 0.13g/t Au (0.53% CuEq)

- 0m @ 1.20% Cu, 1.10g/t Ag and 0.01g/t Au (1.16% CuEq) from 529m (hole stopped in mineralisation)

***CuEq grades are based on recovery factors and commodity prices as detailed after the tabulated reported assays of this release***

The third drill hole, NCZ003, concludes the on-site portion of the current exploration and infill drilling program and we are expecting litho-geochemical analysis results, from each of the three holes, to be back from the laboratory in Canada in the coming weeks. Subsequently, on the strength of all the data collected and the interpretation thereof, the Company is targeting a resource update on the NCZ, with the aim of converting a significant portion of the Inferred Resource into the higher confidence Indicated category. Based on the Joint Ore Reserve Committee (JORC) guidelines, only Indicated and Measured category Mineral Resources can be converted into Ore Reserves.

Andrew King, Interim Chairman of Anglesey Mining, commented: “Once again, we are very pleased to see the Parys Mountain project delivering some very strong drilling results. It is worth reminding investors that Parys Mountain is demonstrably the largest and most advanced copper project in the UK with substantial resource upside still evident. In addition, the project is favourably located on a previously permitted, brownfield development site with significant existing infrastructure already in place.“

“All three holes in the current program; NCZ001 NCZ002 and NCZ003 have delivered some exceptional high-grade copper intersections within broad thicknesses of mineralisation up to 100m wide. The results continue to support our view that the NCZ provides significant upside for the Parys Mountain project, over and above the 5 million tonne contribution included within the 2021 Preliminary Economic Assessment.”

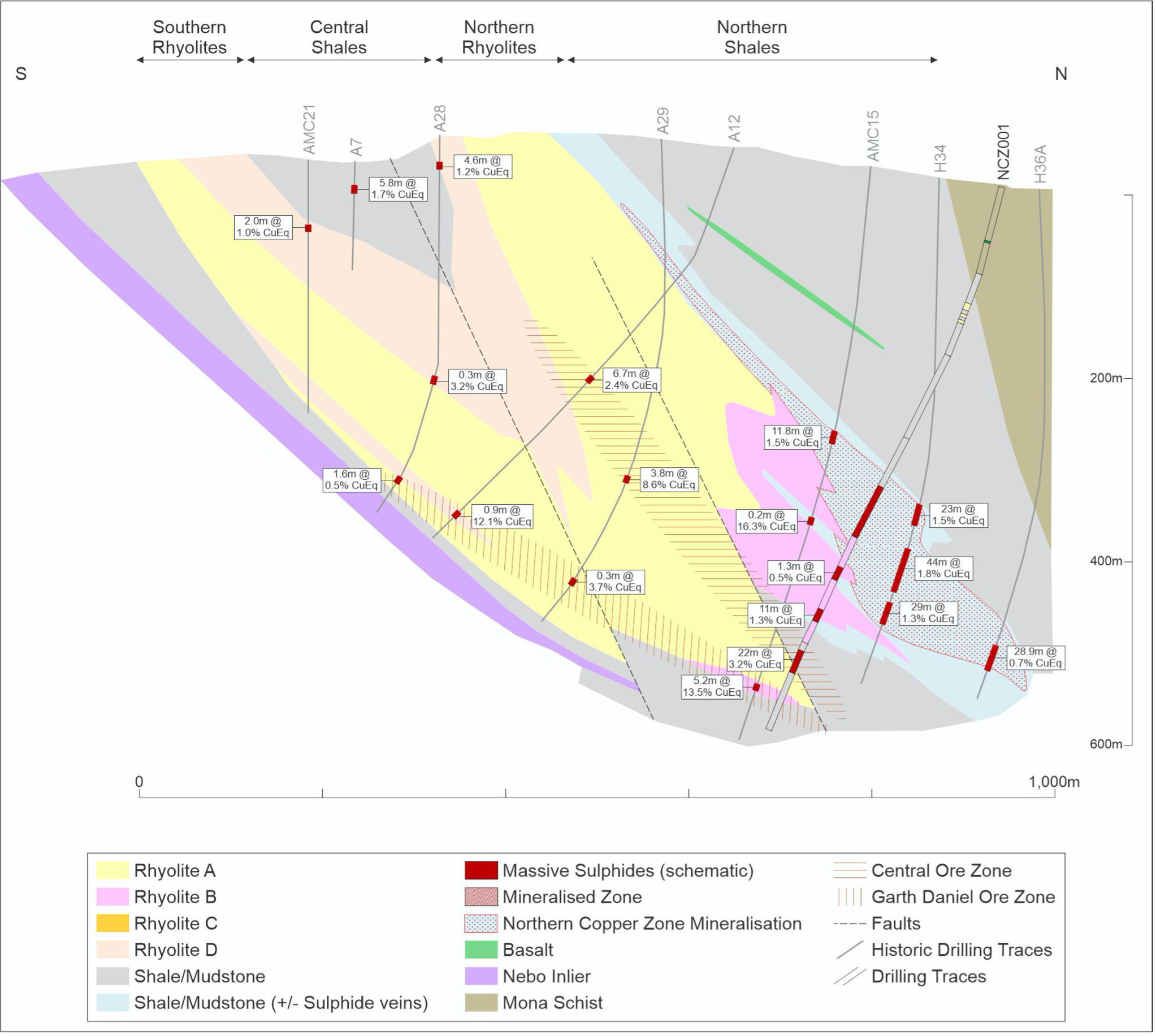

NCZ – Cross Section 4600mE

Section 4600mE below highlights the position of the recently completed drill hole NCZ002 and NCZ003.

The interpreted outline of the NCZ in the cross-section does not imply an economic outcome, it simply highlights where sulphides have been identified within the Northern Shales with a 0.5% CuEq cut-off. A significant number of the drill holes within this zone have returned consistent zones of higher-grade material, which was a key target of the program. The recognition of a shear zone along the hanging wall of the NCZ could imply a structural emplacement, or thickening of the sequence within the mine environment and will greatly assist with future targeting and drilling.

Importantly, every hole drilled into the interpreted position of the NCZ has intersected broad zones of sulphides; the drilling has demonstrated the predictability of the mineralised zone from the detailed geological model that has been constructed and refined over several years.

The most recent drill hole, NCZ003, targeted the up-dip area above historical hole H17A and has provided important additional information relating to the key lithology Rhyolite B – the emplacement of this unit is closely associated to the mineralising event. This additional information will now be incorporated into the geological model and the resource block model of the NCZ.

Drill hole NCZ003 ended prematurely at a depth of 535m due to faulted ground conditions and the intersection of a 4m void. The last metre of core prior to the void assayed 1.3% Cu and 1.22% CuEq. The location of the void correlates to the contact position of Rhyolite B and the host northern shale unit, which has traditionally been a zone related to higher grade intersections – drill hole A15 intersected 1.6m @ 3.7% CuEq approximately 100m up-dip from NCZ003 and NCZ001 intersected 22.0m @ 3.2% CuEq on section 4800mE (200m along strike).

NCZ – Cross Section 4800mE

Section 4800mE below highlights the position of drill hole NCZ001.

As per section 4600mE, this section also highlights the continuity of sulphide mineralisation across the NCZ. With the completion of NCZ003, the Company has gained a greater understanding of the influence from Rhyolite B on the higher-grade zones of mineralisation.

Section 4800mE also highlights the potential related to the Central Zone with significant intersections from historical 1970’s drilling, including 3.8m @ 8,6% Cu and 6.7m @ 2.4% Cu. The Company believes potential exists for these intersections to link to the 22m @ 3.2 % CuEq (including 4.0m @ 5.2% Cu) in NCZ001.

Drill hole details:

| Hole ID | Co-ordinates

(E) (N) |

Elevation

(m) |

Azimuth

(°) |

Dip (°) | End of Hole (m) | |

| NCZ003 | 243806.92 | 390948.57 | 73.09 | 165 | -72 | 535 |

Reported Assays (results >0.5 CuEq in bold):

