Home » Posts tagged 'indirect'

Tag Archives: indirect

#SVML Sovereign Metals LTD – Kasiya Definitive Feasibility Study Results

OUTSTANDING FINANCIAL RETURNS

Steady State annual EBITDA US$476M and Free Cash Flow (pre-tax, unlevered) US$452M

Total revenue of US$16.2Bn over 25-year initial mine life, with potential for mine life extensions

Pre-tax NPV₈ of US$2.2 billion

NPV/Capex ratio of 3.0x – capital expenditure to first production of US$727 million

Operating cost of just US$450/t product (FOB Nacala) – underpinning strong margin resilience across commodity cycles

GLOBAL LEADER ACROSS TWO CRITICAL MINERALS SUPPLY CHAINS

Positioned to become the world’s largest producer of both natural rutile (222ktpa) and natural flake graphite (275ktpa)

Lowest-cost graphite producer globally at or beyond pre-feasibility stage – including China

Titanium and graphite both designated as Critical Minerals by the United States and the European Union, highlighting their strategic importance to Western supply chains

Free-dig orebody requiring no pre-strip, drilling or blasting with a simple low-energy processing flowsheet

Established export infrastructure: hydropower grid, heavy-haul rail, port at Nacala

BANKABLE DEVELOPMENT PATHWAY

DFS completed under the oversight of the Sovereign-Rio Tinto Technical Committee

Data obtained from Pilot Mining Program, completed with technical input from Rio Tinto, provided real-world inputs across key DFS workstreams

DFS incorporates environmental and social workstreams aligned with IFC performance standards; World Bank/IFC Collaboration Agreement in place as potential co-lead mandated lead arranger for project financing

Non-binding offtake MOUs covering over 50% of Stage 1 rutile production (Mitsui) and over 35% of coarse flake graphite sales (Traxys)

HEAVY RARE EARTH POTENTIAL NOT INCLUDED IN DFS – EVALUATION UNDERWAY

Monazite concentrate recovered from rutile processing circuit with exceptionally elevated levels of heavy rare earths Dysprosium, Terbium and Yttrium

Potential third revenue stream at minimal incremental cost – all three elements subject to Chinese export restrictions

Dedicated monazite evaluation program now underway to assess scale, recovery and economic potential

Sovereign Metals Limited (ASX:SVM; AIM:SVML; OTCQX:SVMLF) (Sovereign or the Company) is delighted to announce the results of the Definitive Feasibility Study (DFS or the Study) for its Kasiya Rutile-Graphite Project (Kasiya or the Project) in Malawi. The DFS builds on the outcomes of the Optimised Pre-feasibility Study (OPFS) and on empirical data from the Pilot Mining and Rehabilitation Program (Pilot Mining). The DFS was undertaken in accordance with a scope of work approved by, and with technical input and oversight from, the Sovereign-Rio Tinto Technical Committee and, where applicable, conforms to the World Bank Group’s International Finance Corporation (IFC) Performance Standards to enhance bankability of the Project.

Managing Director and CEO Frank Eagar commented:

“The completion of this DFS marks a defining milestone for Kasiya and for the global titanium and graphite supply chains. To deliver a DFS of this quality, depth and confidence, rarely achieved by a pre-production company, reflects the calibre of partnerships that Sovereign has assembled around this project: Rio Tinto’s technical expertise, alignment with IFC Performance Standards under our Collaboration Agreement, and offtake interest driven by U.S. and Japanese supply chain security priorities. The successful completion of large-scale field trials, combined with the expertise of our experienced owner’s team and the technical support provided by Rio Tinto, reinforces Kasiya’s potential to be a long-life, low-cost, and reliable source of two critical and globally strategic minerals. Kasiya is not simply a mining project – it is a globally strategic asset.“