| Hole Number | From | To | Sample Length | Assays | |||||

| (m) | (m) | (m) | Cu

(%) |

Zn

(%) |

Pb

(%) |

Ag (g/t) | Au (g/t) | CuEq

(%)* |

|

| NCZ003 | 264.4 | 264.8 | 0.4 | 0.02 | 1.34 | 0.26 | 3.6 | 0.11 | 0.42% |

| NCZ003 | 339.8 | 340.3 | 0.5 | 0.00 | 0.00 | 0.01 | 0.5 | 0.01 | 0.01% |

| NCZ003 | 340.3 | 340.8 | 0.5 | 0.00 | 0.00 | 0.01 | 0.5 | 0.01 | 0.01% |

| NCZ003 | 340.8 | 341.3 | 0.5 | 0.00 | 0.00 | 0.01 | 0.5 | 0.01 | 0.01% |

| NCZ003 | 385 | 386 | 1 | 0.12 | 0.00 | 0.01 | 0.5 | 0.02 | 0.12% |

| NCZ003 | 386 | 387 | 1 | 0.38 | 0.00 | 0.01 | 0.7 | 0.02 | 0.37% |

| NCZ003 | 387 | 388 | 1 | 0.50 | 0.02 | 0.05 | 1.9 | 0.12 | 0.54% |

| NCZ003 | 388 | 389 | 1 | 0.36 | 0.01 | 0.09 | 1.1 | 0.12 | 0.42% |

| NCZ003 | 389 | 390 | 1 | 0.50 | 0.01 | 0.05 | 1.4 | 0.11 | 0.53% |

| NCZ003 | 390 | 391 | 1 | 0.25 | 0.00 | 0.03 | 1.0 | 0.18 | 0.32% |

| NCZ003 | 391 | 392 | 1 | 0.27 | 0.01 | 0.05 | 1.0 | 0.05 | 0.29% |

| NCZ003 | 392 | 393 | 1 | 0.44 | 0.01 | 0.04 | 1.5 | 0.41 | 0.60% |

| NCZ003 | 393 | 394 | 1 | 1.90 | 0.00 | 0.09 | 2.2 | 0.12 | 1.85% |

| NCZ003 | 394 | 395 | 1 | 0.04 | 0.00 | 0.01 | 0.5 | 0.06 | 0.07% |

| NCZ003 | 395 | 396 | 1 | 0.67 | 0.00 | 0.01 | 1.1 | 0.11 | 0.68% |

| NCZ003 | 396 | 397 | 1 | 0.33 | 0.00 | 0.00 | 1.1 | 0.32 | 0.45% |

| NCZ003 | 397 | 398 | 1 | 0.10 | 0.02 | 0.06 | 0.8 | 0.16 | 0.18% |

| NCZ003 | 398 | 399 | 1 | 0.18 | 0.01 | 0.02 | 0.8 | 0.06 | 0.20% |

| NCZ003 | 399 | 400 | 1 | 0.02 | 0.00 | 0.01 | 0.5 | 0.06 | 0.05% |

| NCZ003 | 400 | 401 | 1 | 0.32 | 0.01 | 0.01 | 1.2 | 0.18 | 0.38% |

| NCZ003 | 401 | 402 | 1 | 0.33 | 0.01 | 0.01 | 1.7 | 0.20 | 0.40% |

| NCZ003 | 402 | 403 | 1 | 0.34 | 0.00 | 0.01 | 1.1 | 0.10 | 0.37% |

| NCZ003 | 403 | 404 | 1 | 0.29 | 0.01 | 0.01 | 1.2 | 0.08 | 0.31% |

| NCZ003 | 404 | 405 | 1 | 2.80 | 0.02 | 0.01 | 4.2 | 0.28 | 2.75% |

| NCZ003 | 405 | 406 | 1 | 0.26 | 0.02 | 0.01 | 1.5 | 0.10 | 0.30% |

| NCZ003 | 406 | 407 | 1 | 0.27 | 0.01 | 0.01 | 2.6 | 0.25 | 0.37% |

| NCZ003 | 407 | 408 | 1 | 0.32 | 0.00 | 0.01 | 1.0 | 0.07 | 0.33% |

| NCZ003 | 408 | 409 | 1 | 0.23 | 0.00 | 0.01 | 0.8 | 0.14 | 0.28% |

| NCZ003 | 409 | 410 | 1 | 0.08 | 0.00 | 0.01 | 0.5 | 0.11 | 0.13% |

| NCZ003 | 410 | 411 | 1 | 0.62 | 0.01 | 0.01 | 2.0 | 0.49 | 0.79% |

| NCZ003 | 411 | 412 | 1 | 0.11 | 0.00 | 0.01 | 0.5 | 0.03 | 0.11% |

| NCZ003 | 412 | 413 | 1 | 0.19 | 0.01 | 0.01 | 0.9 | 0.12 | 0.24% |

| NCZ003 | 413 | 414 | 1 | 0.17 | 0.02 | 0.01 | 1.3 | 0.16 | 0.24% |

| NCZ003 | 414 | 415 | 1 | 0.29 | 0.00 | 0.00 | 0.8 | 0.10 | 0.31% |

| NCZ003 | 415 | 416 | 1 | 0.33 | 0.00 | 0.01 | 0.7 | 0.15 | 0.37% |

| NCZ003 | 416 | 417 | 1 | 1.14 | 0.01 | 0.02 | 1.8 | 0.15 | 1.14% |

| NCZ003 | 417 | 418 | 1 | 0.09 | 0.01 | 0.01 | 0.5 | 0.09 | 0.12% |

| NCZ003 | 418 | 419 | 1 | 0.50 | 0.01 | 0.01 | 1.8 | 0.09 | 0.52% |

| NCZ003 | 419 | 420 | 1 | 0.66 | 0.02 | 0.01 | 2.4 | 0.18 | 0.70% |

| NCZ003 | 420 | 421 | 1 | 0.25 | 0.01 | 0.01 | 1.0 | 0.08 | 0.28% |

| NCZ003 | 421 | 422 | 1 | 0.56 | 0.01 | 0.01 | 2.4 | 0.19 | 0.61% |

| NCZ003 | 422 | 423 | 1 | 0.76 | 0.01 | 0.01 | 2.6 | 0.24 | 0.83% |

| NCZ003 | 423 | 424 | 1 | 0.16 | 0.01 | 0.01 | 1.5 | 0.06 | 0.19% |

| NCZ003 | 424 | 425 | 1 | 0.05 | 0.01 | 0.01 | 1.2 | 0.11 | 0.10% |

| NCZ003 | 425 | 426 | 1 | 0.41 | 0.01 | 0.04 | 1.1 | 0.05 | 0.43% |

| NCZ003 | 426 | 427 | 1 | 0.17 | 0.00 | 0.01 | 0.7 | 0.08 | 0.20% |

| NCZ003 | 427 | 428 | 1 | 0.92 | 0.02 | 0.01 | 2.8 | 0.13 | 0.93% |

| NCZ003 | 428 | 429 | 1 | 0.86 | 0.00 | 0.01 | 1.5 | 0.10 | 0.86% |

| NCZ003 | 429 | 430 | 1 | 1.82 | 0.01 | 0.01 | 2.8 | 0.13 | 1.77% |

| NCZ003 | 430 | 431 | 1 | 1.41 | 0.04 | 0.01 | 4.2 | 0.19 | 1.43% |

| NCZ003 | 431 | 432 | 1 | 0.48 | 0.01 | 0.01 | 1.5 | 0.10 | 0.50% |

| NCZ003 | 432 | 433 | 1 | 0.07 | 0.00 | 0.00 | 0.6 | 0.05 | 0.09% |

| NCZ003 | 433 | 434 | 1 | 0.27 | 0.01 | 0.01 | 2.0 | 0.43 | 0.44% |

| NCZ003 | 434 | 435 | 1 | 0.53 | 0.01 | 0.00 | 2.1 | 0.15 | 0.57% |

| NCZ003 | 435 | 436 | 1 | 0.29 | 0.06 | 0.21 | 4.5 | 0.30 | 0.49% |

| NCZ003 | 436 | 437 | 1 | 0.12 | 0.01 | 0.01 | 2.2 | 0.15 | 0.19% |

| NCZ003 | 437 | 438 | 1 | 0.11 | 0.00 | 0.01 | 1.1 | 0.14 | 0.17% |

| NCZ003 | 438 | 439 | 1 | 0.21 | 0.02 | 0.00 | 1.7 | 0.09 | 0.25% |

| NCZ003 | 439 | 440 | 1 | 0.04 | 0.01 | 0.01 | 1.4 | 0.10 | 0.09% |

| NCZ003 | 440 | 441 | 1 | 0.05 | 0.00 | 0.00 | 0.9 | 0.08 | 0.09% |

| NCZ003 | 441 | 442 | 1 | 0.09 | 0.00 | 0.00 | 1.0 | 0.07 | 0.12% |

| NCZ003 | 442 | 443 | 1 | 0.80 | 0.01 | 0.00 | 2.4 | 0.19 | 0.84% |

| NCZ003 | 443 | 444 | 1 | 0.37 | 0.01 | 0.00 | 2.0 | 0.19 | 0.43% |

| NCZ003 | 444 | 445 | 1 | 0.38 | 0.04 | 0.04 | 4.3 | 0.36 | 0.55% |

| NCZ003 | 445 | 446 | 1 | 0.18 | 0.01 | 0.01 | 1.6 | 0.13 | 0.24% |

| NCZ003 | 446 | 447 | 1 | 0.31 | 0.01 | 0.00 | 2.0 | 0.14 | 0.36% |

| NCZ003 | 447 | 448 | 1 | 0.53 | 0.09 | 0.27 | 4.8 | 0.16 | 0.68% |

| NCZ003 | 448 | 449 | 1 | 0.24 | 0.01 | 0.17 | 1.6 | 0.10 | 0.32% |

| NCZ003 | 449 | 450 | 1 | 2.10 | 0.02 | 0.03 | 7.1 | 0.40 | 2.17% |

| NCZ003 | 450 | 451 | 1 | 0.51 | 0.01 | 0.02 | 2.3 | 0.18 | 0.57% |

| NCZ003 | 451 | 452 | 1 | 1.60 | 0.28 | 0.80 | 7.1 | 0.13 | 1.87% |

| NCZ003 | 452 | 453 | 1 | 0.95 | 0.03 | 0.26 | 5.3 | 0.21 | 1.08% |

| NCZ003 | 453 | 454 | 1 | 0.49 | 0.06 | 0.20 | 3.1 | 0.08 | 0.58% |

| NCZ003 | 454 | 455 | 1 | 0.14 | 0.01 | 0.02 | 1.0 | 0.06 | 0.16% |

| NCZ003 | 455 | 456 | 1 | 0.29 | 0.12 | 0.22 | 5.9 | 0.06 | 0.42% |

| NCZ003 | 456 | 457 | 1 | 0.30 | 0.08 | 0.08 | 2.1 | 0.13 | 0.38% |

| NCZ003 | 457 | 458 | 1 | 2.55 | 0.07 | 0.16 | 5.1 | 0.09 | 2.50% |

| NCZ003 | 458 | 459 | 1 | 0.28 | 0.06 | 0.12 | 3.0 | 0.16 | 0.39% |

| NCZ003 | 459 | 460 | 1 | 0.70 | 0.04 | 0.09 | 5.4 | 0.19 | 0.79% |

| NCZ003 | 460 | 461 | 1 | 0.76 | 0.03 | 0.02 | 3.5 | 0.17 | 0.80% |

| NCZ003 | 461 | 462 | 1 | 0.64 | 0.01 | 0.01 | 1.7 | 0.14 | 0.67% |

| NCZ003 | 462 | 463 | 1 | 0.39 | 0.01 | 0.01 | 1.7 | 0.08 | 0.40% |

| NCZ003 | 463 | 464 | 1 | 0.13 | 0.26 | 0.53 | 2.9 | 0.06 | 0.36% |

| NCZ003 | 464 | 465 | 1 | 0.13 | 0.06 | 0.19 | 1.8 | 0.03 | 0.21% |

| NCZ003 | 465 | 466 | 1 | 1.10 | 0.12 | 0.04 | 5.4 | 0.10 | 1.13% |

| NCZ003 | 466 | 467 | 1 | 0.42 | 0.04 | 0.08 | 3.9 | 0.10 | 0.48% |

| NCZ003 | 467 | 468 | 1 | 0.18 | 0.00 | 0.07 | 0.7 | 0.02 | 0.20% |

| NCZ003 | 468 | 469 | 1 | 0.31 | 0.02 | 0.05 | 1.9 | 0.03 | 0.33% |

| NCZ003 | 469 | 470 | 1 | 0.14 | 0.09 | 0.18 | 1.9 | 0.08 | 0.24% |

| NCZ003 | 470 | 471 | 1 | 0.10 | 0.03 | 0.14 | 1.1 | 0.02 | 0.16% |

| NCZ003 | 471 | 472 | 1 | 1.71 | 0.05 | 0.09 | 6.4 | 0.05 | 1.68% |

| NCZ003 | 472 | 473 | 1 | 0.12 | 0.01 | 0.01 | 0.8 | 0.06 | 0.14% |

| NCZ003 | 473 | 474 | 1 | 0.15 | 0.01 | 0.01 | 0.9 | 0.04 | 0.16% |

| NCZ003 | 474 | 475 | 1 | 0.71 | 0.02 | 0.05 | 1.7 | 0.13 | 0.74% |

| NCZ003 | 475 | 476 | 1 | 0.58 | 0.02 | 0.01 | 3.2 | 0.17 | 0.63% |

| NCZ003 | 476 | 477 | 1 | 0.07 | 0.01 | 0.06 | 0.8 | 0.04 | 0.11% |

| NCZ003 | 477 | 478 | 1 | 0.82 | 0.04 | 0.05 | 3.5 | 0.16 | 0.87% |

| NCZ003 | 478 | 479 | 1 | 1.37 | 0.02 | 0.04 | 3.5 | 0.08 | 1.34% |

| NCZ003 | 479 | 480 | 1 | 0.10 | 0.01 | 0.05 | 0.8 | 0.04 | 0.12% |

| NCZ003 | 480 | 481 | 1 | 0.04 | 0.03 | 0.06 | 0.7 | 0.03 | 0.07% |

| NCZ003 | 481 | 482 | 1 | 0.13 | 0.01 | 0.02 | 0.5 | 0.03 | 0.14% |

| NCZ003 | 482 | 483 | 1 | 0.38 | 0.01 | 0.02 | 1.3 | 0.05 | 0.39% |

| NCZ003 | 483 | 484 | 1 | 0.07 | 0.00 | 0.01 | 0.5 | 0.01 | 0.08% |

| NCZ003 | 484 | 485 | 1 | 0.02 | 0.00 | 0.01 | 0.5 | 0.01 | 0.03% |

| NCZ003 | 485 | 486 | 1 | 0.40 | 0.00 | 0.01 | 0.6 | 0.03 | 0.39% |

| NCZ003 | 486 | 487 | 1 | 0.03 | 0.00 | 0.01 | 0.5 | 0.02 | 0.04% |

| NCZ003 | 487 | 488 | 1 | 0.02 | 0.13 | 0.06 | 0.8 | 0.02 | 0.07% |

| NCZ003 | 488 | 489 | 1 | 0.19 | 0.01 | 0.02 | 0.5 | 0.03 | 0.19% |

| NCZ003 | 489 | 490 | 1 | 0.15 | 0.00 | 0.01 | 0.5 | 0.02 | 0.15% |

| NCZ003 | 490 | 491 | 1 | 0.63 | 0.03 | 0.01 | 4.1 | 0.19 | 0.69% |

| NCZ003 | 491 | 492 | 1 | 0.51 | 0.07 | 0.02 | 4.0 | 0.26 | 0.63% |

| NCZ003 | 492 | 493 | 1 | 0.13 | 0.01 | 0.07 | 0.9 | 0.04 | 0.16% |

| NCZ003 | 493 | 494 | 1 | 0.66 | 0.00 | 0.01 | 0.9 | 0.02 | 0.63% |

| NCZ003 | 494 | 495 | 1 | 0.09 | 0.06 | 0.05 | 1.0 | 0.04 | 0.13% |

| NCZ003 | 495 | 496 | 1 | 0.01 | 0.01 | 0.01 | 0.5 | 0.02 | 0.03% |

| NCZ003 | 496 | 497 | 1 | 0.31 | 0.01 | 0.01 | 1.2 | 0.06 | 0.32% |

| NCZ003 | 497 | 498 | 1 | 0.83 | 0.02 | 0.01 | 1.7 | 0.04 | 0.81% |

| NCZ003 | 498 | 499 | 1 | 0.63 | 0.01 | 0.01 | 1.1 | 0.05 | 0.61% |

| NCZ003 | 499 | 500 | 1 | 0.03 | 0.00 | 0.01 | 0.5 | 0.01 | 0.04% |

| NCZ003 | 500 | 501 | 1 | 0.47 | 0.00 | 0.01 | 1.2 | 0.03 | 0.46% |

| NCZ003 | 501 | 504 | 3 | 0.64 | 0.04 | 0.14 | 1.5 | 0.08 | 0.69% |

| NCZ003 | 504 | 505 | 1 | 0.78 | 0.09 | 0.15 | 1.4 | 0.03 | 0.81% |

| NCZ003 | 505 | 506 | 1 | 0.08 | 0.00 | 0.01 | 0.5 | 0.01 | 0.08% |

| NCZ003 | 506 | 507 | 1 | 0.04 | 0.00 | 0.01 | 0.5 | 0.01 | 0.05% |

| NCZ003 | 507 | 508 | 1 | 0.00 | 0.00 | 0.01 | 0.5 | 0.01 | 0.01% |

| NCZ003 | 508 | 509 | 1 | 0.00 | 0.00 | 0.02 | 0.5 | 0.01 | 0.02% |

| NCZ003 | 509 | 510 | 1 | 0.00 | 0.00 | 0.01 | 0.5 | 0.01 | 0.01% |

| NCZ003 | 510 | 511 | 1 | 0.02 | 0.00 | 0.01 | 0.5 | 0.02 | 0.03% |

| NCZ003 | 511 | 512 | 1 | 0.19 | 0.00 | 0.05 | 0.5 | 0.01 | 0.20% |

| NCZ003 | 512 | 513 | 1 | 0.00 | 0.00 | 0.01 | 0.5 | 0.01 | 0.01% |

| NCZ003 | 513 | 514 | 1 | 0.00 | 0.00 | 0.01 | 0.5 | 0.01 | 0.01% |

| NCZ003 | 514 | 515 | 1 | 0.01 | 0.00 | 0.01 | 0.6 | 0.03 | 0.03% |

| NCZ003 | 515 | 516 | 1 | 0.07 | 0.00 | 0.01 | 0.5 | 0.01 | 0.08% |

| NCZ003 | 516 | 517 | 1 | 0.04 | 0.01 | 0.02 | 0.5 | 0.01 | 0.05% |

| NCZ003 | 517 | 518 | 1 | 0.83 | 0.00 | 0.01 | 0.8 | 0.01 | 0.78% |

| NCZ003 | 518 | 519 | 1 | 0.14 | 0.01 | 0.02 | 0.8 | 0.01 | 0.14% |

| NCZ003 | 519 | 520 | 1 | 0.15 | 0.00 | 0.02 | 0.5 | 0.01 | 0.15% |

| NCZ003 | 520 | 521 | 1 | 0.06 | 0.00 | 0.02 | 0.5 | 0.01 | 0.07% |

| NCZ003 | 521 | 522 | 1 | 0.10 | 0.00 | 0.02 | 0.5 | 0.01 | 0.11% |

| NCZ003 | 522 | 523 | 1 | 0.03 | 0.00 | 0.01 | 0.5 | 0.01 | 0.04% |

| NCZ003 | 523 | 524 | 1 | 0.25 | 0.00 | 0.02 | 0.5 | 0.01 | 0.24% |

| NCZ003 | 524 | 525 | 1 | 0.01 | 0.00 | 0.01 | 0.5 | 0.01 | 0.02% |

| NCZ003 | 525 | 526 | 1 | 0.21 | 0.00 | 0.01 | 0.5 | 0.01 | 0.20% |

| NCZ003 | 526 | 527 | 1 | 0.08 | 0.00 | 0.01 | 0.5 | 0.01 | 0.08% |

| NCZ003 | 527 | 528 | 1 | 0.00 | 0.00 | 0.01 | 0.5 | 0.01 | 0.01% |

| NCZ003 | 528 | 529 | 1 | 0.24 | 0.00 | 0.01 | 0.5 | 0.01 | 0.23% |

| NCZ003 | 529 | 531 | 2 | 1.15 | 0.01 | 0.19 | 1.2 | 0.01 | 1.13% |

| NCZ003 | 534 | 535 | 1 | 1.30 | 0.01 | 0.02 | 0.9 | 0.01 | 1.22% |

| Total | 148.90 | ||||||||

* Copper Equivalent (CuEq %) = Cu grade % * Cu Recovery + (Zn grade % * Zn Recovery * (Zn price $/t /Cu price $/t)) + (Pb grade % * Pb Recovery * (Pb price $/t /Cu price $/t)) + (Ag grade g/t / 31.103 * Ag recovery * (Ag price $/oz /Cu price $/t)) + (Au grade g/t / 31.103 * Au recovery * (Au price $/oz /Cu price $/t))

Cu Equivalent calculated using following commodity prices: Zn – US$3350/t, Cu – US$9523/t, Pb – US$2292/t, Ag – US$25.50/oz and

Au – US$1850/oz

Cu Equivalent calculated using following recovery assumptions for Northern Copper Zone: Zn – 82%, Cu – 93%, Pb – 78%, Ag – 72% and Au – 65%

Sample analysis and QA/QC

All samples generated from the drilling were dispatched to ALS Loughrea, Ireland.

Samples were assayed for multi-element data analysis using their ME-ICP61 package, which includes Ag, Cu, Pb and Zn. The samples were also assayed for gold using their Au-AA23 analysis package. Overlimit assays were then analysed using their Ag-OG62, Cu-OG62, Pb-OG62, Zn-OG62 and ME-OG62 analysis packages.

For QA/QC purposes, Anglesey Mining used the industry standard of inserting 5% Certified Reference Material (CRM) samples, 2.5% Certified Blank Samples (Blanks) and 5% duplicate samples at source. The CRMs were sourced from OREAS Australia.