TABLE 1: Key DFS Metrics (Steady State)

|

OPERATING METRICS |

Units |

Results |

|

Initial Life of Mine (LOM) |

Yrs |

25 |

|

Total Ore Mined |

Mt |

536 |

|

Phase 1 Plant Throughput (Yrs 1-4) |

Mtpa |

12 |

|

Phase 2 Plant Throughput (Yrs 5-25) |

Mtpa |

24 |

|

Annual Rutile Production (95%+ TiO2) |

ktpa |

222 |

|

Annual Graphite Production (96% TGC) |

ktpa |

275 |

|

FINANCIAL PERFORMANCE |

||

|

Total Revenue |

US$M |

16,210 |

|

Annual Revenue |

US$M |

728 |

|

Annual EBITDA |

US$M |

476 |

|

Annual Free Cash Flow (pre-tax, unlevered) |

US$M |

452 |

|

NPV8 (real, pre-tax) |

US$M |

2,204 |

|

IRR (pre-tax) |

% |

23% |

|

OPERATING AND CAPITAL EXPENDITURE |

||

|

Capex to First Production |

US$M |

727 |

|

Total LOM Development Capex |

US$M |

1,239 |

|

Total LOM Sustaining Capex |

US$M |

431 |

|

Operating Costs (FOB Nacala) |

US$/t product |

450 |

Note: Steady State is defined as years of operation during which total run-of-mine is at full capacity of 24 Mtpa (i.e., years 5 to 23). All results are presented on a 100% project basis.

DFS CONFIRMS SOVEREIGN TO REDEFINE TITANIUM METAL AND GRAPHITE SUPPLY CHAINS

Kasiya, located in central Malawi, hosts the world’s largest natural rutile deposit and the second-largest flake graphite deposit. Both titanium and graphite are officially classified as Critical Minerals by the United States and the European Union. At steady-state, Kasiya is forecast to deliver approximately 222 kt of rutile and 275 kt of graphite annually – positioning Sovereign as potentially the world’s largest producer of both natural rutile and natural flake graphite.

Natural Rutile – Addressing Titanium Supply Chain Vulnerability

Natural rutile is the purest and highest-grade form of naturally occurring titanium feedstock, with titanium dioxide (TiO₂) content typically exceeding 95%. It is the preferred feedstock for titanium sponge production and high-specification titanium alloy applications in aerospace, defence and medical industries.

According to the United States Geological Survey (USGS), the United States currently produces zero titanium sponge domestically and is 100% import-reliant, with record imports of 44,000 tonnes in 2025. Japan supplies over 70% of the US’s titanium sponge imports, and Japanese producers themselves depend on securing reliable natural rutile feedstock. Meanwhile, Western-qualified titanium sponge production has declined 9% to approximately 81,000 tonnes, while China’s share of global sponge production has risen to 70%.

Figure 1: Kasiya contained rutile resource vs. other rutile-bearing titanium deposits (Mt)

(Source: See Appendix 2)

Global primary rutile supply is in structural decline. Rutile reserves at Leonoil Company Limited’s Area 1 Mine are expected to be depleted within the next 2-3 years, and Energy Fuels Inc. has recently ceased operations at its Kwale Mine in Kenya. With no other large-scale primary rutile developments at an advanced stage, Sovereign is positioned to become the only large-scale primary producer of natural rutile globally.

Kasiya’s natural rutile has demonstrated premium chemical characteristics and suitability across all major end-use applications, with high TiO₂ content, low impurity levels, and favourable particle size distribution – positioning it as a preferred high-purity feedstock within a structurally undersupplied market.

Kasiya’s 222ktpa of natural rutile would represent a significant addition to Western-accessible non-pigment rutile supply, directly addressing the structural feedstock deficit facing the US, Japanese and European titanium industries.