Competent Person

The information in this announcement which relates to Drilling Results has been approved by Mrs. Liz de Klerk, M.Sc., Pr.Sci.Nat., FIMMM who is a professional registered with the South African Council for Natural Scientific Professionals (SACNASP: 400090/08) and independent consultant to the Company. Mrs. de Klerk is the Senior Geologist & Managing Director of Micon International Co Limited and has over 20 continuous years of exploration and mining experience in a variety of mineral deposit styles. Mrs. de Klerk has sufficient experience which is relevant to the style of exploration, mineralisation and type of deposit under consideration and to the activity which she is undertaking to qualify as a Competent Person as defined in the 2012 Edition of the “Australasian Code for reporting of Exploration Results, Exploration Targets, Mineral Resources and Ore Reserves” (JORC Code). Mrs. de Klerk consents to inclusion in the announcement of the matters based on this information in the form and context in which it appears.

About Anglesey Mining plc:

Anglesey is traded on the AIM market of the London Stock Exchange and currently has 420,093,017 ordinary shares in issue.

Anglesey is developing the 100% owned Parys Mountain Cu-Zn-Pb-Ag-Au VMS deposit in North Wales, UK with a reported resource of 5.3 million tonnes at over 4.0% combined base metals in the Measured and Indicated categories and 10.8 million tonnes at over 2.5% combined base metals in the Inferred category.

Anglesey also holds a 49.75% interest in the Grängesberg iron ore project in Sweden and 12% of Labrador Iron Mines Holdings Limited, which through its 52% owned subsidiaries, is engaged in the exploration and development of direct shipping iron ore deposits in Labrador and Quebec.

For further information, please contact:

Anglesey Mining plc

Rob Marsden, Chief Executive Officer – Tel: +44 (0)7531 475111

Andrew King, Interim-Chairman – Tel: +44 (0)7825 963700

Davy

Nominated Adviser & Joint Corporate Broker

Brian Garrahy / Daragh O’Reilly – Tel: +353 1 679 6363

WH Ireland

Joint Corporate Broker

Katy Mitchell / Harry Ansell – Tel: +44 (0)207 220 1666

Brand Communications

Public & Investor Relations

Alan Green – Tel: +44 (0)7976 431608

Quoted Micro 10 May 2024

AQUIS STOCK EXCHANGE

AQUIS STOCK EXCHANGE

Time to ACT is planning to join the Aquis Stock Exchange later this month and it has launched a fundraising ahead of the flotation. The flotation will take place even if there is no money raised. Time to ACT plans to develop a group of engineering-based energy transition businesses. Middlesborough-based Time to ACT has two subsidiaries. Diffusion Alloys is a long-established diffusion coating business. The technology provides an intermetallic layer that protects metal components at high temperatures. GreenSpur is a much newer business that is developing direct drive generator technology for use in wind power that does not require rare earths for magnets. The Winterflood Retail Access Platform is being used to raise up to £1m. The issue price and closing date have yet to be announced. Investors have to apply for shares via a broker. The minimum subscription is £100.

Cykel AI (CYK) has agreed a bid from standard listed Mustang Energy (MUST). The offer is 1.911 Mustang Energy shares for each Cykel AI share. Both companies’ shares have been suspended since 17 January. The Mustang Energy suspension price was 30.6p, but the bid is based on a much lower share price valuing the company, which has net liabilities, at £1m. That values the bid at 9.37p/share and Cykel AI is valued at £19.2m. Cykel AI is developing artificial intelligence products.

Newbury Racecourse (NYR) increased 2023 revenues by 9% to £19m and reported pre-tax profit improved from £130,000 to £720,000. However, there was a £700,000 exceptional gain relating to the release of a provision included. Cost increases reduced underlying profit. Raceday attendances fell from 141,000 to 130,000. The nursery has increased capacity by 18%. Shaun Hinds will become chief executive on 3 June.

Silverwood Brands (SLWD) executive director acquired 100,000 shares at 20p following the restoration of trading at the beginning of May. The share price recovered by 48.5% to 24.5p, but it is still not back to its suspension price.

Marula Mining (MARU) has appointed a new mine manager at the Larisoro manganese mine in Kenya. Bernard Kiprotich has five years of mining experience in Kenya. Marula Mining is investing in the established Larisoro manganese mining operation by securing a 60% commercial interest with an option to increase it to 70%. There are three shallow open pits. The purchase price is £300,000 satisfied by the issue of 2.4 million shares. Marula Mining will provide investment of $1.5m for equipment to enable production to be increased.

Essentially Group (ESSN) has completed the acquisition of Best Latin Foodstuff Trading for £1.945m in shares at 52.5p each. Catalina Onate, who founded the food importer, has been appointed as an executive director.

Shareholders passed resolutions at the AGM of Supernova Digital Assets (SOL), including a cancelation of the share premium account and authority to buy back shares.

TruSpine Technologies (LON: TSP) chief executive Laurence Strauss has resigned. He was appointed in April 2023.

RentGuarantor Holdings (RGG) raised £35,000 at 274p/share.

AIM

Metallurgical coal company Bens Creek (BEN) says a further court hearing related to the three US operations that are in Chapter 11 bankruptcy protection will be held on 6 June. The court has accepted the proposed Avanti debtor in possession financing and $2m has been drawn down. This provides enough cash until the end of May. The final terms of the facility are being negotiated.

Genedrive (GDR) has raised £2.1m in a placing at 1.5p. This follow’s yesterday evening’s announcement of a fundraising, where the point of care pharmacogenetic testing company wanted to raise £2.5m via a placing. There is also a REX retail offer for up to £3.5m, which closes on 17 May, and a one-for-one open offer that could raise up to £2.1m. If the total amount raised is not at least £6m the fundraising will not go ahead, so a further £3.9m is required. The company’s tests are being commercialised and a direct to consumer strategy pursued in the UK, while there will be distributors in other countries. There will also be investment to improve manufacturing efficiency and to fund regulatory approvals.

Plant Health Care (PHC) generated a 72% increase in revenues to $4.3m in the first four months of 2024. There is cash of $2.3m. The loss could be reduced from $3m to less than $1m this year. A profit is possible in 2025.

Third quarter driver management systems units produced by Seeing Machines (SEE) have gone into 313,662 vehicles, which is 51% higher than the previous quarter. This is more than treble the number in the same period two years and 80% higher than one year previously with more contracts set to contribute. Monitored connections of the Guardian fleet units were 5% higher on the quarter at 59,706.

Push-to-talk and workplace management technology developer Mobile Tornado (MBT) has won a contract through its regional partner to supply technology for a mobile network in the Middle East and Africa, which has more than 50 million customers. Management believes that there should be increasing sales momentum following the deal.

Healthcare services provider Totally (TLY) reassured the market with its latest trading statement. Full year EBITDA was £2.3m, down from £6.9m, and net debt was £800,000 at the end of March 2024. Revenues fell 22% to £106m because of the loss of a contract. Cost reductions and efficiency improvements have offset the tough market. Annualised cost savings of £3.5m are expected.

Bushveld Minerals (BMN) has agreed the conditional disposal of Vanchem to Southern Point Resources Fund 1 for up to $40.6m. The initial consideration is $20.6m. This requires shareholder approval. Southern Point Resources is increasing the interim working capital facility it is providing that is secured on production at Vanchem. This, and a $9m working capital facility, will be offset against the initial consideration and be used to pay creditors. This will leave a cash payment to Bushveld Minerals of $3.5m when the disposal happens. The deferred consideration is based on 25% of distributable free cash flow with a minimum of $1.25m paid for each quarter of the three-year period.

Mothercare (MTC) reported a 13% decline in global system sales last year due to poor trading in the Middle East. Destocking is a problem. There was better trading in the UK and Indonesia. The retailer will improve EBITDA, but Cavendish reduced its forecast EBIDA by 9% to £7m, compared to £6.7m in 2022-23. Refinancing talks continue and a conclusion should reduce the interest bill.

Battery technology developer Ilika (IKA) is raising up to £3.4m at 28p/share to spend on the Goliath solid-state battery. This cash should last at least 12 months. A placing and subscription raised £1.7m and a one-for-26 open offer could raise up to £1.7m more. The open offer closes on 28 May. There will be £750,000 earmarked for the development of the Goliath battery and this supplements the grant assistance obtained. A further £750,000 will be used to increase testing capacity to 0.75MWh/a and for upgrading dry room facilities. Additional cash raised will support further capital expenditure and working capital for Goliath and the Stereax miniature battery.

MAIN MARKET

Packaging manufacturer and distributor Macfarlane Group (MACF) disappointed with its AGM trading statement and lost the majority of the share price gain this year. Prices are falling, but this reflects lower costs, so margins are being maintained. First quarter sales were 9.5% lower, which does reflect a reduction in volumes. There should be improvement in the second half.

Oxford Cannabinoid Technologies (LON: OCTP) plans to cancel the standard listing. Management believes that stockmarket uncertainty is making it difficult to raise cash at an acceptable share price. The development of the drug pipeline will continue. The cancelation date is 6 June.

Andrew Hore

Alan Green covers Electric Guitar #ELEG, Thor Energy #THOR & Golden Metal Resources #GMET on this week’s Stockbox Research Talks

Alan Green covers Electric Guitar #ELEG, Thor Energy #THOR & Golden Metal Resources #GMET on this week’s Stockbox Research Talks

#SVML Sovereign Metals Ltd – Testwork Delivers Superior Quality Graphite

Graphite circuit feed prepared at Sovereign’s existing Lilongwe laboratory facility has produced high quality concentrates in benchtop and pilot-scale flotation and cleaning

Graphite circuit feed prepared at Sovereign’s existing Lilongwe laboratory facility has produced high quality concentrates in benchtop and pilot-scale flotation and cleaning

· Four independent laboratories all successfully produced high-grade graphite concentrate averaging over 97% Total Graphite Content (TGC) with flotation recoveries exceeding 90%

· Flotation results demonstrated 1.44% TGC run-of-mine Kasiya ore upgrades to more than 55% TGC rougher concentrate without crushing or milling, process steps typically required for producing graphite concentrates from hard-rock deposits; contributing to the unique low cost characteristics of Kasiya’s saprolite hosted graphite

· Graphite concentrates indicate exceptionally low levels of sulphur compared to typical hard-rock graphite peers – a key metric to qualify as active anode material for lithium-ion batteries

· Results are part of ongoing testwork being undertaken as part of the Company’s graphite marketing and active anode qualification strategy, supervised by Dr Surinder Ghag

· Downstream testwork to produce and characterise Coated Spherical Purified Graphite (CSPG) active anode material continues at German graphite consultancy ProGraphite GmbH

Sovereign Metals Limited (ASX:SVM; AIM:SVML) (the Company or Sovereign) is pleased to announce the results of graphite testwork completed at multiple independent laboratories in Australia, Canada and South Africa.

Graphite flotation and cleaning testwork was conducted on graphite circuit feed from Sovereign’s Kasiya Rutile-Graphite Project (Kasiya or Project) at four different laboratories, which all successfully produced high-grade graphite concentrate (94.9%-97.8% TGC) at high flotation recoveries (91.2%-97.2%).

The testwork demonstrated excellent results using a conventional flowsheet that was consistent across all laboratories, thus confirming Sovereign’s ability to produce a high quality graphite concentrate.

Managing Director Frank Eagar commented: “Our ability to upgrade Kasiya ore at 1.4% graphite to a 55% rougher concentrate without any crushing or milling, highlights more of the unique qualities of Kasiya. There are very limited other graphite projects with these characteristics. The pilot-scale results also confirm that Kasiya produces high-grade concentrates with very low sulphur levels at high recoveries. Simply put, Kasiya will be a standout producer of high-quality graphite concentrate at industry low operating costs.”

Classification 2.2: This announcement includes Inside Information

ENQUIRIES

|

Frank Eagar (South Africa/Malawi) +61(8) 9322 6322 |

Sam Cordin (Perth) |

Sapan Ghai (London)

|

|

Nominated Adviser on AIM and Joint Broker |

|

|

SP Angel Corporate Finance LLP |

+44 20 3470 0470 |

|

Ewan Leggat Charlie Bouverat |

|

|

|

|

|

Joint Brokers |

|

|

Stifel |

+44 20 7710 7600 |

|

Varun Talwar |

|

|

Ashton Clanfield |

|

|

|

|

|

Berenberg |

+44 20 3207 7800 |

|

Matthew Armitt |

|

|

Jennifer Lee |

|

|

|

|

|

Buchanan |

+ 44 20 7466 5000 |

The graphite circuit feed provided to the various laboratories was produced at the Company’s existing laboratory facility in Lilongwe, Malawi, where it was screened and separated over a wet shaking table.

Figure 1: Holman Wilfley 2000 wet shaking table in action demonstrating clear separation between Rutile HM, waste and Graphite

The graphite feed grades of 3.5%-4.0% TGC to the graphite circuit are significantly higher than the Mineral Resource Grade of 1.44%, highlighting the ~2.4-2.8-fold upgrading of graphite grades when ROM ore passes through the front-end rutile gravity separation circuit.

This demonstrates the ease of separating the rutile heavy mineral and graphite streams from the front end of the Kasiya Pre-feasibility Study process flowsheet. Subsequently, the two product streams pass into distinct, industry-standard, final product flowsheets. This further highlights the commercial benefits of having both rutile and graphite mineralisation co-existent in the same soft saprolite-hosted orebody.

The first stage of upgrading the graphite feed, rougher flotation, achieved very high rejection (>90%) of waste materials to rougher tails, producing a rougher concentrate with more than 55% TGC and very high recoveries (94%-98%) in laboratory scale testing consistently across all four laboratories. Upgrading the graphite feed at very high recoveries and rejection of non-graphitic minerals without run-of-mine milling is another of Kasiya’s significant advantages, supporting the lowest cost graphite production.

The rougher concentrate was further upgraded through laboratory scale flotation, cleaning and polishing stages, producing high-grade concentrates at high graphite circuit recoveries.

Figure 2: High-level process flowsheet for rutile and graphite production at Kasiya

Pilot-scale testwork confirmed the laboratory-scale results with >90% TGC recovery to high-grade graphite concentrates (<180-micron concentrate at 96.9% TGC and >180-micron concentrate at 97.2% TGC).