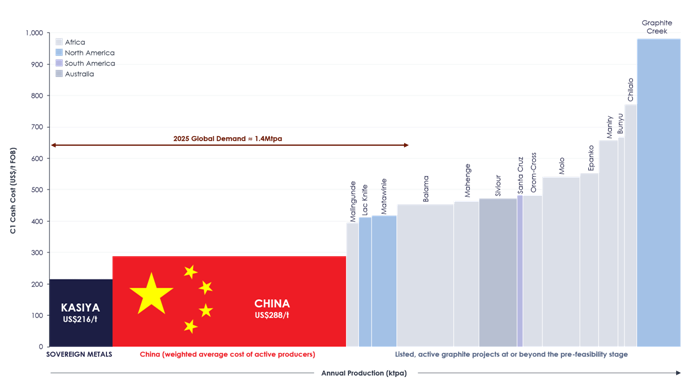

Natural Flake Graphite – Lowest-Cost Producer Outside Chinese Control

Graphite is essential to lithium-ion battery anodes, refractories and a range of advanced industrial applications. China currently dominates global natural graphite production and processing, accounting for approximately 77% of worldwide output and an even larger share of battery-grade anode material³. The US has designated graphite as a critical mineral and is actively seeking to diversify supply away from Chinese-controlled sources, including through the US$12 billion Project Vault strategic reserve initiative.

Kasiya’s incremental cost of graphite production is estimated at US$216/t. Based on public disclosures by listed graphite developers with studies at or beyond the pre-feasibility stage, this positions Sovereign as the lowest-cost graphite producer globally, including China (see Appendix 3).

Compared with single-commodity hard-rock graphite operations, Kasiya benefits from a soft, free-dig orebody and a simple processing flowsheet. The majority of operating costs are allocated to the primary rutile stream, enabling the production of high-purity, coarse-flake graphite at materially lower costs. Independent testing has confirmed that Kasiya graphite performs exceptionally well as an anode material for lithium-ion batteries, while also meeting specifications for traditional industrial markets such as refractories.

Figure 3: Natural flake graphite C1 cash costs. (Source: See Appendix 3. China cost from Benchmark Minerals Intelligence)

Figure 4: Utility-scale battery energy storage system using graphite anodes – California, USA.

SUMMARY OF KEY DFS WORKSTREAMS

Following input from world-class consultancies, Sovereign’s highly experienced owners’ team, and subject matter experts from Rio Tinto, the DFS has reconfirmed that Kasiya will be a leading future supplier to two distinct strategic critical minerals supply chains and outside of Chinese control – natural rutile for the titanium industry and natural flake graphite.

The DFS outlines a large-scale, long-life operation that delivers substantial volumes of premium-quality natural rutile and graphite while generating significant returns across a range of price scenarios.

The DFS for Kasiya has been prepared in accordance with the JORC Code (2012), with an estimated accuracy range of ±15% for Capital Expenditure (Capex) and ±10% for Operating Costs (Opex).

Dry Mining Method Confirmed

Using real-world data collected from the Pilot Mining, the DFS confirms a dry mechanical mining method using draglines and 100t rigid dump trucks. The soft, free-dig saprolite orebody requires no drilling, blasting, crushing or milling. A two-bench approach (5m top cut, up to 15m bottom cut) keeps the draglines above the water table, eliminating the need for production equipment below groundwater level. This represents a significant de-risking step from the hydro-mining method originally considered in the original Pre-feasibility Study (PFS).

No Conventional Tailings Storage Facility

A major advancement in the DFS is the elimination of the conventional Tailings Storage Facility (TSF) leading to a significant reduction in the mining footprint and providing a flexible, lower-risk tailings management solution. All tailings will be stored via hydraulic co-disposal backfilling of mined-out pits, designed in compliance with the Global Industry Standard on Tailings Management (GISTM), aiming for zero harm to people and the environment. The 50:50 fines-to-sand backfill ratio closely matches the existing soil profile, supporting progressive rehabilitation. This has also reduced the raw water dam wall height from 23m to 20.7m and storage capacity from 16.4 to 11Mm³.

Hydropower-Sourced Grid Electricity

The DFS is based on connection to Malawi’s national hydropower grid via a 132kV overhead line to the Nkhoma substation. Electricity Supply Corporation of Malawi Limited (ESCOM) has confirmed significant grid expansion is underway, including a 400kV Mozambique interconnector (2025) and the 375MW IFC/World Bank-funded Mpatamanga hydropower station (2030). Grid connection delivers substantially lower power costs and a favourable emissions profile.