Figure 3: Graphite flotation test work at Australia-based ALS Global

HIGHLY FAVOURABLE IMPURITY PROFILE

Kasiya concentrates have very low levels of sulphur. Sulphur can be difficult to remove in the purification processes required to produce anode materials. Other major impurities important for anode material purification processes are iron (Fe), silicon (Si) and aluminium (Al). The Kasiya material has exceptionally low levels of all of these impurities. Benchmarked against the Chinese Standard (China dominates the supply of graphite for battery anodes) this could potentially lead to significant commercial advantages during purification and Kasiya’s potential as a long term secure source of graphite ex-China.

|

|

Kasiya |

Benchmarks |

|||

|

|

Concentrate |

Concentrate |

Combined |

China |

Example Chinese Product 2 |

|

Graphite (TGC%) |

96.9% |

97.2% |

97.0% |

>94% |

96.0% |

|

Sulphur (S) (%) |

<0.02% |

<0.02% |

<0.02% |

<0.5% |

0.23% |

|

Iron (Fe) (%) |

0.48% |

0.46% |

0.47% |

<1.00% |

0.55% |

|

Silicon (Si) (%) |

0.60% |

0.80% |

0.68% |

n/d |

1.25% |

|

Aluminium (Al) (%) |

0.24% |

0.28% |

0.26% |

n/d |

0.38% |

1. National Standard of China – Flake Graphite (GB/T 3518-2023)

2. Asbury Carbons – A Study Comparing the Performance of Natural Flake Graphite from Two Different Geographical Regions (https://asbury.com/media/1170/a-study-comparing-the-performance-of-natural-flake-graphite.pdf)

CONTINUING DOWNSTREAM TEST WORK

Kasiya concentrate has been sent for downstream testwork at respected graphite consultancy ProGraphite to produce and characterise CSPG active anode material for lithium-ion batteries. ProGraphite is conducting shaping, purification, and coating testwork to produce CSPG and evaluate the electrochemical performance of Kasiya CSPG. This will provide baseline data for further optimisation and engagement with off-takers. Initial outcomes of this test work are expected to be released in the coming weeks.

Competent Person Statement

The information in this report that relates to Metallurgical Testwork is based on information compiled by Dr Surinder Ghag, PhD., B. Eng, MBA, M.Sc., who is a Member of the Australasian Institute of Mining and Metallurgy (MAusIMM). Dr Ghag is engaged as a consultant by Sovereign Metals Limited. Dr Ghag has sufficient experience, which is relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking, to qualify as a Competent Person as defined in the 2012 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Dr Ghag consents to the inclusion in the report of the matters based on his information in the form and context in which it appears.

The information in this report that relates to Exploration Results is based on information compiled by Mr Samuel Moyle, a Competent Person who is a member of The Australasian Institute of Mining and Metallurgy (AusIMM). Mr Moyle is the Exploration Manager of Sovereign Metals Limited and a holder of ordinary shares and unlisted performance rights in Sovereign Metals Limited. Mr Moyle has sufficient experience that is relevant to the style of mineralisation and type of deposit under consideration and to the activity being undertaken, to qualify as a Competent Person as defined in the 2012 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves’. Mr Moyle consents to the inclusion in the report of the matters based on his information in the form and context in which it appears.

The information in this announcement that relates to the Mineral Resource Estimate is extracted from an announcement dated 5 April 2023 entitled ‘Kasiya Indicated Resource Increased by over 80%’ which is available to view at www.sovereignmetals.com.au and is based on, and fairly represents information compiled by Mr Richard Stockwell, a Competent Person, who is a fellow of the Australian Institute of Geoscientists (AIG). Mr Stockwell is a principal of Placer Consulting Pty Ltd, an independent consulting company. The original announcement is available to view on www.sovereignmetals.com.au. Sovereign confirms that a) it is not aware of any new information or data that materially affects the information included in the original announcement; b) all material assumptions included in the original announcement continue to apply and have not materially changed; and c) the form and context in which the relevant Competent Persons’ findings are presented in this announcement have not been materially changed from the original announcement.

The information in this announcement that relates to Production Targets, Ore Reserves, Processing, Infrastructure and Capital Operating Costs, Metallurgy (rutile and graphite) is extracted from an announcement dated 28 September 2023 entitled ‘Kasiya Pre-Feasibility Study Results’ which is available to view at www.sovereignmetals.com.au. Sovereign confirms that: a) it is not aware of any new information or data that materially affects the information included in the original announcement; b) all material assumptions and technical parameters underpinning the Production Target, and related forecast financial information derived from the Production Target included in the original announcement continue to apply and have not materially changed; and c) the form and context in which the relevant Competent Persons’ findings are presented in this presentation have not been materially modified from the original announcement.

|

Ore Reserve for the Kasiya Deposit |

|

||||||

|

Classification |

Tonnes |

Rutile Grade |

Contained Rutile |

Graphite Grade (TGC) (%) |

Contained Graphite |

RutEq. Grade* |

|

|

Proved |

– |

– |

– |

– |

– |

– |

|

|

Probable |

538 |

1.03% |

5.5 |

1.66% |

8.9 |

2.00% |

|

|

Total |

538 |

1.03% |

5.5 |

1.66% |

8.9 |

2.00% |

|

* RutEq. Formula: Rutile Grade x Recovery (100%) x Rutile Price (US$1,484/t) + Graphite Grade x Recovery (67.5%) x Graphite Price (US$1,290/t) / Rutile Price (US$1,484/t). All assumptions are taken from the PFS ** Any minor summation inconsistencies are due to rounding

|

Kasiya Total Indicated + Inferred Mineral Resource Estimate at 0.7% rutile cut-off grade |

|||||

|

Classification |

Resource |

Rutile Grade |

Contained Rutile |

Graphite Grade (TGC) (%) |

Contained Graphite |

|

Indicated |

1,200 |

1.0% |

12.2 |

1.5% |

18.0 |

|

Inferred |

609 |

0.9% |

5.7 |

1.1% |

6.5 |

|

Total |

1,809 |

1.0% |

17.9 |

1.4% |

24.4 |

Forward Looking Statement

This release may include forward-looking statements, which may be identified by words such as “expects”, “anticipates”, “believes”, “projects”, “plans”, and similar expressions. These forward-looking statements are based on Sovereign’s expectations and beliefs concerning future events. Forward looking statements are necessarily subject to risks, uncertainties and other factors, many of which are outside the control of Sovereign, which could cause actual results to differ materially from such statements. There can be no assurance that forward-looking statements will prove to be correct. Sovereign makes no undertaking to subsequently update or revise the forward-looking statements made in this release, to reflect the circumstances or events after the date of that release.

The information contained within this announcement is deemed by the Company to constitute inside information as stipulated under the Market Abuse Regulations (EU) No. 596/2014 as it forms part of UK domestic law by virtue of the European Union (Withdrawal) Act 2018 (‘MAR’). Upon the publication of this announcement via Regulatory Information Service (‘RIS’), this inside information is now considered to be in the public domain.

Sharepickers – Alan Green discusses Crimson Tide #TIDE, Warpaint #W7L, Electric Guitar #ELEG & Silver Bullet Data #SBDS

Sharepickers – Alan Green discusses Crimson Tide #TIDE, Warpaint #W7L, Electric Guitar #ELEG & Silver Bullet Data #SBDS with Justin Waite

Cadence Minerals #KDNC – Corporate Update – Evergreen Lithium (ASX: EG1) Fully Permitted to Commence Exploration at Bynoe

Cadence Minerals (AIM: KDNC; OTC: KDNCY) is pleased to note that ASX listed Evergreen Lithium Limited (“Evergreen”) (ASX: EG1) has announced the approval of its Mine Management Plan (MMP), enabling EverGreen to commence high impact exploration activities such as auger sampling and drilling at its flagship Bynoe project.

Cadence Minerals (AIM: KDNC; OTC: KDNCY) is pleased to note that ASX listed Evergreen Lithium Limited (“Evergreen”) (ASX: EG1) has announced the approval of its Mine Management Plan (MMP), enabling EverGreen to commence high impact exploration activities such as auger sampling and drilling at its flagship Bynoe project.

Geochemical, geophysical and mapping activities completed to date demonstrate the potential for lithium bearing LCT pegmatite style mineralisation within EverGreen’s EL 31774 lease, spanning 231 square Kilometers of tenure.

Highlights:

- EverGreen has received approval for its Mine Management Plan (MMP) which will allow for drilling and other higher impact activities to commence at its Bynoe Project. These activities include auger sampling, AC/RAB, RC and diamond drilling.

- Aboriginal Areas Protection Authority certificate (AAPA) has already been received in December 2023.

- The Bynoe project is now fully permitted to commence exploration.

- Auger sampling and drilling contractors have been secured and work is scheduled

- to commence when field conditions are suitable.

- Planned work programs for 2024 will include auger, RAB/AC and RC drilling testing of geochemical and geophysical anomalies, with potential follow-up diamond drilling.

Link here to view the full Evergreen ASX announcement

Evergreen Exploration Manager Andrew Harwood commented: “With all Bynoe exploration and drilling approvals now received and field conditions improving, it is expected that field activities will commence in the coming weeks. The Company looks forward to drilling on its 231Km2 lease at Bynoe, one of the largest land holdings in the Bynoe Pegmatite Field. The Company believes that its Bynoe Lithium Project hosts excellent and compelling drill-ready targets”.