Processing Flowsheet

Ore will be trucked to the processing plant for scrubbing and screening before entering the Wet Concentration Plant (WCP). The WCP employs a low-energy gravity separation process to produce a Heavy Mineral Concentrate (HMC). The HMC is then fed to the Mineral Separation Plant (MSP), where electrostatic and magnetic separation yield premium-quality rutile (+95% TiO₂), suitable as a direct feedstock for titanium sponge production or use in high-end titanium alloy applications, including aerospace and defence. Graphite-rich concentrate recovered from the spirals is processed in a dedicated flotation plant, producing a high-purity, high-crystallinity, coarse-flake graphite product. Independent testing has confirmed that Kasiya graphite performs exceptionally well as an anode material for lithium-ion batteries and meets specifications for traditional industrial markets such as refractories.

Dual Plant Configuration

The DFS confirms a staged development with two 12Mtpa processing plants – South Plant from Year 1 and North Plant from Year 5 – positioned at the respective resource centres of gravity to minimise haulage distances and costs. The configuration provides operational flexibility and a phased capital profile.

Logistics and Export Infrastructure

Kasiya’s products will be railed directly from a purpose-built dry port at the mine site eastward along the Nacala Logistics Corridor to the container terminal at the Port of Nacala on the Indian Ocean. The existing heavy-haul rail line and deep-water port provide a proven, operational export route – a significant infrastructure advantage over comparable undeveloped projects. Product transport cost is estimated at US$117/t product (FOB Nacala).

Rutile and Graphite Pricing

The DFS adopts a life-of-mine weighted-average realised rutile price of US$1,670/t (real, FOB Nacala), based on an independent TZMI market study. Japanese titanium metal producers OSAKA Titanium Technologies Co., Ltd. (Osaka Titanium) and Toho Titanium Co., Ltd. (Toho Titanium) are expected to drive the growth in rutile demand for titanium manufacturing over the next 10 years. Graphite pricing is based on an independent Benchmark Minerals Intelligence (BMI) price forecast, resulting in a life-of-mine average price of approximately US$1,288/t (FOB Nacala) – effectively in line with the OPFS assumption of US$1,290/t. The graphite basket price is derived from FOB China benchmarks, adjusted for an East Africa premium and weighted by Kasiya’s concentrate flake size distribution.

IFC Performance Standards Integrated into Design

The DFS has been prepared in alignment with IFC Performance Standards, with a comprehensive Environmental and Social Impact Assessment (ESIA) nearing completion and the full suite of environmental and social specialist studies completed. Sovereign’s established on-the-ground social team of 22 core staff and 90-member Community Liaison Team represent a level of social preparedness rarely achieved at DFS stage.

Mining and Rehabilitation Trials – Proven in Practice

Large-scale mining and rehabilitation trials were completed during the DFS period, covering excavation, backfilling, soil remediation and crop establishment. During Pilot Mining, the Company successfully completed dry and hydraulic mining trials, excavating a test pit at Kasiya. The test pit covered the planned area of 120 metres by 110 metres and was excavated to a depth of 20 metres through the weathered ore at Kasiya.

Post mining, the rehabilitated pit has achieved maize yields of 5.2 tonnes per hectare within six months of backfilling – over five times the local community average of approximately 1 tonne per hectare. The Pilot Mining validated the progressive rehabilitation approach and confirmed that mined land can be returned to productive agricultural use within one to two years.

|

Enquiries |

|

|

Frank Eagar, Managing Director & CEO South Africa / Malawi +27 21 140 3190

|

Sapan Ghai, CCO London +44 207 478 3900 |

|

Nominated Adviser on AIM and Joint Broker |

|

|

SP Angel Corporate Finance LLP |

+44 20 3470 0470 |

|

Ewan Leggat Charlie Bouverat |

|

|

|

|

|

Joint Broker |

|

|

Stifel |

+44 20 7710 7600 |

|

Varun Talwar |

|

|

Ashton Clanfield |

|

To view this announcement in full, including the Summary Section of the DFS and all images and figures, please refer to: https://api.investi.com.au/api/announcements/svm/b6f76c34-dfa.pdf.