Background to Cadence’s investment in Evergreen Lithium

Cadence Minerals received approximately 15.8 million shares in Evergreen in July 2022 when Cadence sold its 31.5% stake in Lithium Technologies and Lithium Supplies (“LT and LS”) to Evergreen as announced on 27 June 2022. A further AS$ 3.47 million (£1.86 million) of shares in Evergreen are due to Cadence on the achievement of certain performance milestones by Evergreen. The pricing of Evergreen shares associated with this consideration is based on a defined pricing mechanism linked to the VWAP and the date at which the performance milestones are achieved. Further details of these milestones can be found in the Evergreen prospectus available here . Cadence’s shares are subject to a 2-year escrow agreement as determined by the listing rules of the ASX.

|

For further information contact:

|

|

| Cadence Minerals plc | +44 (0) 20 3582 6636 |

| Andrew Suckling | |

| Kiran Morzaria | |

| WH Ireland Limited (NOMAD & Broker) | +44 (0) 20 7220 1666 |

| James Joyce | |

| Darshan Patel | |

| Fortified Securities – Joint Broker | +44 (0) 20 3411 7773 |

| Guy Wheatley | |

| Brand Communications | +44 (0) 7976 431608 |

| Public & Investor Relations | |

| Alan Green |

ECR Minerals #ECR – Victoria Projects Update – Significant increase in gold grades from Bulk Sampling at Creswick

ECR Minerals plc (LON: ECR), the exploration and development company focused on gold in Australia, is pleased to provide an update on the bulk sample results for the first four reverse circulation drill holes as well as the final two holes drilled at the Kuboid Hill prospect in Creswick earlier this year. The Company is also pleased to provide results from stream sampling that was carried out last month at its Bailieston Project.

HIGHLIGHTS

Creswick

- Reportable bulk sampling results of 05g/t Au and 2.53 g/t Au over 1 metre upgraded from 0.76 and 0.37 g/t Au respectively.

- Techniques employed give potential scope for a marked improvement in grades for the remaining “best hole” bulk samples from pan concentrate.

Bailieston

- Best results of 798 ppb Au and 712 ppb Au from stream sampling.

- Sampling was carried out at three areas with no known historical workings and have shown encouraging surface expression of anomalous gold which gives merit to further follow up

- Now re-analysing a number of drill cores from HR3 at Bailieston for the presence of Antimony, which correlates with this latest reconnaissance work showing a presence of Antimony.

- ECR is funded for its planned activities in Victoria and Queensland in 2024.

Details of the Programmes

Creswick

As announced on 8 April 2024, a total of 1,032 metres of reverse circulation (“RC”) drilling was completed at Kuboid Hill on 16 February 2024. This was the second part of an extended reverse circulation drilling programme at Creswick, following on from 522 metres completed at Davey Road where, as previously announced on 12 February 2024, ECR reported a best overall grade gold of 41.03g/t Au. The Kuboid Hill programme was designed to follow up on the Company’s anomalous gold soil sampling campaign that was completed in 2022.

ECR has received final results from bulk sampling for the first four of the 17 RC drill holes at Kuboid Hill (being KHRC012, KHRC008, KHRC009 and KHRC015). Only KHRC012 generated any reportable results from the bulk sampling, significant improvement was seen in three of the samples from that hole, as set out below:

Details of bulk sampling and significant intercepts > 0.5g/t

| HOLE | From (m) | To (m) | Interval (m) | Original Au g/t | Bulk Au g/t |

| KHRC012 | 27 | 28 | 1 | 0.76 | 3.05 |

| KHRC012 | 28 | 29 | 1 | 0.26 | 0.81 |

| KHRC012 | 40 | 41 | 1 | 0.37 | 2.53 |

The bulk samples from the remaining drillholes are currently in the laboratory. Based on the improved results for hole KHRC012, the ECR Board considers that there is a reasonable expectation of an improvement in grades for some of the remaining bulk samples from other mineralised zones.

Additional Kuboid Hill Drill Holes

The remaining samples for the final two drill holes at Kuboid Hill (see announcement 8 April 2024) have revealedfurther mineralised zones, consistent with what has been seen previously, although neither reported intercepts above 1 g/t.

Bailieston

At the Company’s Bailieston Project, a stream sampling campaign was recently completed throughout the northern part of the tenements (EL006911, EL006912 and EL007296) with the campaign being designed to test for initial evidence of gold mineralisation within the unexplored part of the region.

All three areas have had no historical work and, based on the results obtained, the Company believes there is merit in undertaking additional near-term follow up exploration.

- Black Cat South

Best results of 798 ppb Au and 712 ppb Au from two streams on the western flank of the Black Cat Fault. The two streams drain a prominent ridgeline that is approximately 400m long in strike and offers further prospectivity. The regional Black Cat Fault is associated with other gold and antimony historical mining activity along strike.

- King’s Cross

Result of 150 ppb Au from a stream that drains an old prospect known as King’s Cross. Highly oxidised quartz veins are present in this area and require follow up testing.

- Freisland Hills

An anomaly of 100ppb Au was obtained from an unnamed creek in the centre of the area.

In all three prospects, LIDAR mapping shows there has been no previous mining activity or prospecting in the area which provides for an opportunity for development and deeper exploration.

In addition to stream sampling, two small soil orientation surveys were completed on the north fringes of the HR3 goldfield area and the Cherry Tree South goldfield. Both soil surveys show coincidental elevated arsenic and antimony. Previous soil sampling at HR3 has identified arsenic and antimony as pathfinders to gold mineralisation.

ECR is now also re-analysing the core from its earlier drilling at the HR3 prospect at Bailieston for antimony. The Costerfield-Bailieston-Nagambie district is noted for economic veins of antimony and elevated antimony has been observed from previous pXRF analysis of the drill core.

Mike Whitlow Chief Operating Officer said: “Today’s news points to further potential value at our Creswick gold assets and we’re looking forward to the results from the remaining bulk samples from our “best holes” following onfrom our ‘off the rig’ sample results, which include observations of visible gold.”

Adam Jones Chief Geologist said: “Results from the Bailieston stream sampling survey are also encouraging and we firmly believe ground exploration above these streams is now merited. The Bailieston field is prospective for not only gold, but also for antimony, and we’re fortunate to be located between the two proven fields of Costerfield and Nagambie. Today’s results give further validation to our rationale to re-analyse our historical core from HR3 and Cherry Tree.”

REVIEW OF ANNOUNCEMENT BY QUALIFIED PERSON

This announcement has been reviewed by Adam Jones, Chief Geologist at ECR Minerals plc. Adam Jones is a professional geologist and is a Member of the Australian Institute of Geoscientists (MAIG). He is a qualified person as that term is defined by the AIM Note for Mining, Oil and Gas Companies.

FOR FURTHER INFORMATION, PLEASE CONTACT:

| ECR Minerals plc | Tel: +44 (0) 1738 317 693 | ||

| Nick Tulloch, Chairman

Andrew Scott, Director |

|||

| Email: | |||

| Website: www.ecrminerals.com | |||

| WH Ireland Ltd | Tel: +44 (0) 207 220 1666 | ||

| Nominated Adviser

Katy Mitchell / Andrew de Andrade |

|||

| Axis Capital Markets Limited | Tel: +44 (0) 203 026 0320 | ||

| Broker | |||

| Ben Tadd/Lewis Jones | |||

| SI Capital Ltd | Tel: +44 (0) 1483 413500 | ||

| Broker | |||

| Nick Emerson | |||

| Novum Securities Limited | Tel: +44 (0) 20 7399 9425 | ||

| Broker

Jon Belliss |

|||

| Brand Communications | Tel: +44 (0) 7976 431608 | ||

| Public & Investor Relations | |||

| Alan Green | |||

Glossary

| Au | Gold |

| ppb | parts per billion |

| pXRF | Portable x-ray fluorescence (analyser) |

ABOUT ECR MINERALS PLC

ECR Minerals is a mineral exploration and development company. ECR’s wholly owned Australian subsidiary Mercator Gold Australia Pty Ltd (“MGA”) has 100% ownership of the Bailieston and Creswick gold projects in central Victoria, Australia, has six licence applications outstanding which includes one licence application lodged in eastern Victoria (Tambo gold project).

ECR also owns 100% of an Australian subsidiary LUX Exploration Pty Ltd (“LUX”) which has three approved exploration permits covering 946 km2 over a relatively unexplored area in Lolworth Range, Queensland, Australia. The Company has also submitted a license application at Kondaparinga which is approximately 120km2 in area and located within the Hodgkinson Gold Province, 80km NW of Mareeba, North Queensland.

Following the sale of the Avoca, Moormbool and Timor gold projects in Victoria, Australia to Fosterville South Exploration Ltd (TSX-V: FSX) and the subsequent spin-out of the Avoca and Timor projects to Leviathan Gold Ltd (TSX-V: LVX), MGA has the right to receive up to A$2 million in payments subject to future resource estimation or production from projects sold to Fosterville South Exploration Limited. MGA also has approximately A$75 million of unutilised tax losses incurred during previous operations.

ECR holds a royalty on the SLM gold project in La Rioja Province, Argentina which could potentially receive up to US$2.7 million in aggregate across all licences

Alan Green covers Altona Rare Earths #REE, Coinsilium #COIN & Facilities by ADF #ADF on this week’s Stockbox Research Talks

Alan Green covers Altona Rare Earths #REE, Coinsilium #COIN & Facilities by ADF #ADF on this week’s Stockbox Research Talks

Quoted Micro 6 May 2024

AQUIS STOCK EXCHANGE

Good Life Plus (GDLF) has traded strongly since joining Aquis and raising cash for marketing. The luxury prize draw company increased the number of subscribers from 21,000 at the end of 2023 to 30,000. Churn has been reduced.

Invinity Energy Systems (IES) raised £56m at 23p/share with £25m committed by the UK Infrastructure Bank and £3m from Korean Investment Partners. There is also an open offer to raise up to £6.6m. The share price slipped 6.12% to 23p. IES will use £30m to increase capacity ahead of the launch of the latest version of the Mistral flow battery.

KR1 (KR1) gained shareholder approval for the market acquisition of up to 14.99% of its shares. NAV was 132.05p/share at the end of March 2024, down from 134.6p/share one month earlier. There was £1.96m in income from digital assets during the month.

Apollon Formularies (APOL) has sent a general meeting notice for 28 May to gain approval of the cancelation of the Aquis quotation. The company is selling its IP to a Canadian company.

Rogue Baron (SHNJ) has acquired Eight Vodka for £70,000 in shares at 0.5p each. Eight Vodka is distilled eight times in Ecuador.

Trading in Silverwood Brands (SLWD) was restored following the completion of a capital reduction. Phoenix Asset Management increased its stake from 0.94% to 29.9%. In the first quarter a rebranding of Balmonds has disrupted sales. The costs of acquiring Cosme Science hit profitability of Sonotas.

One Health Group (OHGR) says it did better than expected last year with annual revenues improving from £20.5m to £23m. Net cash was £4.7m at the end of March 2024. There was a 13% increase in NHS patient referrals for treatments. New five-year contracts have been secured with the two largest customers.

RentGuarantor Holdings (RGG) says first quarter revenues were 62% ahead and the number of tenant contracts was 38% higher.

Investment company MaxRets Ventures (MAX) reported net assets of £19,000 at the end of October 2023, down from £497,000. There was no new investment during the year. A transformative acquisition is being sought.

Hydrogen Future Industries (HFI) more than halved the interim cash outflow from operating activities to £234,000. Ther was £263,000 in the bank at the end of January 2024, but £612,000 has been raised since then. Testing of the prototype wind turbine and the electrolyser has gone well.

Substrate AI (SAI) generated revenues of $8.6m in 2023. There was $4.42m in the bank.

Hacienda Management has taken a 7.48% stake in Supernova Digital Assets (SOL). Pete Mills increased his stake in Oscillate (MUSH) from 3.02% to 4.03%. DXS International (DXSP) chairman Robert Sutcliffe bought 100,000 shares at 1.46p/share.

AIM

Trinity Exploration & Production (TRIN) has agreed a bid from fellow AIM-quoted Trinidad oil and gas company Touchstone Exploration (TXP), which is offering 1.5 shares for every Trinity share. The Trinity shareholders will own one-fifth of the enlarged company. The combined group will be in a stronger position to make investments in new production. The Touchstone Exploration share price is 4.85% lower at 39.25p, valuing each Trinity share at 58.875p – the share price is 50% higher at 54p.

Alpha Financial Markets Consulting (AFM) has confirmed that BridgePoint Advisers has made a bid approach and Cinven is considering making a bid. Revolution Bars Group (RBG) has received interest from Nightcap (NGHT), which is assessing the situation and options include a bid or acquisition of some sites or subsidiaries.

Electric Guitar (ELEG) moved from the standard list to AIM following the reverse takeover of 3radical on 3 May. It is the first in a planned series of acquisitions in the digital marketing sector, where regulatory and market changes, such as the blocking of third-party cookies, provide significant growth opportunities. 3radical was acquired for 61.2 million shares valued at £1.28m. A fundraising generated £1.32m at 2.1p/share and that valued the company at £4.7m. 3radical was set up by the founders of campaign management software provider Alterian at the end of 2011 The shares had been suspended at 2.1p and they fell to 1.8p when trading recommenced on AIM.

Multi-channel retailer TheWorks.co.uk (WRKS) moved from a premium listing to AIM. The board felt the company was too small for the cost and regulatory burden of the Main Market. One of the attractions of AIM is that the company will no longer be classified as a Public Interest Entity and it will be able to choose an auditor from a wider range of firms. Singer forecasts a slump in pre-tax profit from £10.1m to £1m in the year to April 2024.

Cornish Metals (CUSN) has published a preliminary economic assessment of the South Crofty tin project in Cornwall. There is an after-tax NPV8 of $201m at a tin price of $31,000 /tonne. Pre-production capital requirement is $177m, which is higher than previous estimates, and there should be 14-year mine life. Life of mine all in sustaining cost is estimated at $13,661/tonne. Planned first production is in 2027.

Horizonte Minerals (HZM) has enough cash until 17 May and senior lenders have agreed to extend waivers on loans, including deferring interest payments, until 15 May. These lenders have security over the company’s assets. Horizonte Minerals has guaranteed the debt of the subsidiary that owns the Araguaia project. Discussions with creditors and investors continue in an attempt to achieve some recovery value for creditors. That may include the disposal of the Araguaia project. None of the proposals are likely to recover value for shareholders.

Arrow Exploration (AXL) grew average production from 1.3mboe/day in 2022 to 2.2mboe/day in 2023 and revenues increased from $28.1m to $50.6m, which was slightly lower than forecast. There was cash of $13m at the end of 2023 and this fell to $12m at the end of March 2024. Production has reached 2.9mboe/day in March, while drilling activity will lead to further increases in the medium-term. Canaccord Genuity has cut its 2024 revenues forecast from $103.9m to $98.6m and net cash is expected to be $17m at the end of 2024.

Trading at property services provider Kinovo (KINO) is ahead of expectations with organic growth of 23% in the year to March 2024. Underlying pre-tax profit should be more than £6m, excluding costs related to the DCB contracts, which were guaranteed by Kinovo when it was sold, still to be completed.

Mark Halpin has stepped down as chief executive of managed IT services provider CloudCoCo (CLCO) and MXC Guernsey, which holds a 10.6% stake, has extended its loan notes to 31 August 2026 in return for a £550,000 fee. The amount outstanding on the loan notes is £5.85m. MXC can also appoint an executive director and Ian Smith becomes interim chief executive. The shares returned from suspension following the release of figures for the year to September 2023 showing revenues 7% ahead at £26m. The loss was flat at £2.6m. There was a cash inflow from operating activities. Net debt was £6.3m at the end of September 2023.

Brake discs developer Surface Transforms (SCE) raised £6.5m fundraising at 1p/share. There will be a one-for 1.76036319 open offer at the same price. That could raise £2m. The cash will finance the scale up of manufacturing. Factory capacity will be increased to £75m. This year’s revenues are forecast to be £17.5m.

Gift wrap and stationery supplier IG Design (IGR) did better than expected in the year to March 2024 with margins recovering and pre-tax profit improving from $9.2m to $25.9m, compared with a forecast of $20.5m, even though revenues fell. Net cash nearly doubled to $95m. It appears the recovery is gathering pace. Management believes that margins could return to previous levels this year and an operating margin of more than 6% in 2026-27, suggesting a pre-tax profit of around $50m.

IT distributor Northamber (NAR) is acquiring Tempura Technology and Tempura Communications, which distribute unified communications products, for £6.02m in cash and 181,818 shares. There is £2.64m of the cash consideration contingent on EBITDA in the years ending June 2025, 2026 and 2027. This is a profitable business that has been growing organically.

Heavy mineral sands project developer Kazera Global (KZG) says recent changes at the National Nuclear Regulator in South Africa mean that it will have to provide additional information on how it will meet financial obligations. This should be funded by cash flow. A response is expected shortly and that will allow heavy mineral sands production to start in Alexander Bay, South Africa.

Oil and gas producer Jadestone Energy (JSE) reported a $91.3m loss for 2023 due to asset impairments, lower oil prices and higher interest costs. Capital investment has increased net debt to $110.5m by the end of March 2024. Average production in the first quarter of 2024 was 17,200 boe/day, which was hit by the Australian cyclone season. Production guidance for 2024 is 20,000-22,000 boe/day.

MAIN MARKET

Castings (CGS) did better than expected in the year to March 2024 and Canaccord Genuity upgraded its pre-tax profit forecast from £27.1m to £28.2m. Margins improved in the second half. Net cash is £32m.

Cybersecurity firm Narf Industries (NARF) is accelerating work on capabilities uniquely effective in battling a new generation threat. Developed was funded through a $2.3m contract from DARPA.

Andrew Hore